Embed Size (px)

Citation preview

University of California,

Los Angeles Medical Center Report on Audits of Financial Statements For the Years Ended June 30, 2005 and 2004

University of California, Los Angeles Medical Center Report on Audits of Financial Statements

Table of Contents

Page Report of Independent Auditors 1 Management’s Discussion and Analysis 2 Financial Statements: Statements of Net Assets At June 30, 2005 and 2004 15 Statements of Revenues, Expenses and Changes in Net Assets For the Years Ended June 30, 2005 and 2004 16 Statements of Cash Flows For the Years Ended June 30, 2005 and 2004 17 Notes to Financial Statements 19

1

PricewaterhouseCoopers LLP 350 South Grand Avenue Los Angeles CA 90071 Telephone (213) 356 6000 Facsimile (813) 637 4444

Report of Independent Auditors

The Regents of the University of California Oakland, California In our opinion, the accompanying financial statements, as shown on pages 15 through 37, present fairly, in all material respects, the financial position of the University of California, Los Angeles Medical Center (the "Medical Center"), a division of the University of California (“University”), at June 30, 2005 and 2004, and changes in its financial position and cash flows for the years then ended in conformity with accounting principles generally accepted in the United States of America. These financial statements are the responsibility of the Medical Center's management. Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these statements in accordance with auditing standards generally accepted in the United States of America. These standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion. As discussed in Note 1, the financial statements of the Medical Center are intended to present the financial position, and the changes in financial position and cash flows of only that portion of the University that is attributable to the transactions of the Medical Center. They do not purport to, and do not, present fairly the financial position of the University as of June 30, 2005 and 2004, and its changes in financial position and cash flows for the years then ended in conformity with accounting principles generally accepted in the United States of America. The Management's Discussion and Analysis on pages 2 through 14 is not a required part of the basic financial statements but is supplementary information required by the Governmental Accounting Standards Board. We have applied certain limited procedures, which consist principally of inquiries of management regarding the methods of measurement and presentation of the required supplementary information. However, we did not audit the information and express no opinion on it.

September 21, 2005

University of California, Los Angeles Medical Center Management’s Discussion and Analysis

2

Introduction The objective of Management’s Discussion and Analysis is to help readers better understand UCLA Medical Center’s position and operating activities for the year ended June 30, 2005, with selected comparative information for the years ended June 30, 2004 and 2003. This discussion has been prepared by management and should be read in conjunction with the financial statements, starting on page 15, and the notes to the financial statements, starting on page 19. Unless otherwise indicated, years (2003, 2004, 2005, 2006 etc.) in this discussion refer to fiscal year ended June 30. Overview The University of California, Los Angeles Medical Center (the “Medical Center”) is part of the University of California (the “University”). The Medical Center operates licensed beds facilities as follows: the 669 bed UCLA Medical Center located in Westwood, the 291 bed Santa Monica-UCLA Medical Center located in Santa Monica, and the 136 bed Neuropsychiatric Hospital located in Westwood. The financial statements also include the activities of Tiverton House, a 100-room facility for patients and their families. The UCLA Medical Center serves as the principal teaching site for the David Geffen School of Medicine at UCLA. The Medical Center’s mission is to provide excellent patient care in support of the educational and scientific programs of the Schools of the UCLA Center for the Health Sciences, that include the Schools of Medicine, Dentistry, Nursing and Public Health. The Westwood campus opened in 1955 as a 320-bed hospital and expanded to its current capacity of 669 beds in 1967. Currently, construction is under way on a new 525-bed state-of-the-art replacement hospital expected to be completed in calendar year 2006 and to be opened for patient care in calendar year 2007. The replacement hospital will meet the State of California’s SB 1953, The Hospital Facilities Seismic Safety Act. The Medical Center offers patients of all ages comprehensive care, from routine to highly specialized medical and surgical treatment. In addition, the Westwood Campus is best known for the wide range of its tertiary/quaternary care offerings that include Level I trauma care, regional neonatal and pediatric intensive care units, Neurosurgery/Neurology, and organ transplantation.

University of California, Los Angeles Medical Center Management’s Discussion and Analysis

3

In 1995, the Santa Monica Hospital Medical Center was acquired by The Regents and renamed “Santa Monica – UCLA Medical Center.” This hospital is also dedicated to serving the University’s teaching and research missions while meeting the healthcare needs of Los Angeles’s west side. The Santa Monica campus features several nationally recognized clinical programs located within its seven-acre campus. Several sections of this medical center are also in the process of replacement and are expected to be completed in calendar year 2007. In 1998, UCLA Healthcare signed a strategic alliance with Orthopaedic Hospital/Los Angeles. This alliance will result in the relocation of Orthopaedic Hospital inpatient services to Santa Monica in July 2005. The UCLA Neuropsychiatric Hospital is one of the leading centers for comprehensive patient care, research and education in the fields of mental and developmental disabilities. Located on the Westwood Campus, the hospital offers a full range of treatment options for patients needing inpatient, outpatient, or partial-day services. The Tiverton House is a 100-room guest hotel for patients and their families. Tiverton was temporarily closed in March, 2002 in order to repair water damage. This work was completed in June, 2004 and Tiverton opened on July 1, 2004. Together, these sites enable the Medical Center to provide a full spectrum of services and attract the volume and diversity of patients necessary to meet its educational, clinical, research and community services missions. For the year ended June 30, 2005, the consolidated Medical Centers reported net income before other changes in net assets of $9.2 million generating a margin of 0.9%. The year ended with a cash position of $79.6 million. For 2004, net income before other changes in net assets was $11.7 million and cash totaled $64.5 million. Significant events affecting the year are summarized below: • New Executive Management Team

The most significant event of the year has been the appointment of the new executive leadership team: David Callender, Associate Vice Chancellor, Chief Executive Officer – Hospital System; Mitch Creem, Associate Vice Chancellor, Chief Financial Officer –Medical Sciences; Thomas Sibert, Associate Vice Chancellor, President Faculty Practice Group; and Paul Staton, Senior Associate Director, Chief Financial Officer – Hospital System. The Chief Operating Officer position for the Westwood campus was filled on an interim basis by an outside consultant during the fiscal year.

• Changes in Payor Mix

Total inpatient days increased by 2.1%. The increases were in Medi-Cal and Uninsured days of 3.4% and 26.9%, respectively. The acute average length of stay increased by 1.0% over the prior year. The adverse growth in Medi-Cal and Uninsured occurred primarily through the Emergency Department.

University of California, Los Angeles Medical Center Management’s Discussion and Analysis

4

• Price Increases

The Medical Center increased its prices for the majority of its services by approximately 10% on October 1, 2004. These price increases contributed to an increase in net patient revenue helping to offset the adverse payor mix.

• The Medical Center restructured its managed care arrangements and renegotiated major

third-party contracts

The Medical Center continued its efforts to reduce full-risk capitated contracts. During 2005, two full-risk plans were terminated and one plan was converted to fee-for-service. Capitation membership declined from 15,000 members in 2004 to approximately 5,000 members at the end of 2005.

• Cash Collections

During 2005, the Medical Center continued to work on ways to improve its cash position. The Medical Center established formal revenue cycle teams to focus on various revenue and cash initiatives. Cash collected on patient accounts increased by $58.4 million, or 9.2%, over 2004.

• Capital Leases for Equipment

The Medical Center continued its efforts to obtain financing for capital needs. During 2005, the Medical Center financed $9.5 million of equipment through capital leases. The interest rates for all of the Medical Center’s leases range between 0.0% and 9.4%.

• Wage Increases and Nursing Shortages

The nation-wide nursing shortage continues to have a significant impact on both the salary costs of hospital-employed nurses as well as the rate charged for nurses employed from nurse registry agencies. In 2002, the union representing the nurses renegotiated a three-year contract with annual wage increases ranging from 7% to 9.2%. This contract increased the Medical Center’s labor costs by approximately $10.0 million in 2005. Temporary labor costs have declined by approximately $3.0 million from the prior year. The 2005 average monthly cost was $800 thousand compared to $1.1 million in 2004. Nursing made up approximately 90% of this cost. Overall, labor and benefit costs per hospital-paid employee increased by 5.2% over 2004.

University of California, Los Angeles Medical Center Management’s Discussion and Analysis

5

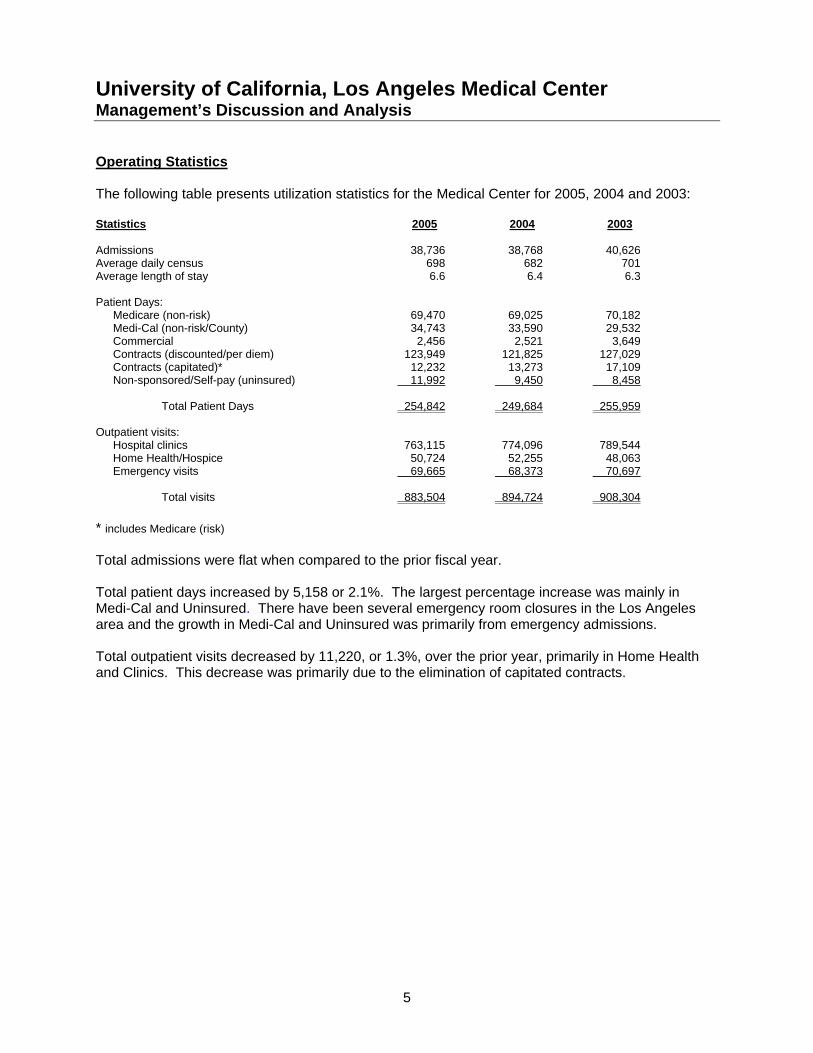

Operating Statistics The following table presents utilization statistics for the Medical Center for 2005, 2004 and 2003: Statistics 2005 2004 2003 Admissions 38,736 38,768 40,626 Average daily census 698 682 701 Average length of stay 6.6 6.4 6.3 Patient Days: Medicare (non-risk) 69,470 69,025 70,182 Medi-Cal (non-risk/County) 34,743 33,590 29,532 Commercial 2,456 2,521 3,649 Contracts (discounted/per diem) 123,949 121,825 127,029 Contracts (capitated)* 12,232 13,273 17,109 Non-sponsored/Self-pay (uninsured) 11,992 9,450 8,458 Total Patient Days 254,842 249,684 255,959

Outpatient visits: Hospital clinics 763,115 774,096 789,544 Home Health/Hospice 50,724 52,255 48,063 Emergency visits 69,665 68,373 70,697 Total visits 883,504 894,724 908,304 * includes Medicare (risk) Total admissions were flat when compared to the prior fiscal year. Total patient days increased by 5,158 or 2.1%. The largest percentage increase was mainly in Medi-Cal and Uninsured. There have been several emergency room closures in the Los Angeles area and the growth in Medi-Cal and Uninsured was primarily from emergency admissions. Total outpatient visits decreased by 11,220, or 1.3%, over the prior year, primarily in Home Health and Clinics. This decrease was primarily due to the elimination of capitated contracts.

University of California, Los Angeles Medical Center Management’s Discussion and Analysis

6

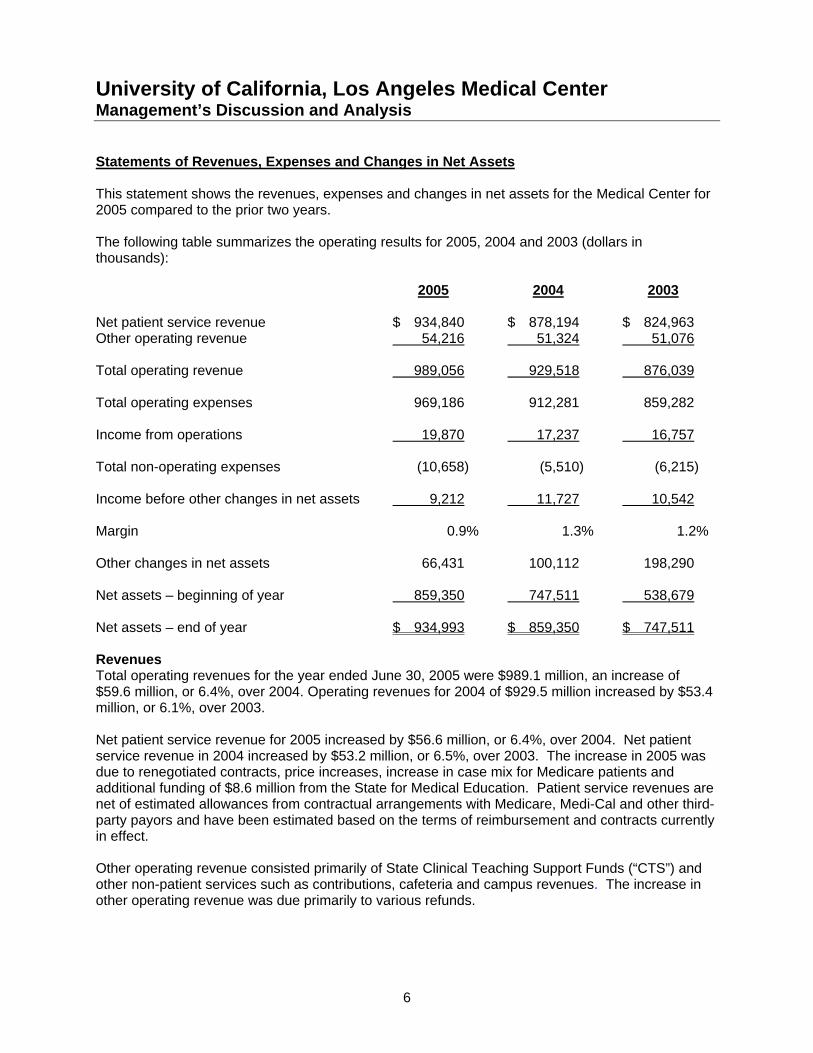

Statements of Revenues, Expenses and Changes in Net Assets This statement shows the revenues, expenses and changes in net assets for the Medical Center for 2005 compared to the prior two years. The following table summarizes the operating results for 2005, 2004 and 2003 (dollars in thousands): 2005 2004 2003 Net patient service revenue $ 934,840 $ 878,194 $ 824,963 Other operating revenue 54,216 51,324 51,076 Total operating revenue 989,056 929,518 876,039 Total operating expenses 969,186 912,281 859,282 Income from operations 19,870 17,237 16,757 Total non-operating expenses (10,658) (5,510) (6,215) Income before other changes in net assets 9,212 11,727 10,542 Margin 0.9% 1.3% 1.2% Other changes in net assets 66,431 100,112 198,290 Net assets – beginning of year 859,350 747,511 538,679 Net assets – end of year $ 934,993 $ 859,350 $ 747,511 Revenues Total operating revenues for the year ended June 30, 2005 were $989.1 million, an increase of $59.6 million, or 6.4%, over 2004. Operating revenues for 2004 of $929.5 million increased by $53.4 million, or 6.1%, over 2003. Net patient service revenue for 2005 increased by $56.6 million, or 6.4%, over 2004. Net patient service revenue in 2004 increased by $53.2 million, or 6.5%, over 2003. The increase in 2005 was due to renegotiated contracts, price increases, increase in case mix for Medicare patients and additional funding of $8.6 million from the State for Medical Education. Patient service revenues are net of estimated allowances from contractual arrangements with Medicare, Medi-Cal and other third-party payors and have been estimated based on the terms of reimbursement and contracts currently in effect. Other operating revenue consisted primarily of State Clinical Teaching Support Funds (“CTS”) and other non-patient services such as contributions, cafeteria and campus revenues. The increase in other operating revenue was due primarily to various refunds.

University of California, Los Angeles Medical Center Management’s Discussion and Analysis

7

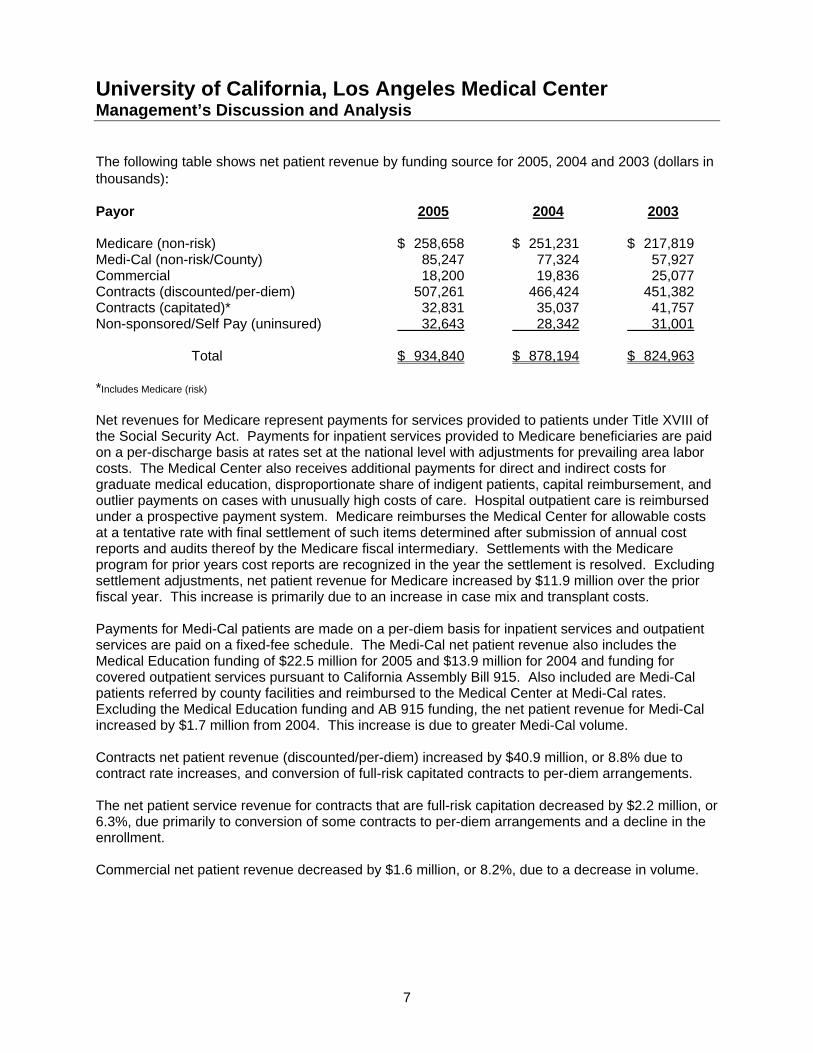

The following table shows net patient revenue by funding source for 2005, 2004 and 2003 (dollars in thousands): Payor 2005 2004 2003 Medicare (non-risk) $ 258,658 $ 251,231 $ 217,819 Medi-Cal (non-risk/County) 85,247 77,324 57,927 Commercial 18,200 19,836 25,077 Contracts (discounted/per-diem) 507,261 466,424 451,382 Contracts (capitated)* 32,831 35,037 41,757 Non-sponsored/Self Pay (uninsured) 32,643 28,342 31,001 Total $ 934,840 $ 878,194 $ 824,963 *Includes Medicare (risk) Net revenues for Medicare represent payments for services provided to patients under Title XVIII of the Social Security Act. Payments for inpatient services provided to Medicare beneficiaries are paid on a per-discharge basis at rates set at the national level with adjustments for prevailing area labor costs. The Medical Center also receives additional payments for direct and indirect costs for graduate medical education, disproportionate share of indigent patients, capital reimbursement, and outlier payments on cases with unusually high costs of care. Hospital outpatient care is reimbursed under a prospective payment system. Medicare reimburses the Medical Center for allowable costs at a tentative rate with final settlement of such items determined after submission of annual cost reports and audits thereof by the Medicare fiscal intermediary. Settlements with the Medicare program for prior years cost reports are recognized in the year the settlement is resolved. Excluding settlement adjustments, net patient revenue for Medicare increased by $11.9 million over the prior fiscal year. This increase is primarily due to an increase in case mix and transplant costs. Payments for Medi-Cal patients are made on a per-diem basis for inpatient services and outpatient services are paid on a fixed-fee schedule. The Medi-Cal net patient revenue also includes the Medical Education funding of $22.5 million for 2005 and $13.9 million for 2004 and funding for covered outpatient services pursuant to California Assembly Bill 915. Also included are Medi-Cal patients referred by county facilities and reimbursed to the Medical Center at Medi-Cal rates. Excluding the Medical Education funding and AB 915 funding, the net patient revenue for Medi-Cal increased by $1.7 million from 2004. This increase is due to greater Medi-Cal volume. Contracts net patient revenue (discounted/per-diem) increased by $40.9 million, or 8.8% due to contract rate increases, and conversion of full-risk capitated contracts to per-diem arrangements. The net patient service revenue for contracts that are full-risk capitation decreased by $2.2 million, or 6.3%, due primarily to conversion of some contracts to per-diem arrangements and a decline in the enrollment. Commercial net patient revenue decreased by $1.6 million, or 8.2%, due to a decrease in volume.

University of California, Los Angeles Medical Center Management’s Discussion and Analysis

8

The uninsured pay net revenue increased from the prior year by $4.3 million, or 15.2%. This category fluctuates from year to year depending on the volume and type of patients. The closure of hospitals and emergency rooms in the Los Angeles area could increase the volume of uninsured patients in the future. Reimbursement for uninsured patients is significantly reduced by the provision for doubtful accounts, which is included in operating expense. Operating Expenses Total operating expenses for 2005 were $969.2 million, an increase of $56.9 million, or 6.2%, over 2004. This increase was primarily due to increased salary costs, increases in employee benefit costs, inflationary increases in medical supplies and increases in purchased services. Total operating expenses for 2004 increased by $53.0 million, or 6.2%, over 2003 due to similar reasons. Salaries and employee benefit expenses increased by $37.2 million, or 7.6%, over the prior year due to a 2.5% increase in staffing, inflation in negotiated union wage increases, and higher benefit costs. Salary increases accounted for $24.4 million, due mainly to $16.9 million in negotiated nursing wage increases from union contracts and increased staffing. Increases in total benefits costs were $12.1 million, with health insurance benefits higher by $6.2 million and workers’ compensation insurance premiums up $1.9 million. Salary and employee benefit expenses increased by $15.8 million in 2004 over 2003. Payments for professional services decreased by $700 thousand or 4.0% from 2004, primarily due to decrease in contracted interim management services. Professional services decreased by $2.8 million, or 20.3%, in 2004 from 2003. Medical supply expense increased by $6.7 million, or 4.4%, mainly due to $4.7 million higher pharmaceutical costs for increased usage of blood factors, oncology, and transplant anti-rejection drugs. Prosthesis supply increased $700 thousand and other medical supplies were up $1.3 million. Medical supply expense increased in 2004 by $13.3 million, or 9.6%, over 2003 due to inflation and volume increases. Other supplies and purchased services increased by $11.0 million, or 6.1%, over the prior year due to a $3.7 million increase in transplant organ acquisition costs, $2.0 million increase in blood purchased services, $2.0 million increase in repairs and maintenance expense, ($700) thousand reduction in outside provider costs, $1.2 million increase in other purchased services and a $2.8 million increase in food, minor medical equipment and miscellaneous non-medical supplies. Other supplies and purchased services increased $12.1 million in 2004 over 2003. Depreciation and amortization expense increased by $800 thousand over the prior year due to investments in capital assets. Provision for doubtful accounts was comparable to the prior year. Insurance expense of $8.9 million was primarily the Medical Center’s contribution to the University of California self-insured malpractice fund. This expense increased by $1.4 million, or 19.1%, over the prior year.

University of California, Los Angeles Medical Center Management’s Discussion and Analysis

9

Non-Operating Revenue (Expense) Total non-operating expenses were $10.7 million for 2005 compared to $5.5 million in the prior year. The majority of this increase was primarily due to an increase in interest expense of $2.2 million and replacement hospital transition expense of $4.1 million. The replacement hospital transition expense is composed primarily of salary and consulting expenses related to the planning, coordination and logistics of moving to the replacement hospitals. Interest income increased by $1.1 million over the prior year. Income (Loss) before Other Changes in Net Assets The Medical Center’s income before other changes in net assets was $9.2 million for 2005 compared to $11.7 million for 2004 and $10.5 million in 2003. The Medical Center’s net income decreased from prior year due to an adverse payor mix resulting in increased costs. Increased expenses were in salary and benefit costs and inflationary increases in medical supplies and purchased services. Other Changes in Net Assets The lower section of the Statement of Revenues, Expenses and Changes in Net Assets shows the other changes to net assets in addition to the income or loss. Net assets are the difference between the total assets and total liabilities. The other changes in net assets represents additional funds the Medical Center receives and cash outflow for support and transfers to other university entities. Included in the other changes in net assets are the following: • Proceeds received and receivable from the Federal Emergency Management Agency

(“FEMA”) for the hospitals' replacement projects were $44.6 million in 2005. The total anticipated funding from FEMA for the replacement hospitals’ project is $512.0 million. The total received to date from FEMA is $481.8 million.

• Contributions from the University for the building program of $31.5 million are related to the

hospitals’ replacement projects and represent funding from the State Public Works Board Bonds totaling $30.5 million and funding from the line of credit of $1.0 million.

• Donated assets represent gift funds that have been used for the hospitals' replacement. The

gift funds are only recorded on the Medical Center’s financial statements when an expenditure for the project has been incurred. The Medical Center recorded $14.4 million of gift funds during 2005.

• Health system support represents transfers primarily to the School of Medicine for academic

and clinical support including the Primary Care Network. The Medical Center transferred $24.1 million this year.

In total, the net assets increased for the year by $75.6 million to $935.0 million. The majority of this increase is due to FEMA funds, contributions from the University, and gift funds for the hospitals' replacement projects.

University of California, Los Angeles Medical Center Management’s Discussion and Analysis

10

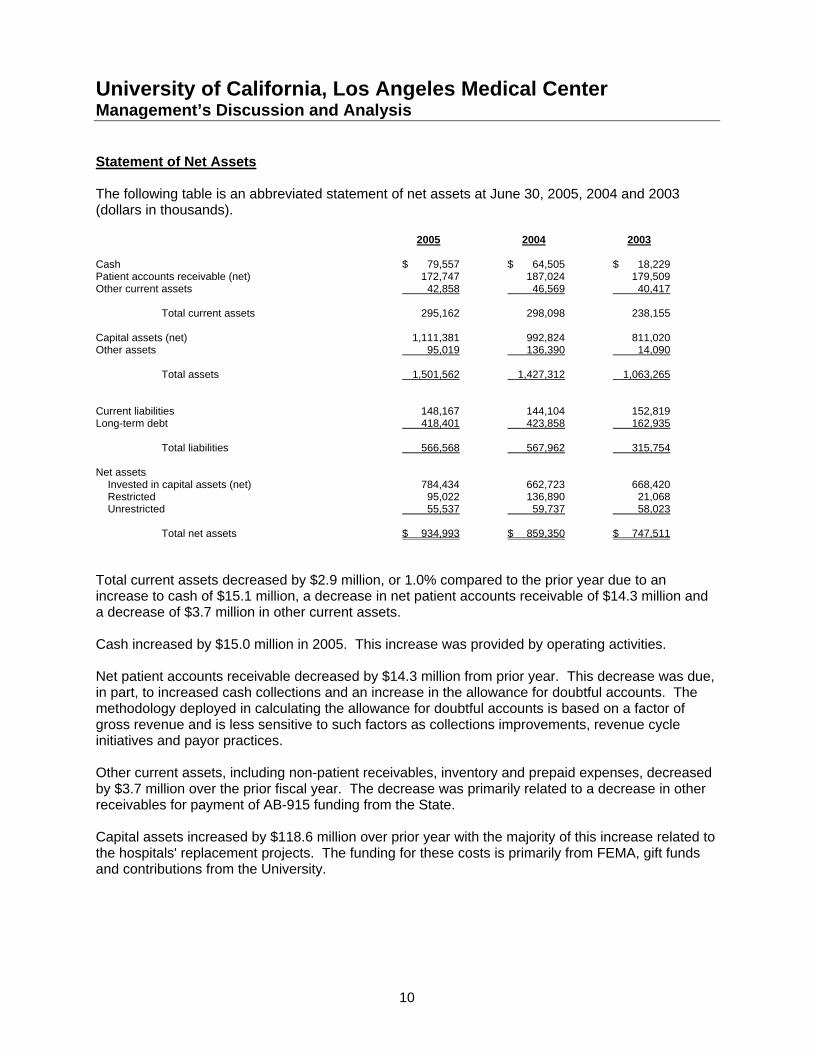

Statement of Net Assets The following table is an abbreviated statement of net assets at June 30, 2005, 2004 and 2003 (dollars in thousands). 2005 2004 2003 Cash $ 79,557 $ 64,505 $ 18,229 Patient accounts receivable (net) 172,747 187,024 179,509 Other current assets 42,858 46,569 40,417 Total current assets 295,162 298,098 238,155 Capital assets (net) 1,111,381 992,824 811,020 Other assets 95,019 136,390 14,090 Total assets 1,501,562 1,427,312 1,063,265 Current liabilities 148,167 144,104 152,819 Long-term debt 418,401 423,858 162,935 Total liabilities 566,568 567,962 315,754 Net assets Invested in capital assets (net) 784,434 662,723 668,420 Restricted 95,022 136,890 21,068 Unrestricted 55,537 59,737 58,023 Total net assets $ 934,993 $ 859,350 $ 747,511 Total current assets decreased by $2.9 million, or 1.0% compared to the prior year due to an increase to cash of $15.1 million, a decrease in net patient accounts receivable of $14.3 million and a decrease of $3.7 million in other current assets. Cash increased by $15.0 million in 2005. This increase was provided by operating activities. Net patient accounts receivable decreased by $14.3 million from prior year. This decrease was due, in part, to increased cash collections and an increase in the allowance for doubtful accounts. The methodology deployed in calculating the allowance for doubtful accounts is based on a factor of gross revenue and is less sensitive to such factors as collections improvements, revenue cycle initiatives and payor practices. Other current assets, including non-patient receivables, inventory and prepaid expenses, decreased by $3.7 million over the prior fiscal year. The decrease was primarily related to a decrease in other receivables for payment of AB-915 funding from the State. Capital assets increased by $118.6 million over prior year with the majority of this increase related to the hospitals' replacement projects. The funding for these costs is primarily from FEMA, gift funds and contributions from the University.

University of California, Los Angeles Medical Center Management’s Discussion and Analysis

11

Other assets, including the long-term portion of cash held by trustees, the Santa Monica Hospital Foundation assets, and the restricted funds for the hospitals’ replacement building projects decreased by $41.4 million from the prior year. This decrease is related the draw-down portion of the 2004 bond proceeds that was restricted for the hospitals’ replacement building projects. Current liabilities increased by $4.1 million from the prior year due to a decrease in accounts payable of $8.0 million, an increase in accrued payroll of $9.4 million, an increase in the current portion of long-term debt of $1.8 million, and an increase of $900 thousand in other liabilities. The increase in accrued payroll is due to the timing of the pay periods. The decrease in accounts payable is due to paying vendors more timely. Long-term debt includes the 2004 Series A and Series B Hospital Revenue Bonds, 2003 General Revenue Bonds, 2002 Hospital Revenue Bonds, and long-term capital leases. The Medical Center financed $9.5 million of capital equipment through leases during 2005. The note payable to campus is for long-term operating capital needs. Liquidity and Capital Resources The Statement of Cash Flows can be found on page 17. During 2005, the Medical Center generated $84.2 million from operating activities. Cash flows from non-capital financing activities shows the Medical Center’s cash was reduced by $24.1 million for transfers to the University for health system support and general support and $4.1 million for the replacement hospital transition costs. Included in cash flows from capital and related financing activities are the proceeds from FEMA ($37.4 million), contributions from the University for funding from the State Public Works Board Bonds ($31.5 million), sale of capital assets $1.7 million, and gifts ($14.3 million) that were used to partially fund capital assets ($147.3 million). Principal payments on long-term debt and capital leases were $12.9 million and interest paid was $10.8 million. Cash flows from investment activities show that $3.1 million was provided by interest income, $42.1 million from a change in restricted assets, primarily proceeds from new debt for the building project and $200 thousand from the Santa Monica Foundation. Overall cash increased to $79.6 million in 2005 from $64.5 million in 2004.

University of California, Los Angeles Medical Center Management’s Discussion and Analysis

12

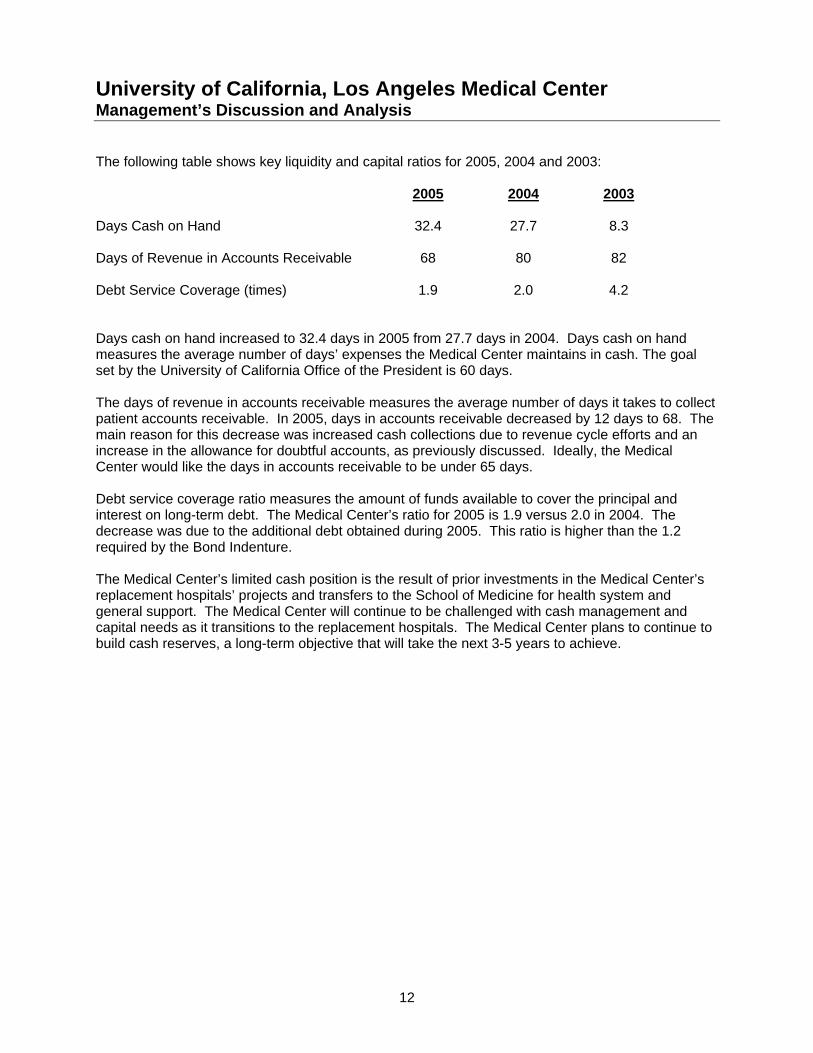

The following table shows key liquidity and capital ratios for 2005, 2004 and 2003: 2005 2004 2003 Days Cash on Hand 32.4 27.7 8.3 Days of Revenue in Accounts Receivable 68 80 82 Debt Service Coverage (times) 1.9 2.0 4.2 Days cash on hand increased to 32.4 days in 2005 from 27.7 days in 2004. Days cash on hand measures the average number of days’ expenses the Medical Center maintains in cash. The goal set by the University of California Office of the President is 60 days. The days of revenue in accounts receivable measures the average number of days it takes to collect patient accounts receivable. In 2005, days in accounts receivable decreased by 12 days to 68. The main reason for this decrease was increased cash collections due to revenue cycle efforts and an increase in the allowance for doubtful accounts, as previously discussed. Ideally, the Medical Center would like the days in accounts receivable to be under 65 days. Debt service coverage ratio measures the amount of funds available to cover the principal and interest on long-term debt. The Medical Center’s ratio for 2005 is 1.9 versus 2.0 in 2004. The decrease was due to the additional debt obtained during 2005. This ratio is higher than the 1.2 required by the Bond Indenture. The Medical Center’s limited cash position is the result of prior investments in the Medical Center’s replacement hospitals’ projects and transfers to the School of Medicine for health system and general support. The Medical Center will continue to be challenged with cash management and capital needs as it transitions to the replacement hospitals. The Medical Center plans to continue to build cash reserves, a long-term objective that will take the next 3-5 years to achieve.

University of California, Los Angeles Medical Center Management’s Discussion and Analysis

13

Looking Forward The Hospital Facilities Seismic Safety Act (SB 1953) During 2005, the Medical Center’s capital program continued to address the requirements in the Hospital Facilities Seismic Safety Act. The projected cost for the Medical Center, which will be compliant with the requirements by January 1, 2008, is $1.0 billion. The capital cost of compliance will be financed through the use of State lease revenue bond funds, Federal Emergency Management Administration (“FEMA”) funds, Hospital Reserves, gift funds and the debt. In 2005, $144.4 million was spent. Regulatory Risk Entities doing business with governmental payors, including Medicare and Medicaid (Medi-Cal in California), are subject to risks unique to the government-contracting environment that are hard to anticipate and quantify. Revenues are subject to adjustment as a result of examination by government agencies or contractors. The audit process and the resolution of significant related matters (including disputes based on differing interpretations of the regulations) often are not finalized until several years after the services were rendered. Medicaid Reform There are efforts to reform components of the Medicaid (Medi-Cal in California) program. Items that have been proposed include additional co-pays and deductibles for patients, expanded use of managed care and other coordinated systems of care for the chronically ill, and changes to hospital supplemental payment systems. Although these changes have been advanced in California to improve the quality of care to Medicaid beneficiaries and help maintain Medicaid supplemental payments to teaching hospitals and other hospitals that serve a large volume of Medicaid patients, the full financial impact of these changes can not be fully assessed at this time. The Medical Center currently incurs significant unreimbursed expenses related to serving Medi-Cal and uninsured patients. Children’s Hospital Bond Act of 2004 California voters passed Proposition 61 that enables the State of California to issue $750 million in General Obligation bonds to fund capital improvement projects for children’s hospitals. Each of the University medical centers is eligible for $30 million of grant funding from this pool of funds. Grant funds must be used for capital projects associated with the care of children and must be used prior to June 30, 2014. Request for Proposition 61 funds will be made in future years as specific projects are identified.

University of California, Los Angeles Medical Center Management’s Discussion and Analysis

14

University of California Retirement Plan The University of California Retirement Plan (“UCRP”) costs are funded by a combination of investment earnings, employee member and employer contributions. Since 1990, the Medical Center’s contribution rate to the UCRP has been zero. In addition, since 1990, most of the required employee member contributions to the UCRP are being redirected to the separate defined contribution plan maintained by the University. Actuarial reviews of the UCRP have determined that, given its financial position and its ability to meet its benefit obligations, employer and employee member contributions are not currently needed and will not be needed in 2006. However, it is not reasonable to expect the Plan to maintain its high level of surplus and The Regents may require contributions at a future date. The zero rate for UCRP contributions and the redirection of employee member UCRP contributions will be reviewed annually by The Regents with the consulting actuaries and continue only until such time as a resumption of employer and employee member contributions to the UCRP are again required to maintain actuarially sound funding levels. Replacement Hospital’s Depreciation Expense It is anticipated that the Replacement Hospitals will be opened to accept patients in 2007. When this occurs, the financial statements will be adversely affected, as there will be a significant increase in depreciation expense for the building due to approximately $1.0 billion of assets that will begin to be depreciated. The Medical Center is currently exploring options as to the accounting treatment of the carrying value of this asset. Cautionary Note Regarding Forward-Looking Statements Certain information provided by the Medical Center, including written as outlined above or oral statements made by its representatives, may contain forward-looking statements as defined in the Private Securities Litigation Reform Act of 1995. All statements, other than statements of historical facts, which address activities, events or developments that the Medical Center expects or anticipates will or may occur in the future contain forward-looking information. In reviewing such information it should be kept in mind that actual results may differ materially from those projected or suggested in such forward-looking information. This forward-looking information is based upon various factors and was derived using various assumptions. The Medical Center does not undertake to update forward-looking information contained in this report or elsewhere to reflect actual results, changes in assumptions or changes in other factors affecting such forward-looking information.

The accompanying notes are an integral part of these financial statements.

15

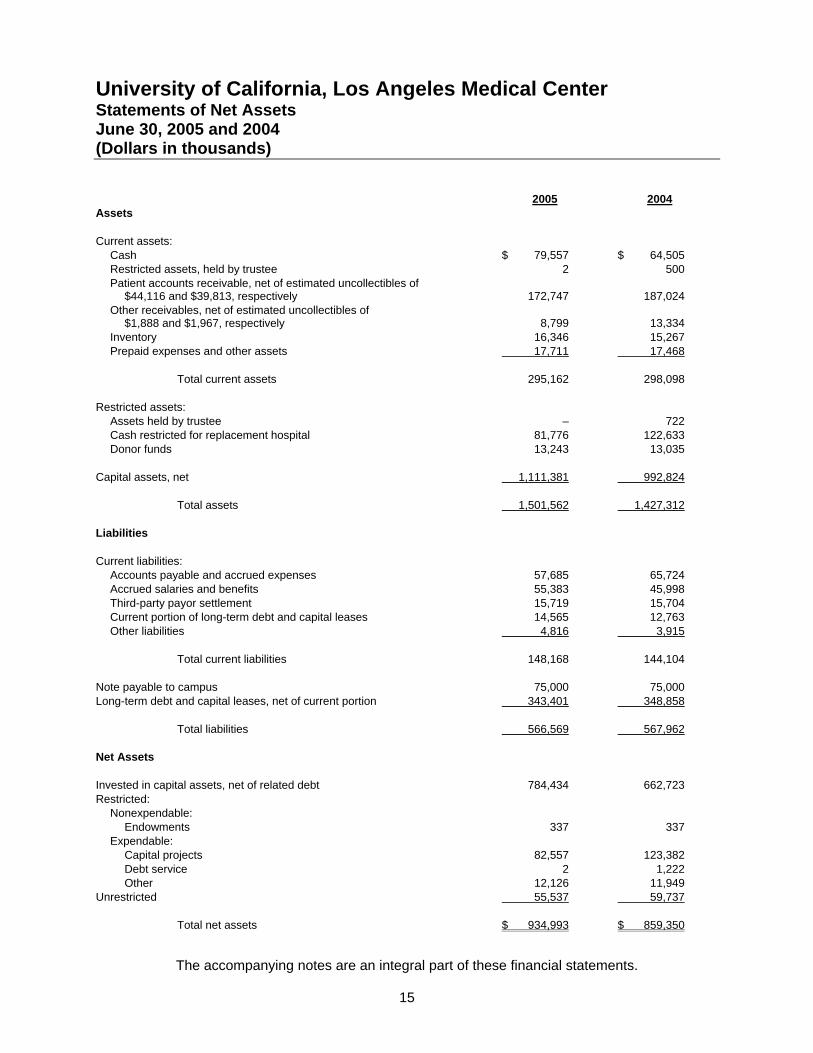

University of California, Los Angeles Medical Center Statements of Net Assets June 30, 2005 and 2004 (Dollars in thousands) 2005 2004 Assets Current assets: Cash $ 79,557 $ 64,505 Restricted assets, held by trustee 2 500 Patient accounts receivable, net of estimated uncollectibles of $44,116 and $39,813, respectively 172,747 187,024 Other receivables, net of estimated uncollectibles of $1,888 and $1,967, respectively 8,799 13,334 Inventory 16,346 15,267 Prepaid expenses and other assets 17,711 17,468 Total current assets 295,162 298,098 Restricted assets: Assets held by trustee – 722 Cash restricted for replacement hospital 81,776 122,633 Donor funds 13,243 13,035 Capital assets, net 1,111,381 992,824 Total assets 1,501,562 1,427,312 Liabilities Current liabilities: Accounts payable and accrued expenses 57,685 65,724 Accrued salaries and benefits 55,383 45,998 Third-party payor settlement 15,719 15,704 Current portion of long-term debt and capital leases 14,565 12,763 Other liabilities 4,816 3,915 Total current liabilities 148,168 144,104 Note payable to campus 75,000 75,000 Long-term debt and capital leases, net of current portion 343,401 348,858 Total liabilities 566,569 567,962 Net Assets Invested in capital assets, net of related debt 784,434 662,723 Restricted: Nonexpendable: Endowments 337 337 Expendable: Capital projects 82,557 123,382 Debt service 2 1,222 Other 12,126 11,949 Unrestricted 55,537 59,737 Total net assets $ 934,993 $ 859,350

The accompanying notes are an integral part of these financial statements.

16

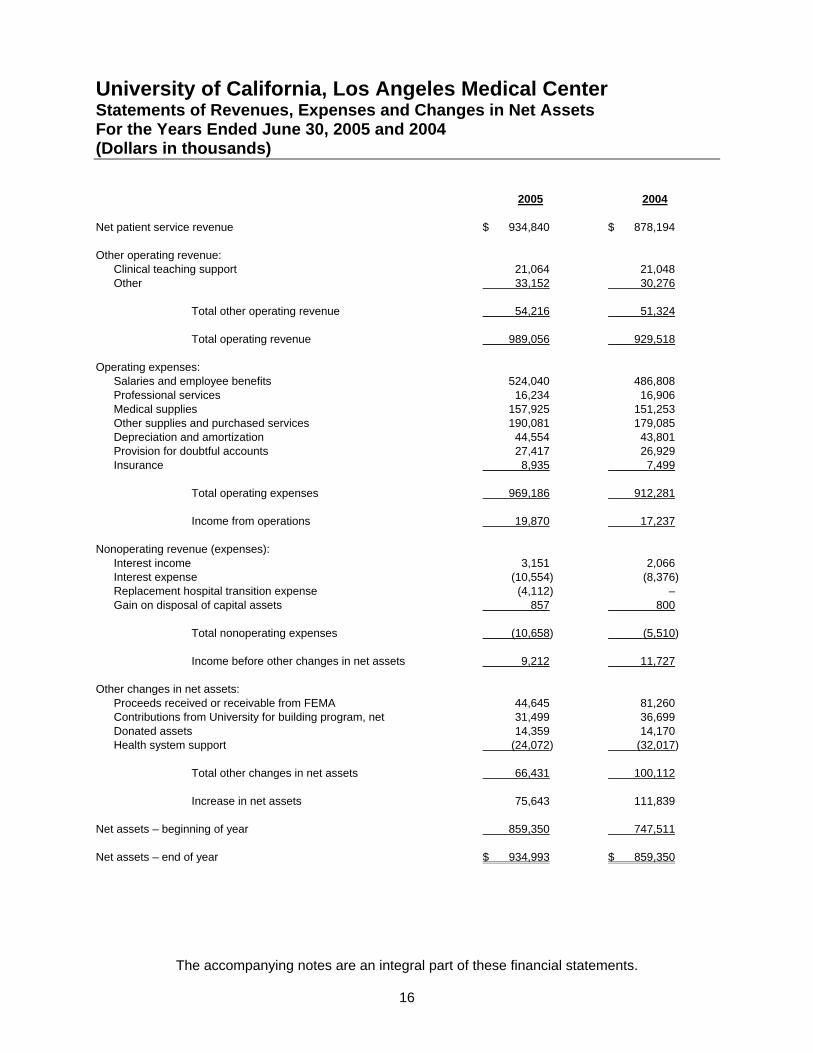

University of California, Los Angeles Medical Center Statements of Revenues, Expenses and Changes in Net Assets For the Years Ended June 30, 2005 and 2004 (Dollars in thousands) 2005 2004 Net patient service revenue $ 934,840 $ 878,194 Other operating revenue: Clinical teaching support 21,064 21,048 Other 33,152 30,276 Total other operating revenue 54,216 51,324 Total operating revenue 989,056 929,518 Operating expenses: Salaries and employee benefits 524,040 486,808 Professional services 16,234 16,906 Medical supplies 157,925 151,253 Other supplies and purchased services 190,081 179,085 Depreciation and amortization 44,554 43,801 Provision for doubtful accounts 27,417 26,929 Insurance 8,935 7,499 Total operating expenses 969,186 912,281 Income from operations 19,870 17,237 Nonoperating revenue (expenses): Interest income 3,151 2,066 Interest expense (10,554) (8,376) Replacement hospital transition expense (4,112) – Gain on disposal of capital assets 857 800 Total nonoperating expenses (10,658) (5,510) Income before other changes in net assets 9,212 11,727 Other changes in net assets: Proceeds received or receivable from FEMA 44,645 81,260 Contributions from University for building program, net 31,499 36,699 Donated assets 14,359 14,170 Health system support (24,072) (32,017) Total other changes in net assets 66,431 100,112 Increase in net assets 75,643 111,839 Net assets – beginning of year 859,350 747,511 Net assets – end of year $ 934,993 $ 859,350

The accompanying notes are an integral part of these financial statements.

17

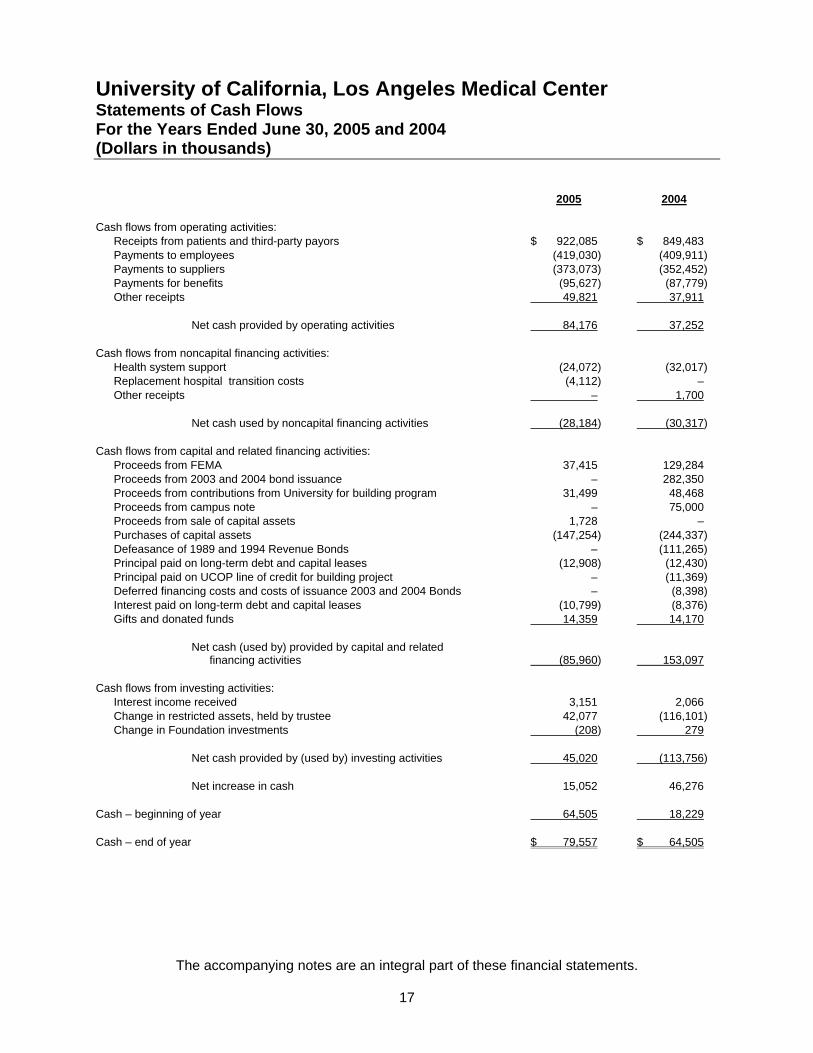

University of California, Los Angeles Medical Center Statements of Cash Flows For the Years Ended June 30, 2005 and 2004 (Dollars in thousands) 2005 2004 Cash flows from operating activities: Receipts from patients and third-party payors $ 922,085 $ 849,483 Payments to employees (419,030) (409,911) Payments to suppliers (373,073) (352,452) Payments for benefits (95,627) (87,779) Other receipts 49,821 37,911 Net cash provided by operating activities 84,176 37,252 Cash flows from noncapital financing activities: Health system support (24,072) (32,017) Replacement hospital transition costs (4,112) – Other receipts – 1,700 Net cash used by noncapital financing activities (28,184) (30,317) Cash flows from capital and related financing activities: Proceeds from FEMA 37,415 129,284 Proceeds from 2003 and 2004 bond issuance – 282,350 Proceeds from contributions from University for building program 31,499 48,468 Proceeds from campus note – 75,000 Proceeds from sale of capital assets 1,728 – Purchases of capital assets (147,254) (244,337) Defeasance of 1989 and 1994 Revenue Bonds – (111,265) Principal paid on long-term debt and capital leases (12,908) (12,430) Principal paid on UCOP line of credit for building project – (11,369) Deferred financing costs and costs of issuance 2003 and 2004 Bonds – (8,398) Interest paid on long-term debt and capital leases (10,799) (8,376) Gifts and donated funds 14,359 14,170 Net cash (used by) provided by capital and related financing activities (85,960) 153,097 Cash flows from investing activities: Interest income received 3,151 2,066 Change in restricted assets, held by trustee 42,077 (116,101) Change in Foundation investments (208) 279 Net cash provided by (used by) investing activities 45,020 (113,756) Net increase in cash 15,052 46,276 Cash – beginning of year 64,505 18,229 Cash – end of year $ 79,557 $ 64,505

The accompanying notes are an integral part of these financial statements.

18

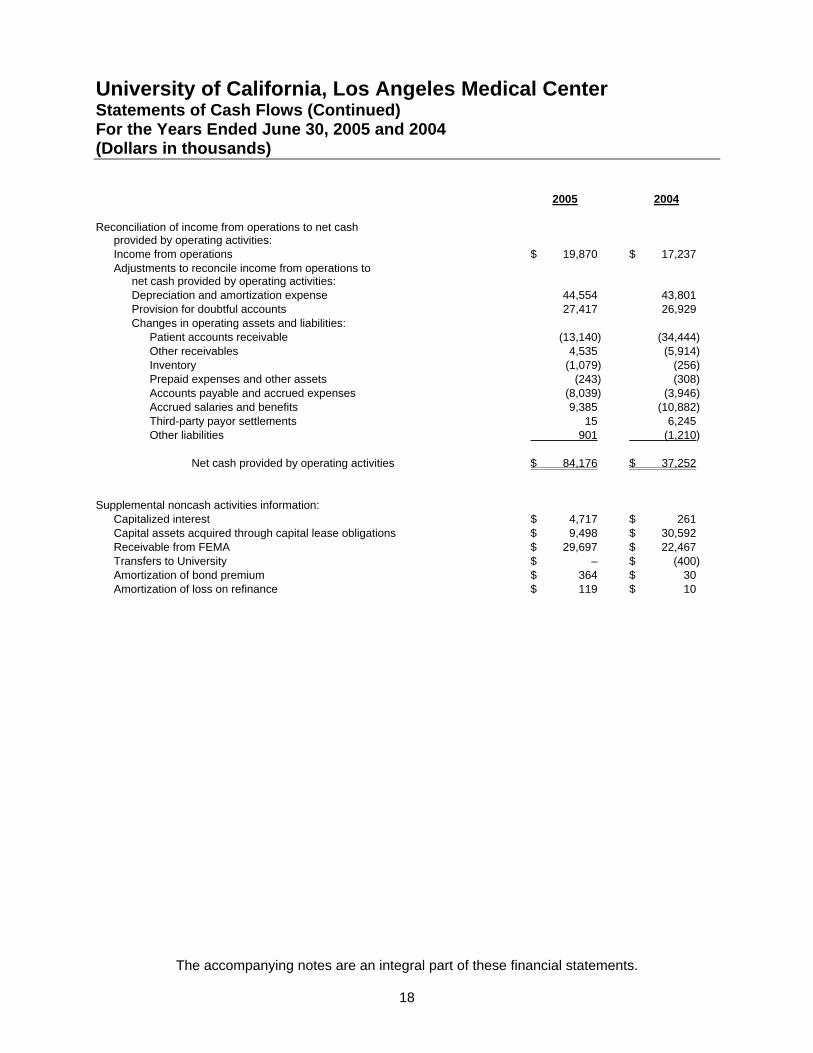

University of California, Los Angeles Medical Center Statements of Cash Flows (Continued) For the Years Ended June 30, 2005 and 2004 (Dollars in thousands) 2005 2004 Reconciliation of income from operations to net cash provided by operating activities: Income from operations $ 19,870 $ 17,237 Adjustments to reconcile income from operations to net cash provided by operating activities: Depreciation and amortization expense 44,554 43,801 Provision for doubtful accounts 27,417 26,929 Changes in operating assets and liabilities: Patient accounts receivable (13,140) (34,444) Other receivables 4,535 (5,914) Inventory (1,079) (256) Prepaid expenses and other assets (243) (308) Accounts payable and accrued expenses (8,039) (3,946) Accrued salaries and benefits 9,385 (10,882) Third-party payor settlements 15 6,245 Other liabilities 901 (1,210) Net cash provided by operating activities $ 84,176 $ 37,252 Supplemental noncash activities information: Capitalized interest $ 4,717 $ 261 Capital assets acquired through capital lease obligations $ 9,498 $ 30,592 Receivable from FEMA $ 29,697 $ 22,467 Transfers to University $ – $ (400) Amortization of bond premium $ 364 $ 30 Amortization of loss on refinance $ 119 $ 10

University of California, Los Angeles Medical Center Notes to Financial Statements (Dollars in thousands)

19

1. Organization

The University of California, Los Angeles Medical Center (the “Medical Center”) is a part of the University of California (the “University”), a California public corporation established under Article IX, Section 9 of the California Constitution. The University is administered by The Regents of the University of California (“The Regents”), an independent board composed of 26 members. The Medical Center’s activities are monitored by The Regents’ Committee on Health Services, with direct management authority being delegated to the Vice Chancellor, Medical Sciences by the Chancellor of the Los Angeles campus. The Medical Center operates licensed bed facilities including the 669 bed UCLA Medical Center, the 291 bed Santa Monica – UCLA Medical Center, and the 136 bed Neuropsychiatric Hospital. The financial statements also include the activities of Tiverton House, a 100-room facility for patients and their families.

2. Summary of Significant Accounting Policies

Basis of Presentation The financial statements of the Medical Center have been prepared in accordance with accounting principles generally accepted in the United States of America, including all applicable statements of the Governmental Accounting Standards Board (“GASB”), and all statements of the Financial Accounting Standards Board through November 30, 1989. The proprietary fund method of accounting is followed and uses the economic resources measurement focus and the accrual basis of accounting. In addition, these statements follow generally accepted accounting principles applicable to the health care industry, which are included in the American Institute of Certified Public Accountants’ Audit and Accounting Guide, Health Care Organizations to the extent that these principles do not contradict GASB. GASB Statement No. 40, Deposit and Investment Risk Disclosures, was adopted during the year ended June 30, 2005 and retroactively applied as of July 1, 2003. Statement No. 40 establishes additional disclosure requirements addressing common risks of deposits and investments. The implementation of Statement No. 40 had no effect on the Medical Center’s net assets or changes in net assets for the years ended June 30, 2005 and 2004. GASB Statement No. 42, Accounting and Financial Reporting for Impairment of Capital Assets and for Insurance Recoveries, was also adopted during the year ended June 30, 2005. Statement No. 42 requires an evaluation of prominent events or changes in circumstances to determine whether an impairment loss should be recorded and whether any insurance recoveries should be offset against the impairment loss. The implementation of Statement No. 42 had no effect on the Medical Center’s net assets or changes in net assets for the years ended June 30, 2005 and 2004.

University of California, Los Angeles Medical Center Notes to Financial Statements (Dollars in thousands)

20

2. Summary of Significant Accounting Policies (Continued)

Cash All University operating entities invest surplus cash balances in a short-term investment pool (“STIP”) managed by the Treasurer of The Regents. The Regents are responsible for managing University’s investments and establishing investment policy, which is carried out by the Treasurer of The Regents. Substantially all of the Medical Center’s cash is deposited into the STIP. All Medical Center deposits into the STIP are considered demand deposits. Unrealized gains and losses associated with the fluctuation in the fair value of the investments included in the STIP (and predominately held to maturity) are not recorded by each operating entity but are absorbed by the University, as the manager of the pool. The Medical Center’s cash at June 30, 2005 and 2004 was $79,557 and $64,505, respectively. None of these amounts are insured by the Federal Deposit Insurance Corporation. Interest income is reported as non-operating revenue in the statements of revenues, expenses and changes in net assets. Additional information on cash and investments can be obtained from the 2004-2005 annual report of the University. Restricted Assets, Held By Trustee Indenture requirements of bond financing (see Note 8, “Long-term Debt”) provide for the establishment and maintenance of various accounts with a trustee. The indenture terms require that the trustee control the expenditure of bond proceeds as well as the payment of principal and interest to the bondholders. Assets held by trustee consist of short-term investments, recorded at cost, which approximates fair value. Restricted Assets, Replacement Hospitals The proceeds from the Revenue Bonds, Series A, are held by the Treasurer of The Regents. The University draws from these funds as expenditures are incurred. Restricted Assets, Donor Funds Santa Monica Foundation investments, which are part of the Medical Center, are recorded at fair value, which approximates cost. Pledges and charitable remainder trusts are discounted using a risk free rate of interest, and an actuarially determined liability for gift annuity funds. Real property is recorded at cost. Inventory The Medical Center’s inventory consists primarily of pharmaceuticals and medical supplies which is stated on a first-in, first-out basis at the lower of cost or market.

University of California, Los Angeles Medical Center Notes to Financial Statements (Dollars in thousands)

21

2. Summary of Significant Accounting Policies (Continued)

Prepaid Expenses and Other Assets The Medical Center’s prepaid expenses and other assets are primarily prepayments for pharmaceuticals and medical supplies, rent, equipment maintenance contracts, and the costs incurred in the issuance of long-term debt, including legal fees, bank fees, and accounting and consulting costs that have been capitalized and are being amortized on the straight-line basis over the term of the related long-term debt. Capital Assets The Medical Center’s capital assets are reported at cost. Depreciation is recorded on a straight-line basis over the estimated useful lives of the assets. Equipment under capital lease is amortized over the shorter period of the lease term or the estimated useful life of the equipment. Lease amortization is included in depreciation and amortization expense. The range of the estimated useful lives for buildings and land improvements is 10 to 40 years and for equipment is 5 to 20 years. Interest on borrowings to finance facilities is capitalized during construction. University guidelines mandate that land purchased with Medical Center funds be recorded as an asset of the Medical Center. Land utilized by the Medical Center but purchased with other sources of funds is recorded as an asset of the University. Net Assets Net assets are required to be classified for accounting and reporting purposes in the following categories:

• Invested in capital assets, net of related debt – Capital assets, net of accumulated

depreciation, reduced by outstanding principal balances of debt attributable to the acquisition, construction or improvement of those assets.

• Restricted – The Medical Center classifies net assets resulting from transactions with

purpose restrictions as restricted net assets until the resources are used for the specific purpose or for as long as the provider requires the resources to remain intact.

• Nonexpendable – Net assets subject to externally imposed restrictions that must be

retained in perpetuity by the Medical Center. • Expendable – Net assets whose use by the Medical Center is subject to externally

imposed restrictions that can be fulfilled by actions of the Medical Center pursuant to those restrictions or that expire by the passage of time.

• Unrestricted – Net assets that are neither restricted nor invested in capital assets, net of

related debt. Unrestricted net assets may be designated for specific purposes by management or The Regents. Substantially all unrestricted net assets are allocated for operating initiatives or programs, or for capital programs.

University of California, Los Angeles Medical Center Notes to Financial Statements (Dollars in thousands)

22

2. Summary of Significant Accounting Policies (Continued)

Revenues and Expenses Revenues received in conducting the programs and services of the Medical Center are presented in the financial statements as operating revenue. Operating revenue includes net patient service revenue reported at the estimated net realizable amounts from patients, third-party payors including Medicare and Medi-Cal, and others for services rendered, including estimated retroactive audit adjustments under reimbursement agreements with third-party payors. Retroactive adjustments are accrued on an estimated basis in the period the related services are rendered and adjusted in future periods as final settlements are determined. Laws and regulations governing the Medicare and Medi-Cal programs are extremely complex and subject to interpretation. As a result, there is at least a reasonable possibility that recorded estimates will change by a material amount in the near term. Substantially all of the Medical Center’s operating expenses are directly or indirectly related to patient care activities. Non-operating revenue and expense includes interest income and expense, replacement hospital transition expenses and the gain or loss on the disposal of capital assets. The replacement hospital transition expense is composed primarily of salary and consulting expenses related to the planning, coordination and logistics of moving to the replacement hospitals. State capital appropriations, health system support, proceeds received or receivable from Federal Emergency Management Agency (FEMA), donated assets and other transactions with the University are classified as other changes in net assets. Charity Care The Medical Center provides care to patients who meet certain criteria under its charity care policy without charge or at amounts less than its established rates. Amounts determined to qualify as charity care are not reported as net patient service revenue. The Medical Center also provides services to other indigent patients under publicly sponsored programs, which may reimburse at amounts less than the cost of the services provided to the recipients. The difference between the cost of services provided to these indigent persons and the expected reimbursement is included in the estimated cost of charity care. Transactions with the University and University Affiliates The Medical Center has various transactions with the University and University affiliates. The University, as the primary reporting entity, has at its discretion the ability to transfer funds from the Medical Center at will (subject to certain restrictive covenants or bond indentures) and use those funds at its discretion. The Medical Center records expense transactions where direct and incremental economic benefits are received by the Medical Center. Those payments, which constitute subsidies or payments for which the Medical Center does not receive direct and incremental economic benefit, are recorded as health system support in the statements of revenues, expenses and changes in net assets.

University of California, Los Angeles Medical Center Notes to Financial Statements (Dollars in thousands)

23

2. Summary of Significant Accounting Policies (Continued)

Transactions with the University and University Affiliates (Continued) Certain expenses are allocated from the University to the Medical Center. Allocated expenses reported as operating expenses in the statements of revenues, expenses, and changes in net assets are management’s best estimates of the Medical Center’s arms-length payment of such amounts for its market specific circumstances. To the extent that payments to the University exceed an arms-length estimated amount relative to the benefit received by the Medical Center, they are recorded as health system support. Compensated Absences The Medical Center accrues annual leave for employees at rates based upon length of service and job classification and compensatory time based upon job classification and hours worked. Tax Exemption The Regents of the University of California is a California public corporation and is a tax-exempt organization under the provisions of the Internal Revenue Code. Use of Estimates The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenditures during the reporting period. Actual amounts could differ from those estimates. New Accounting Pronouncements In August 2004, the GASB issued Statement No. 45, Accounting and Financial Reporting by Employers for Postemployment Benefits Other Than Pensions, effective for the Medical Center’s fiscal year beginning July 1, 2007. Statement No. 45 requires accrual-based measurement recognition and disclosure of other postemployment benefit (“OPEB”) expense, such as retiree medical and dental costs, over the employees’ years of service, along with the related liability, net of any plan assets. The Medical Center is currently evaluating the effect that Statement No. 45 will have on its financial statements. In June 2005, the GASB issued Statement No. 47, Accounting for Termination Benefits, effective for the Medical Center’s fiscal year beginning July 1, 2005. Statement No. 47 requires benefits such as early retirement incentives or severance to employees who are involuntarily terminated to be recognized in the period the Medical Center becomes obligated to provide the benefits. Benefits provided to employees who voluntarily terminate must be recognized when the termination offer is accepted. The Medical Center is currently evaluating the effect that Statement No. 47 will have on its financial statements.

University of California, Los Angeles Medical Center Notes to Financial Statements (Dollars in thousands)

24

3. Net Patient Service Revenue

The Medical Center has agreements with third-party payors that provide for payments at amounts different from the Medical Center’s established rates. A summary of the payment arrangements with major third-party payors follows:

• Medicare – Medicare patient revenues include traditional reimbursement under Title

XVIII of the Social Security Act (non-risk) or Medicare capitated contract revenue (risk).

Inpatient acute care services rendered to Medicare program beneficiaries are paid at prospectively determined rates per discharge. These rates vary according to a patient classification system that is based on clinical, diagnostic and other factors. Inpatient non-acute services, certain outpatient services and medical education costs related to Medicare beneficiaries are paid based, in part, on a cost reimbursement methodology. Medicare reimburses hospitals for covered outpatient services rendered to its beneficiaries by way of an outpatient prospective payment system based on ambulatory payment classifications. The Medical Center does not believe that there are significant credit risks associated with this government agency. The Medical Center is reimbursed for cost reimbursable items at a tentative rate with final settlement of such items determined after submission of annual cost reports and audits thereof by the Medicare fiscal intermediary. The Medical Center’s classification of patients under the Medicare program and the appropriateness of their admission are subject to an independent review by a peer review organization. The Medical Center hospitals’ (the UCLA Medical Center, the Santa Monica – UCLA Medical Center, and the Neuropsychiatric Hospital) Medicare cost reports have been audited by the Medicare fiscal intermediary through June 30, 2001.

• Medi-Cal –The federal Medicaid program is referred to as Medi-Cal in California.

Inpatient services rendered to Medi-Cal program beneficiaries are reimbursed under a contract at a prospectively determined negotiated per-diem rate. Outpatient services are reimbursed based upon prospectively determined fee schedules. Medi-Cal patient revenues include traditional reimbursement under the California State Department of Health Services for patients covered under Title XIX of the Social Security Act (non-risk).

• Medical Education Fund – The Medical Education Fund provides for a supplemental

payment in recognition of both direct and indirect medical education costs associated with inpatient health care services rendered to Medi-Cal beneficiaries. For the years ended June 30, 2005 and 2004, the Medical Center recorded additional revenue of $22,530 and $13,960, respectively.

• Assembly Bill 915 – State of California Assembly Bill 915 (“AB 915”), Public Hospital

Outpatient Services Supplemental Reimbursement Program, provides for supplemental reimbursement equal to the federal share of unreimbursed facility costs incurred by public hospital outpatient departments. This supplemental payment, which was approved for implementation on September 12, 2003, covers only Medi-Cal fee-for-service outpatient services, beginning July 1, 2002. The supplemental payment is based on each eligible hospital’s certified public expenditures (“CPE”), which are matched with

University of California, Los Angeles Medical Center Notes to Financial Statements (Dollars in thousands)

25

3. Net Patient Service Revenue (Continued)

federal Medicaid funds. For the years ended June 30, 2005 and 2004, the Medical Center recorded additional revenue of $3,975 and $6,384, respectively. The $6,384 recorded by the Medical Center in the year ended June 30, 2004 was for two years of patient services rendered from July 1, 2002 through June 30, 2004.

• Other – The Medical Center has entered into agreements with numerous non-

government third-party payors to provide patient care to beneficiaries under a variety of payment arrangements. These include arrangements with:

• Commercial insurance companies reimburse the Medical Center for reasonable

and customary charges. Workers’ compensation plans pay negotiated rates and are reported as contract (discounted or per-diem).

• Managed care contracts such as those with HMO’s and PPO’s, which reimburse

the Medical Center at contracted or per-diem rates, which are usually less than full charges.

• Capitated contracts with health plans, which reimburse the Medical Center on a

per-member-per-month basis, whether or not services are actually rendered. The Medical Center takes on a certain amount of financial risk as the contract requires them to treat a patient for all covered services. Expected losses on capitated agreements are accrued when probable and can be reasonably estimated.

• Certain health plans established a shared-risk pool through which the Medical

Center shares in any surplus of budget over actual health care utilization costs as defined in the related contracts. Additionally, the Medical Center bears risk of health care utilization cost above budgeted cost, as determined in the related agreements. Differences between the final contract settlement and the amount estimated as receivable or payable relating to the shared-risk arrangements are recorded in the year of final settlement.

• Counties in the State of California, which reimburse the Medical Center for

certain indigent patients covered under county contracts.

The most common payment for inpatient services is a prospectively determined per-diem rate. The most common payment arrangement for outpatient care is a prospective payment system that uses ambulatory payment classifications. Amounts due from Medicare and Medi-Cal represent 28.0% and 24.0% of net patient accounts receivable at June 30, 2005 and 2004, respectively. For the years ended June 30, 2005 and 2004, net patient service revenue included $3,000 and $7,424, respectively, due to favorable cost report settlements with Medicare and Medi-Cal.

University of California, Los Angeles Medical Center Notes to Financial Statements (Dollars in thousands)

26

3. Net Patient Service Revenue (Continued)

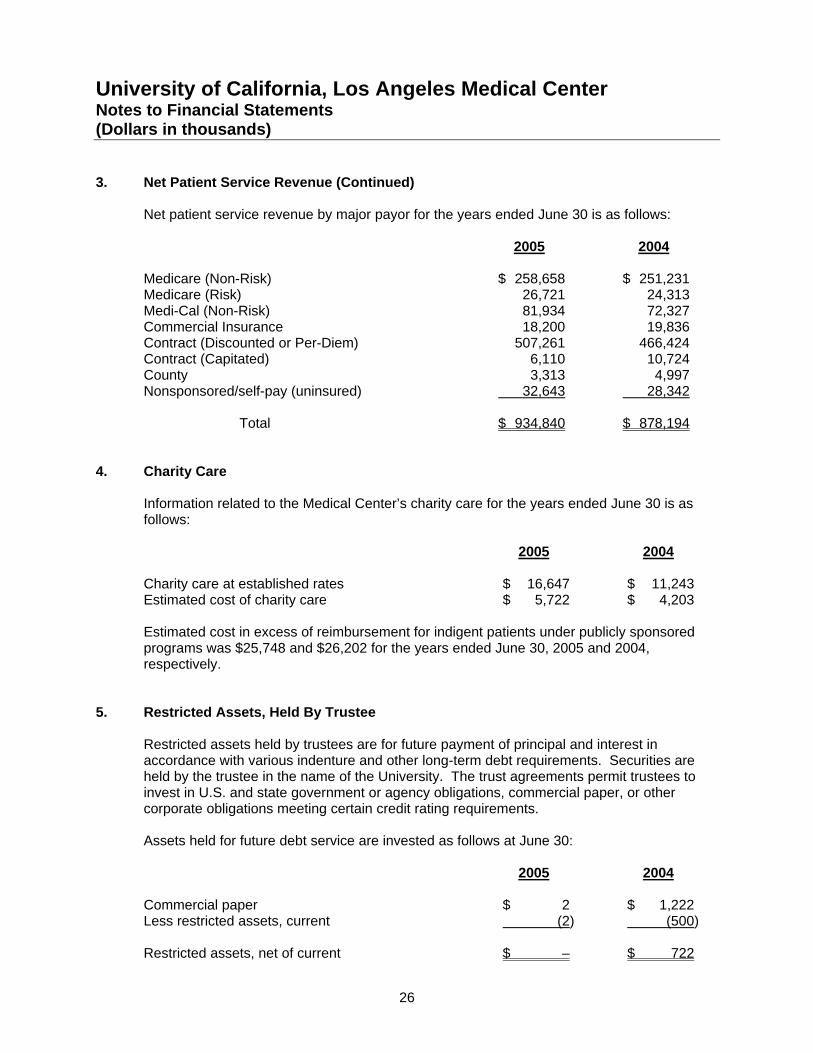

Net patient service revenue by major payor for the years ended June 30 is as follows:

2005 2004 Medicare (Non-Risk) $ 258,658 $ 251,231 Medicare (Risk) 26,721 24,313 Medi-Cal (Non-Risk) 81,934 72,327 Commercial Insurance 18,200 19,836 Contract (Discounted or Per-Diem) 507,261 466,424 Contract (Capitated) 6,110 10,724 County 3,313 4,997 Nonsponsored/self-pay (uninsured) 32,643 28,342 Total $ 934,840 $ 878,194

4. Charity Care

Information related to the Medical Center’s charity care for the years ended June 30 is as follows:

2005 2004 Charity care at established rates $ 16,647 $ 11,243 Estimated cost of charity care $ 5,722 $ 4,203

Estimated cost in excess of reimbursement for indigent patients under publicly sponsored programs was $25,748 and $26,202 for the years ended June 30, 2005 and 2004, respectively.

5. Restricted Assets, Held By Trustee

Restricted assets held by trustees are for future payment of principal and interest in accordance with various indenture and other long-term debt requirements. Securities are held by the trustee in the name of the University. The trust agreements permit trustees to invest in U.S. and state government or agency obligations, commercial paper, or other corporate obligations meeting certain credit rating requirements. Assets held for future debt service are invested as follows at June 30:

2005 2004 Commercial paper $ 2 $ 1,222 Less restricted assets, current (2) (500) Restricted assets, net of current $ – $ 722

University of California, Los Angeles Medical Center Notes to Financial Statements (Dollars in thousands)

27

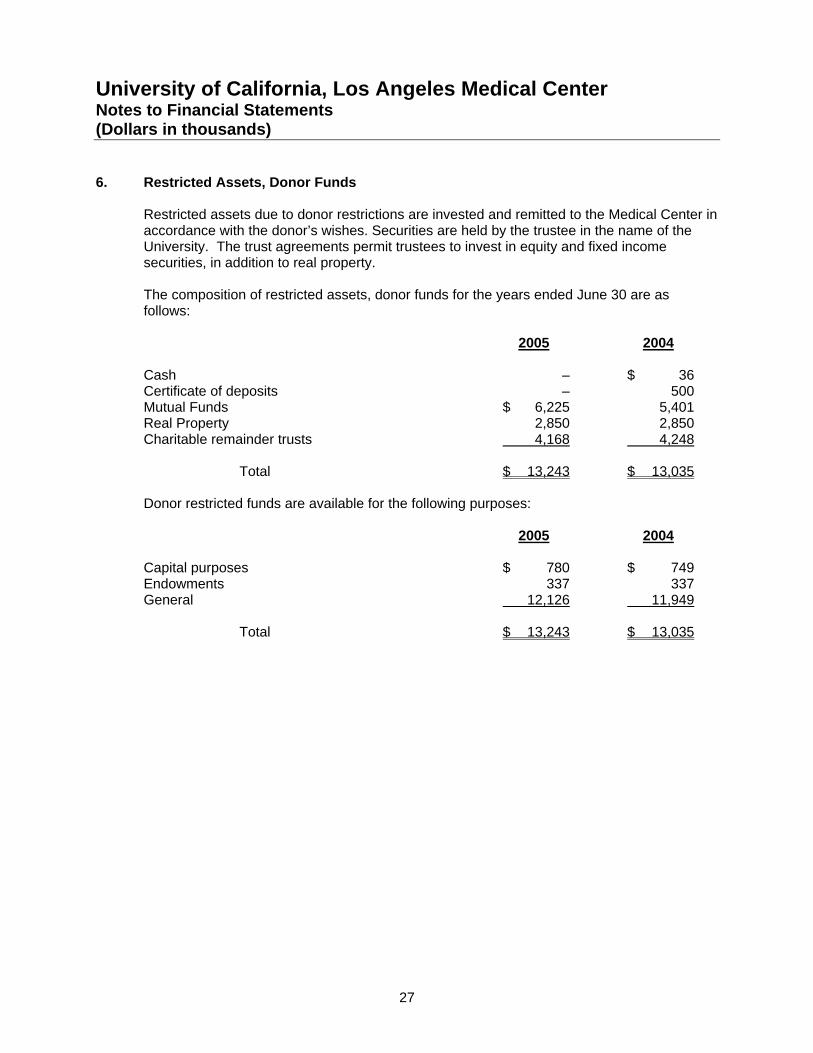

6. Restricted Assets, Donor Funds

Restricted assets due to donor restrictions are invested and remitted to the Medical Center in accordance with the donor’s wishes. Securities are held by the trustee in the name of the University. The trust agreements permit trustees to invest in equity and fixed income securities, in addition to real property. The composition of restricted assets, donor funds for the years ended June 30 are as follows:

2005 2004 Cash – $ 36 Certificate of deposits – 500 Mutual Funds $ 6,225 5,401 Real Property 2,850 2,850 Charitable remainder trusts 4,168 4,248 Total $ 13,243 $ 13,035

Donor restricted funds are available for the following purposes:

2005 2004 Capital purposes $ 780 $ 749 Endowments 337 337 General 12,126 11,949 Total $ 13,243 $ 13,035

University of California, Los Angeles Medical Center Notes to Financial Statements (Dollars in thousands)

28

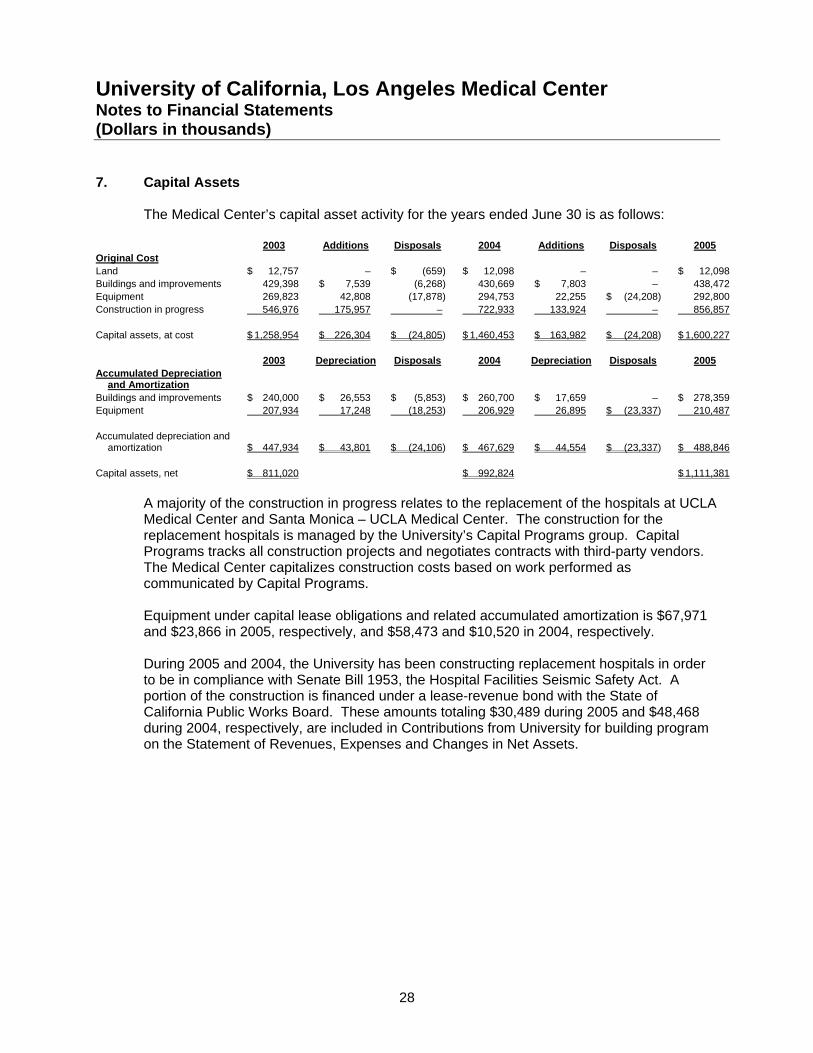

7. Capital Assets

The Medical Center’s capital asset activity for the years ended June 30 is as follows: 2003 Additions Disposals 2004 Additions Disposals 2005 Original Cost Land $ 12,757 – $ (659) $ 12,098 – – $ 12,098 Buildings and improvements 429,398 $ 7,539 (6,268) 430,669 $ 7,803 – 438,472 Equipment 269,823 42,808 (17,878) 294,753 22,255 $ (24,208) 292,800 Construction in progress 546,976 175,957 – 722,933 133,924 – 856,857 Capital assets, at cost $ 1,258,954 $ 226,304 $ (24,805) $ 1,460,453 $ 163,982 $ (24,208) $ 1,600,227 2003 Depreciation Disposals 2004 Depreciation Disposals 2005 Accumulated Depreciation

and Amortization Buildings and improvements $ 240,000 $ 26,553 $ (5,853) $ 260,700 $ 17,659 – $ 278,359 Equipment 207,934 17,248 (18,253) 206,929 26,895 $ (23,337) 210,487 Accumulated depreciation and

amortization $ 447,934 $ 43,801 $ (24,106) $ 467,629 $ 44,554 $ (23,337) $ 488,846 Capital assets, net $ 811,020 $ 992,824 $ 1,111,381

A majority of the construction in progress relates to the replacement of the hospitals at UCLA Medical Center and Santa Monica – UCLA Medical Center. The construction for the replacement hospitals is managed by the University’s Capital Programs group. Capital Programs tracks all construction projects and negotiates contracts with third-party vendors. The Medical Center capitalizes construction costs based on work performed as communicated by Capital Programs. Equipment under capital lease obligations and related accumulated amortization is $67,971 and $23,866 in 2005, respectively, and $58,473 and $10,520 in 2004, respectively. During 2005 and 2004, the University has been constructing replacement hospitals in order to be in compliance with Senate Bill 1953, the Hospital Facilities Seismic Safety Act. A portion of the construction is financed under a lease-revenue bond with the State of California Public Works Board. These amounts totaling $30,489 during 2005 and $48,468 during 2004, respectively, are included in Contributions from University for building program on the Statement of Revenues, Expenses and Changes in Net Assets.

University of California, Los Angeles Medical Center Notes to Financial Statements (Dollars in thousands)

29

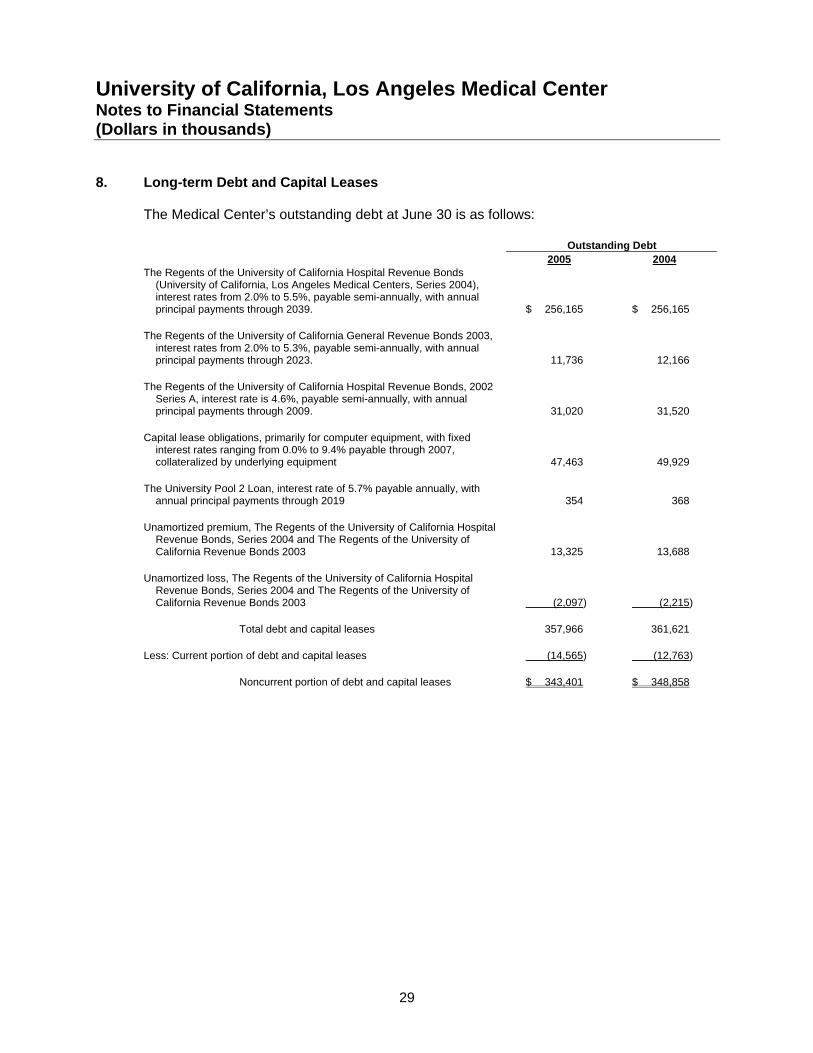

8. Long-term Debt and Capital Leases

The Medical Center’s outstanding debt at June 30 is as follows:

Outstanding Debt 2005 2004 The Regents of the University of California Hospital Revenue Bonds

(University of California, Los Angeles Medical Centers, Series 2004), interest rates from 2.0% to 5.5%, payable semi-annually, with annual principal payments through 2039. $ 256,165 $ 256,165

The Regents of the University of California General Revenue Bonds 2003,

interest rates from 2.0% to 5.3%, payable semi-annually, with annual principal payments through 2023. 11,736 12,166

The Regents of the University of California Hospital Revenue Bonds, 2002

Series A, interest rate is 4.6%, payable semi-annually, with annual principal payments through 2009. 31,020 31,520

Capital lease obligations, primarily for computer equipment, with fixed

interest rates ranging from 0.0% to 9.4% payable through 2007, collateralized by underlying equipment 47,463 49,929

The University Pool 2 Loan, interest rate of 5.7% payable annually, with

annual principal payments through 2019 354 368 Unamortized premium, The Regents of the University of California Hospital

Revenue Bonds, Series 2004 and The Regents of the University of California Revenue Bonds 2003 13,325 13,688

Unamortized loss, The Regents of the University of California Hospital

Revenue Bonds, Series 2004 and The Regents of the University of California Revenue Bonds 2003 (2,097) (2,215)

Total debt and capital leases 357,966 361,621 Less: Current portion of debt and capital leases (14,565) (12,763) Noncurrent portion of debt and capital leases $ 343,401 $ 348,858

University of California, Los Angeles Medical Center Notes to Financial Statements (Dollars in thousands)

30

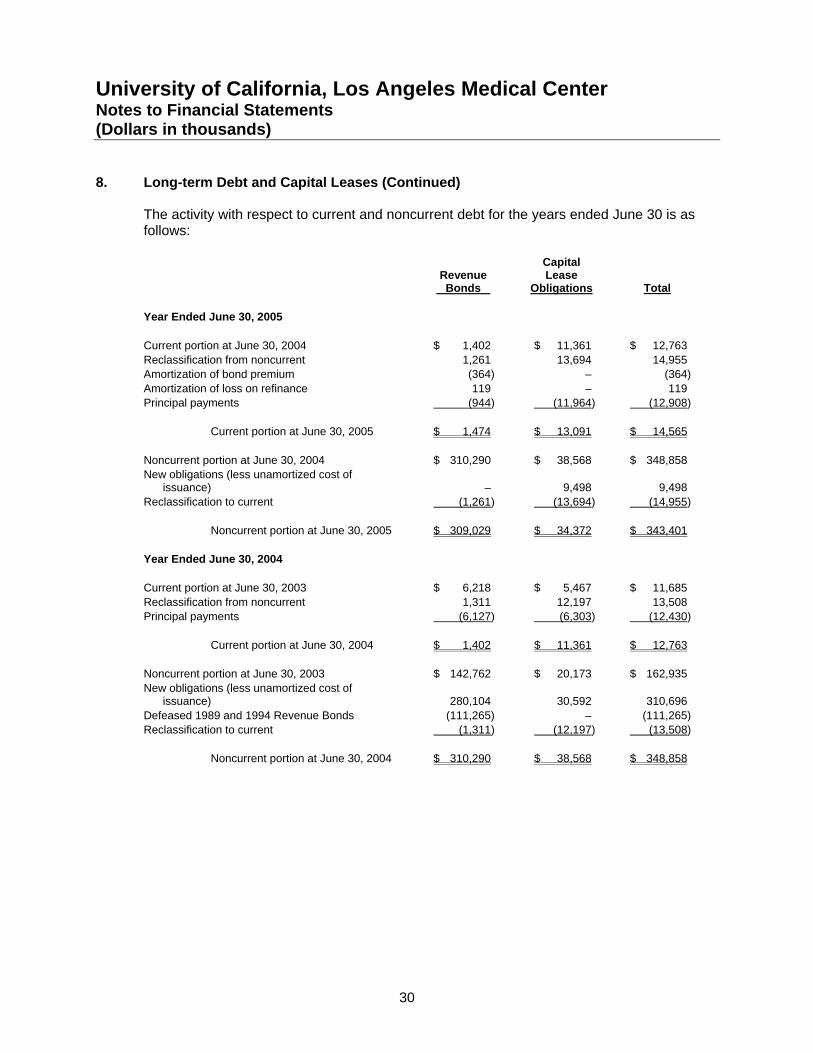

8. Long-term Debt and Capital Leases (Continued)

The activity with respect to current and noncurrent debt for the years ended June 30 is as follows:

Revenue

Bonds .

Capital Lease

Obligations Total Year Ended June 30, 2005 Current portion at June 30, 2004 $ 1,402 $ 11,361 $ 12,763 Reclassification from noncurrent 1,261 13,694 14,955 Amortization of bond premium (364) – (364) Amortization of loss on refinance 119 – 119 Principal payments (944) (11,964) (12,908) Current portion at June 30, 2005 $ 1,474 $ 13,091 $ 14,565 Noncurrent portion at June 30, 2004 $ 310,290 $ 38,568 $ 348,858 New obligations (less unamortized cost of issuance) – 9,498 9,498 Reclassification to current (1,261) (13,694) (14,955) Noncurrent portion at June 30, 2005 $ 309,029 $ 34,372 $ 343,401 Year Ended June 30, 2004 Current portion at June 30, 2003 $ 6,218 $ 5,467 $ 11,685 Reclassification from noncurrent 1,311 12,197 13,508 Principal payments (6,127) (6,303) (12,430) Current portion at June 30, 2004 $ 1,402 $ 11,361 $ 12,763 Noncurrent portion at June 30, 2003 $ 142,762 $ 20,173 $ 162,935 New obligations (less unamortized cost of issuance) 280,104 30,592 310,696 Defeased 1989 and 1994 Revenue Bonds (111,265) – (111,265) Reclassification to current (1,311) (12,197) (13,508) Noncurrent portion at June 30, 2004 $ 310,290 $ 38,568 $ 348,858

University of California, Los Angeles Medical Center Notes to Financial Statements (Dollars in thousands)

31

8. Long-term Debt and Capital Leases (Continued)

In May 2004, The Regents of the University of California issued Hospital Revenue Bonds totaling $256,165, Series A for $165,000 and Series B for $91,165, to finance a portion of the costs of constructing and equipping the replacement hospital facility for UCLA Medical Center Westwood and the replacement hospital facility for Santa Monica – UCLA Medical Center and to refund previously outstanding Hospital Revenue Bonds. The Hospital Revenue Bonds are collateralized solely by revenues of the Medical Center. In addition, under the bond indentures, the Medical Center is required to maintain a debt service ratio of 1.1 to 1 and has limitations as to additional borrowings and the purchase or sale of assets. In September 2003, the University issued General Revenue Bonds, collateralized solely by general revenues of the University, to refinance a substantial portion of the outstanding 1989 Multiple Purpose Project bonds. Certain Medical Center projects were financed with the 1989 Multiple Purpose Project bonds. As a result, Medical Center projects with outstanding debt totaling $12,929 were also refinanced. The Medical Center is charged for its proportionate share of total principal and interest payments made on the General Revenue Bonds pertaining to Medical Center projects.

The Regents of the University of California Hospital Revenue Bonds, 2002 Series A is a private placement to refinance the acquisition of Santa Monica Hospital Medical Center. The bonds are collateralized solely by revenues of the Medical Center. In addition, under the bond indentures, the Medical Center is required to maintain a debt service coverage ratio of 1.2 to 1 and has limitations as to additional borrowings and the purchase or sale of business assets. Additional information on the revenue bonds can be obtained from the 2004-2005 annual report of the University.

University of California, Los Angeles Medical Center Notes to Financial Statements (Dollars in thousands)

32

8. Long-term Debt and Capital Leases (Continued)

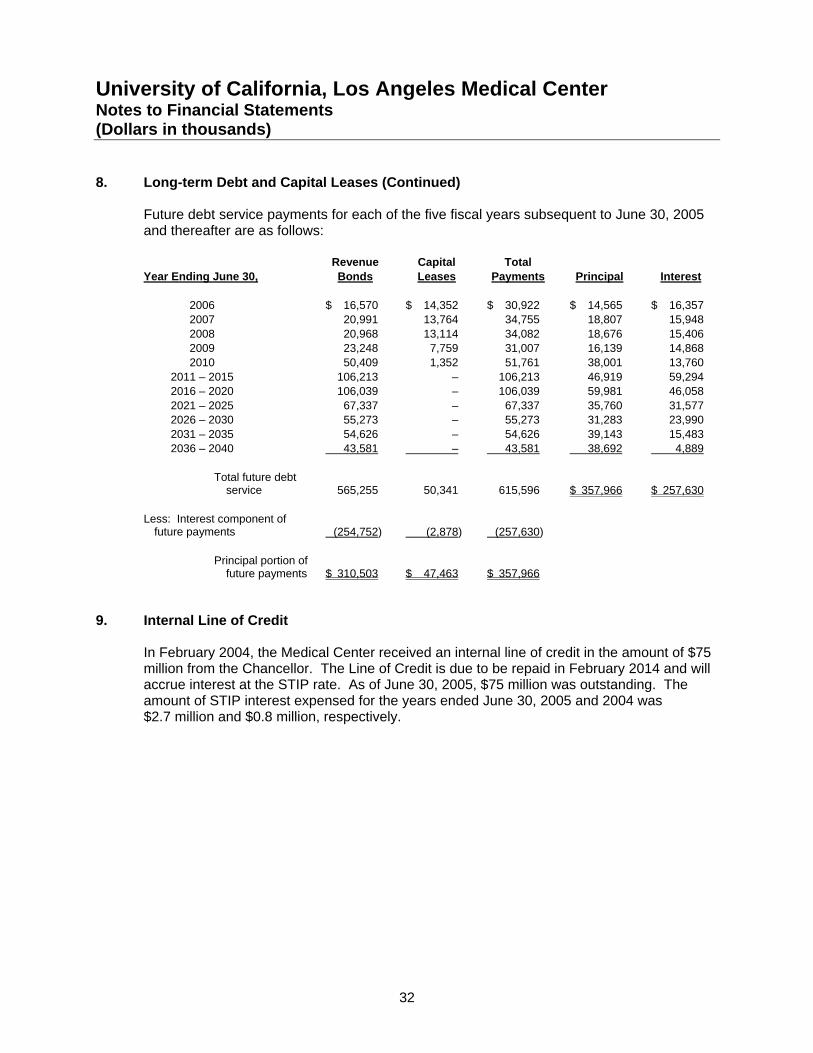

Future debt service payments for each of the five fiscal years subsequent to June 30, 2005 and thereafter are as follows:

Revenue Capital Total Year Ending June 30, Bonds Leases Payments Principal Interest 2006 $ 16,570 $ 14,352 $ 30,922 $ 14,565 $ 16,357 2007 20,991 13,764 34,755 18,807 15,948 2008 20,968 13,114 34,082 18,676 15,406 2009 23,248 7,759 31,007 16,139 14,868 2010 50,409 1,352 51,761 38,001 13,760 2011 – 2015 106,213 – 106,213 46,919 59,294 2016 – 2020 106,039 – 106,039 59,981 46,058 2021 – 2025 67,337 – 67,337 35,760 31,577 2026 – 2030 55,273 – 55,273 31,283 23,990 2031 – 2035 54,626 – 54,626 39,143 15,483 2036 – 2040 43,581 – 43,581 38,692 4,889 Total future debt service 565,255 50,341 615,596 $ 357,966 $ 257,630 Less: Interest component of future payments (254,752) (2,878) (257,630) Principal portion of future payments $ 310,503 $ 47,463 $ 357,966

9. Internal Line of Credit

In February 2004, the Medical Center received an internal line of credit in the amount of $75 million from the Chancellor. The Line of Credit is due to be repaid in February 2014 and will accrue interest at the STIP rate. As of June 30, 2005, $75 million was outstanding. The amount of STIP interest expensed for the years ended June 30, 2005 and 2004 was $2.7 million and $0.8 million, respectively.

University of California, Los Angeles Medical Center Notes to Financial Statements (Dollars in thousands)

33

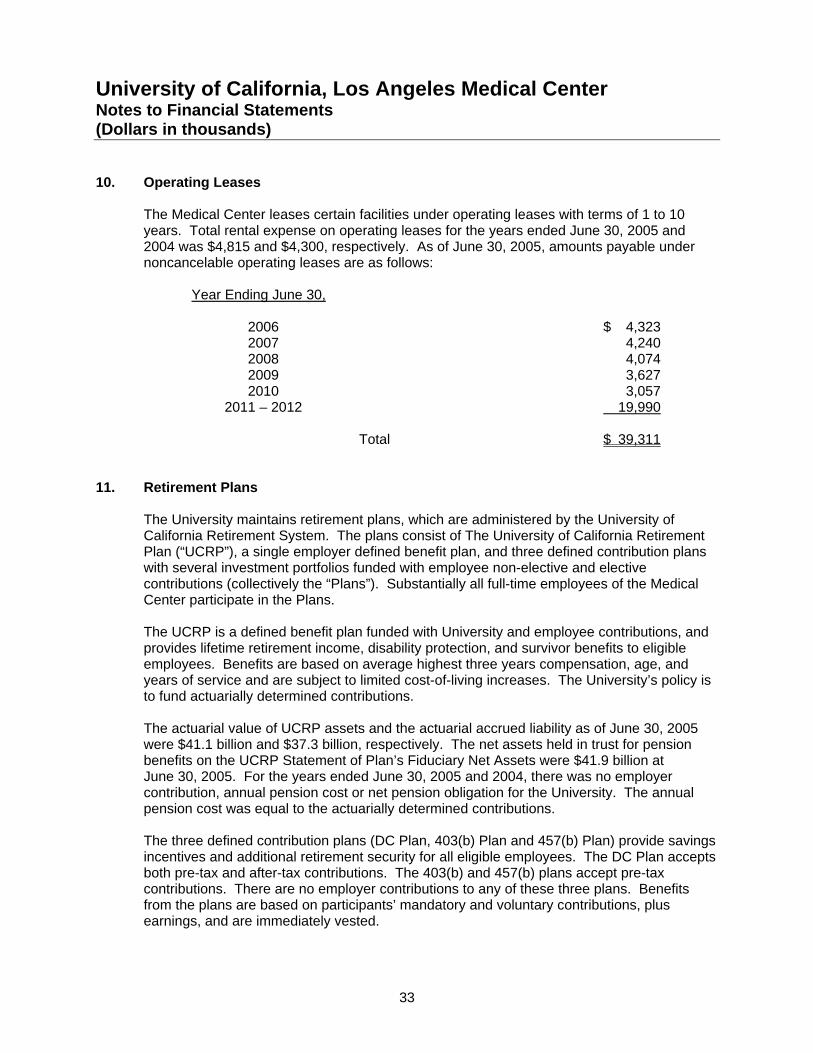

10. Operating Leases

The Medical Center leases certain facilities under operating leases with terms of 1 to 10 years. Total rental expense on operating leases for the years ended June 30, 2005 and 2004 was $4,815 and $4,300, respectively. As of June 30, 2005, amounts payable under noncancelable operating leases are as follows:

Year Ending June 30, 2006 $ 4,323 2007 4,240 2008 4,074 2009 3,627 2010 3,057 2011 – 2012 19,990 Total $ 39,311

11. Retirement Plans

The University maintains retirement plans, which are administered by the University of California Retirement System. The plans consist of The University of California Retirement Plan (“UCRP”), a single employer defined benefit plan, and three defined contribution plans with several investment portfolios funded with employee non-elective and elective contributions (collectively the “Plans”). Substantially all full-time employees of the Medical Center participate in the Plans. The UCRP is a defined benefit plan funded with University and employee contributions, and provides lifetime retirement income, disability protection, and survivor benefits to eligible employees. Benefits are based on average highest three years compensation, age, and years of service and are subject to limited cost-of-living increases. The University’s policy is to fund actuarially determined contributions. The actuarial value of UCRP assets and the actuarial accrued liability as of June 30, 2005 were $41.1 billion and $37.3 billion, respectively. The net assets held in trust for pension benefits on the UCRP Statement of Plan’s Fiduciary Net Assets were $41.9 billion at June 30, 2005. For the years ended June 30, 2005 and 2004, there was no employer contribution, annual pension cost or net pension obligation for the University. The annual pension cost was equal to the actuarially determined contributions. The three defined contribution plans (DC Plan, 403(b) Plan and 457(b) Plan) provide savings incentives and additional retirement security for all eligible employees. The DC Plan accepts both pre-tax and after-tax contributions. The 403(b) and 457(b) plans accept pre-tax contributions. There are no employer contributions to any of these three plans. Benefits from the plans are based on participants’ mandatory and voluntary contributions, plus earnings, and are immediately vested.

University of California, Los Angeles Medical Center Notes to Financial Statements (Dollars in thousands)

34

11. Retirement Plans (Continued)

Information as to contributions made, plan assets and liabilities, as they relate to Medical Center employees, is not readily available. Additional information on the plans can be obtained from the 2004-2005 annual report of the University.

12. University Self-Insurance

The Medical Center is insured through the University’s malpractice, general liability, workers’ compensation, and health and welfare self-insurance programs. All operating departments of the University are charged premiums to finance the workers’ compensation and health and welfare programs. The University’s medical centers are charged premiums to finance the malpractice insurance. All claims and related expenses are paid from the University’s self-insurance funds. Such risks are subject to various per claim and aggregate limits, with excess liability coverage provided by an independent insurer. The Medical Center is contingently liable for the obligations under these self-insurance programs.

The Medical Center paid premiums of $22,582 and $19,211 for the years ended June 30, 2005 and 2004, respectively. These amounts are included in salaries and employee benefits, and insurance on the statement of revenues, expenses and changes in net assets.

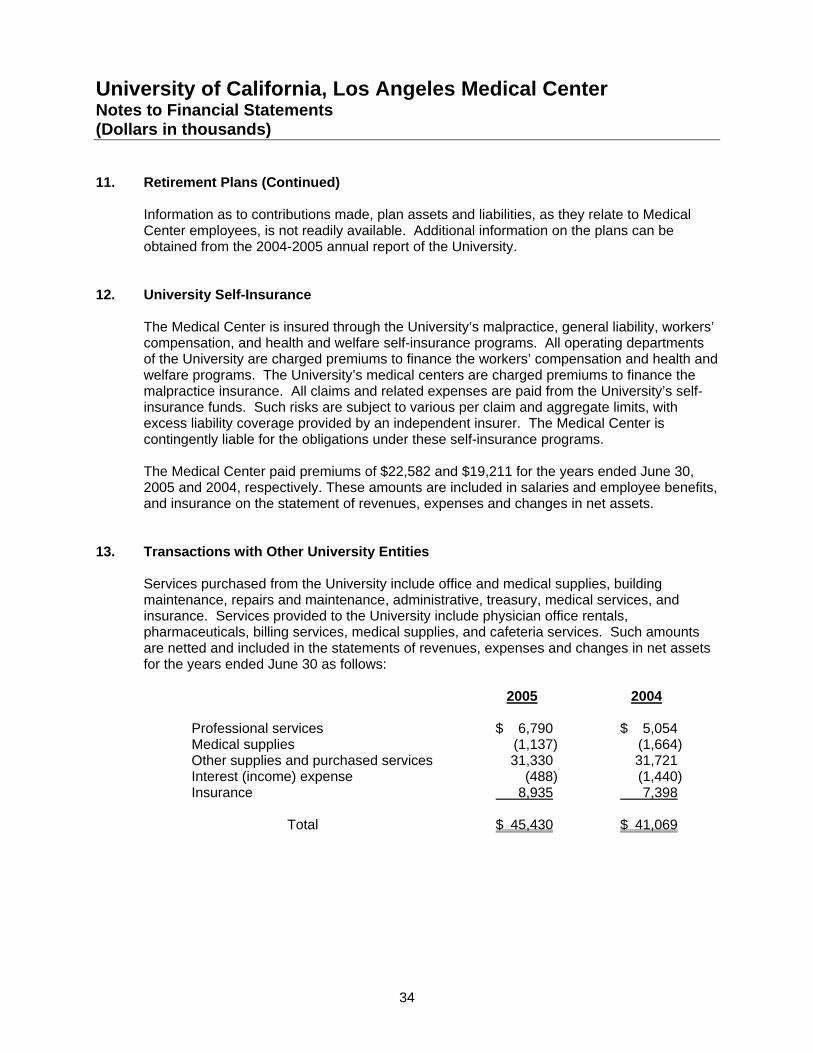

13. Transactions with Other University Entities

Services purchased from the University include office and medical supplies, building maintenance, repairs and maintenance, administrative, treasury, medical services, and insurance. Services provided to the University include physician office rentals, pharmaceuticals, billing services, medical supplies, and cafeteria services. Such amounts are netted and included in the statements of revenues, expenses and changes in net assets for the years ended June 30 as follows:

2005 2004 Professional services $ 6,790 $ 5,054 Medical supplies (1,137) (1,664) Other supplies and purchased services 31,330 31,721 Interest (income) expense (488) (1,440) Insurance 8,935 7,398 Total $ 45,430 $ 41,069

University of California, Los Angeles Medical Center Notes to Financial Statements (Dollars in thousands)

35

13. Transactions with Other University Entities (Continued)

Additionally, the Medical Center makes payments to the University of California, Los Angeles School of Medicine (“School of Medicine”). Services purchased from the School of Medicine include physician services that benefit the Medical Center, such as emergency room coverage, physicians providing medical direction to the Medical Center, and the Medical Center’s allocation of malpractice insurance. Such expenses are reported as operating expenses in the statements of revenue, expenses and changes in net assets. Health system support includes amounts paid by the Medical Center to fund School of Medicine operating activities, payments to support clinical research, transfers to faculty practice plans, as well as other payments made to support various School of Medicine programs.

The total net amounts of payments made by the Medical Center to the School of Medicine were $69,502 and $73,086 in 2005 and 2004, respectively. Of these amounts, $45,430 and $41,069 are reported as operating expenses for the years ended June 30, 2005 and 2004, respectively, and $24,072 and $32,017 are reported as health system support for the years ended June 30, 2005 and 2004, respectively.

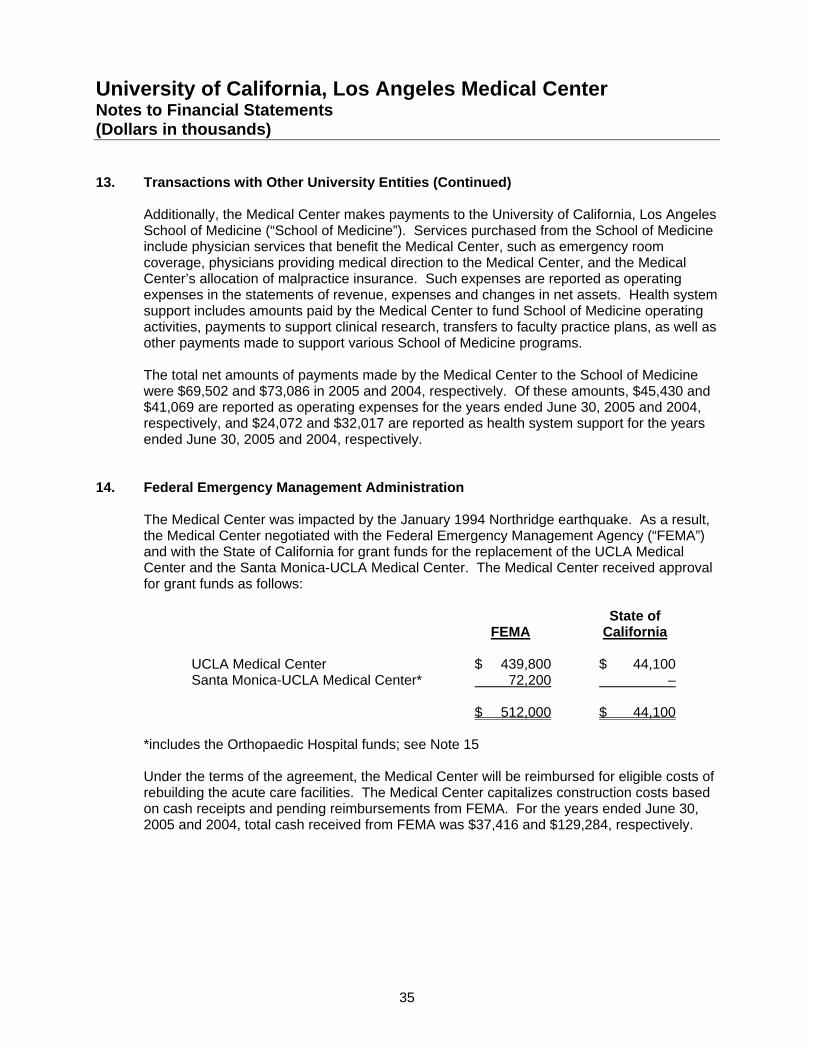

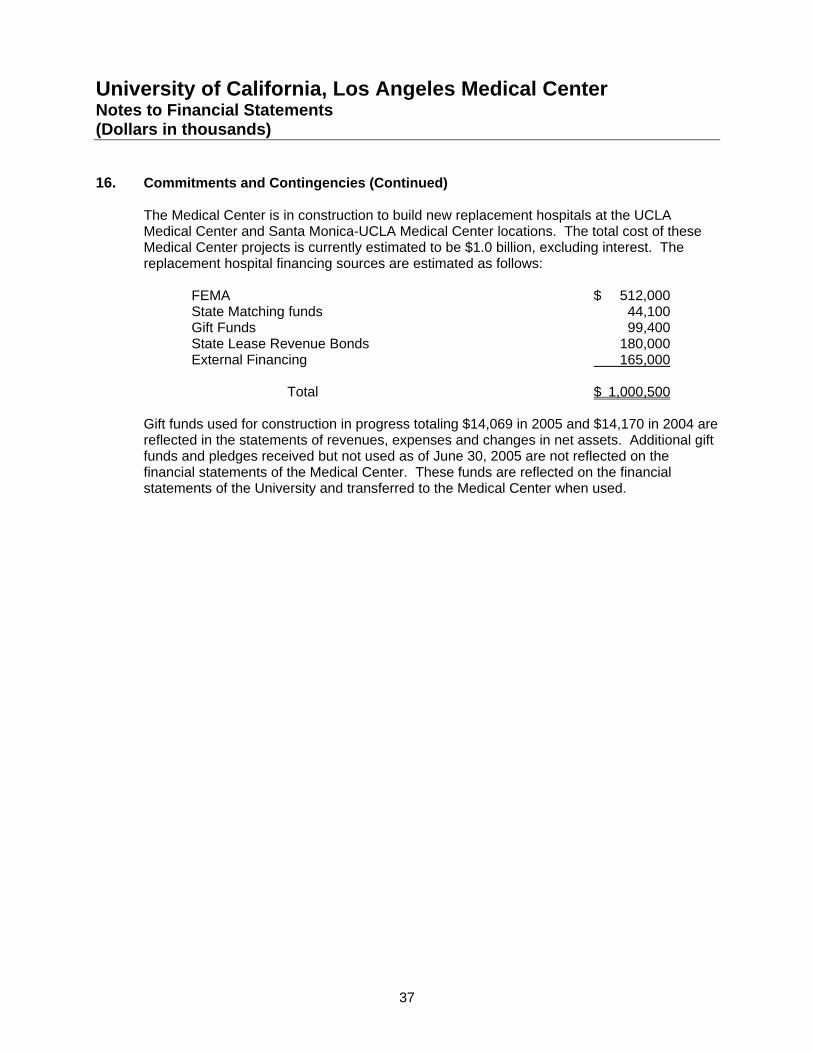

14. Federal Emergency Management Administration