Embed Size (px)

Citation preview

MIKE SULLIVAN GOVERNOR

STATE OF WYOMING OFFICE OF THE GOVERNOR

CHEYENNE 82002

December 30, 1988

TO: MEMBERS OF THE FIFTIETH WYOMING LEGISLATURE

I am pleased to submit this report of the Joint Legislative-Executive Government Efficiency Study Committee as required by Chapter 57, Wyoming Session Laws, 1988.

After several months of intense study by the Committee and valuable input from both executive and legislative branch representatives, as well as the business and general citizenry of the State, the Committee's findings and recommendations are outlined. As the law requires, this report is accompanied by legislation and constitutional amendments for your consideration which are necessary to implement these recommendations.

In my opinion, you have made a wise and prudent decision in funding this study as many of the recommendations it contains, if implemented, will provide a lasting benefit to the citizens of this State. The release of the GnMA and FHLMC securities, in itself, will make available some $50 million in resources, which was facilitated by the Committee's investigation and analysis. Other recommendations, though perhaps more controversial or difficult, should nonetheless be considered, discussed and assessed in terms of their long-term fiscal and administrative benefits.

I have expressed on previous occasions, my desire to make government more efficient and believe that many of the recommendations contained in this report will advance that cause. The reorganization plan outlined herein represents a gradual transition from the current structure which has served Wyoming since its statehood. Technological, sociological, economical and other changes which we have experienced lend argument to the fact that we must adjust and adapt in order to meet the challenges of today and the future.

I wish you success in your deliberations of this important issue.

Very truly yours,

~~ Mike Sullivan

COMMIITEE: Sen. John Perry Sen. Alvin Wiederspahn Rep. Craig Thomas Rep. Bill Rohrbach Robert Pettigrew, Jr.,

Chairman Paul Cleary Frank Galeotos Rodger McDaniel

401 W.19th • Sulte303 Cheyetme, Wyoming 82001 (307) 777.fiiJ70

:Joint Leg ii.fatiue - Executiue

c::Etate § oue 'tnment E({iciency

c::Etudlj Committee

December 20, 1988

Honorable Mike Sullivan Governor of Wyoming Capitol Building Cheyenne, WY 82002

Dear Governor Sullivan:

MIKE SULLIVAN Governor

.JOHN F. TURNER President of the Senate

PATRICK H. MEENAN Speaker of the House

It is with a deep sense of satisfaction that I submit this Report of the Joint Legislative-Executive Efficiency Study Committee.

The charge given this Committee was not a small one. This became quickly apparent as study and research brought into focus the magnitude of the project.

As Chairman, I cannot adequately express my admiration and appreciation for the personal dedication and tireless efforts so freely given by Committee members, state officials and employees, the University of Wyoming, and countless citizens of the State.

I would particularly like to express my appreciation to the Ferrari Group, Consultants to the Committee. Their professional abilities have been invaluable to this effort. Without the sense of devotion and total commitment to the people of Wyoming of Dave Ferrari, Ruth Sommers, and Jan Washburn, our task would have been a great deal more difficult, if not impossible.

Sincerely,

e~~grew,J. Chairman

A Study in State Government

Efficiency

Joint Legislative-Executive Efficiency Study Committee

Robert L. Pettigrew, Jr., Chairman Senator John Perry

Senator Alvin Wiederspahn Representative Craig Thomas Representative Bill Rohrbach

Paul Cleary Frank Galeotos

Rodger McDaniel

- iii -

ACKNOWLEDGMENTS

The Joint Legislative-Executive Committee is greatful for the efforts and contributions of those who provided input to this study.

The State Library was instrumental in providing research data and support to the Committee throughout the project. The staff responded quickly and professionally to requests for documents and information. Without such prompt courtesies, the Committee's work would have been exceedingly more difficult.

The Committee wishes to expressly thank Mr. Joe Meyer, Attorney General, for his personal attention to the details of portions of the study and for the unselfish dedication of many of his staff. Ms. Sylvia Hackl, Ms. Rowena Heckert, Ms. Vicci Colgan, Mr. Dennis Cook, Ms. Barbara Boyer, Mr. John Renneisen, Ms. Mary Guthrie, and Mr. Pete Mulvaney devoted many hours to researching statutes, annual reports and agency budget documents in an effort to define agency programs, services and responsibilities. Their conscientious review and analysis provided the Committee with invaluable information which otherwise would have been extremely difficult to obtain.

The Committee would also like to thank the State's five elected officials for their time and attention to the study. Governor Sullivan's guidance and support of the project and considerable time given for briefings and discussions were especially meaningful. Secretary of State, Kathy Karpan, provided the Committee with unusual insight into the operations of the Board of Charities and Reform, the Department of Health and Social Services, and the operations of her office, as did State Auditor, Jack Sidi. Mr. Sidi's insight into the State's various auditing and budgeting efforts was also greatly appreciated. State treasurer, Stan Smith, and his staff were extremely helpful in providing information and advice on the State's investment program.

Mr. Rick Miller, Director of the Legislative Service Office, contributed numerous hours to the drafting of legislation for the Committee and provided a steady guiding hand in the early stages of the project. The Committee is especially appreciative for his input and counsel.

Many hours were spent by members of the Governor's staff in reviewing drafts, discussing issues, and providing expertise on various portions of the study. Ms. Nancy Freudenthal, Mr. Ernie Mecca, Dr. Pete Maxfield, and Mr. Leonard Bucsanyi were all extremely helpful.

The Committee would also like to thank all of the legislators and state government executive branch officials and employees who took the time to provide input and information. The task of assimilating much of this input data was accomplished by Phill Harris in the Budget Division of the Department of Administration and Fiscal Control. Without their patience and assistance, the Committee could not have completed this project in a timely or meaningful manner.

- iv-

CONTENTS

CHAPTER

I INTRODUCTION AND OVERVIEW ........................... .. • State Government Efficiency Study ............................. . • Consolidation of Funds and Analysis of Pooled Interest .......... . • Investment Program and Cash Management Techniques .......... . • Reorganization of the State's Administrative Structure ............ . • In Summary ................................................. .

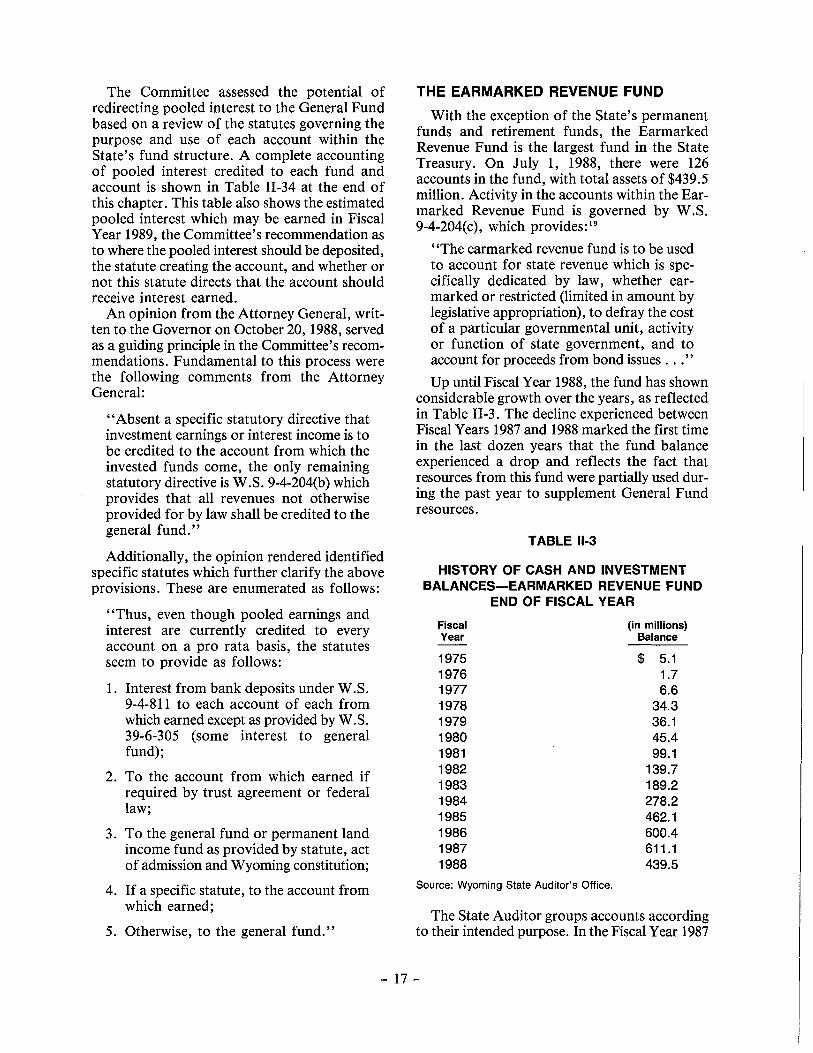

II FUND CONSOLIDATION AND POOLED INTEREST ............ . • The Impact of Earmarking ..................................... . • The General Fund ............................................ . • The Earmarked Revenue Fund ................................. .

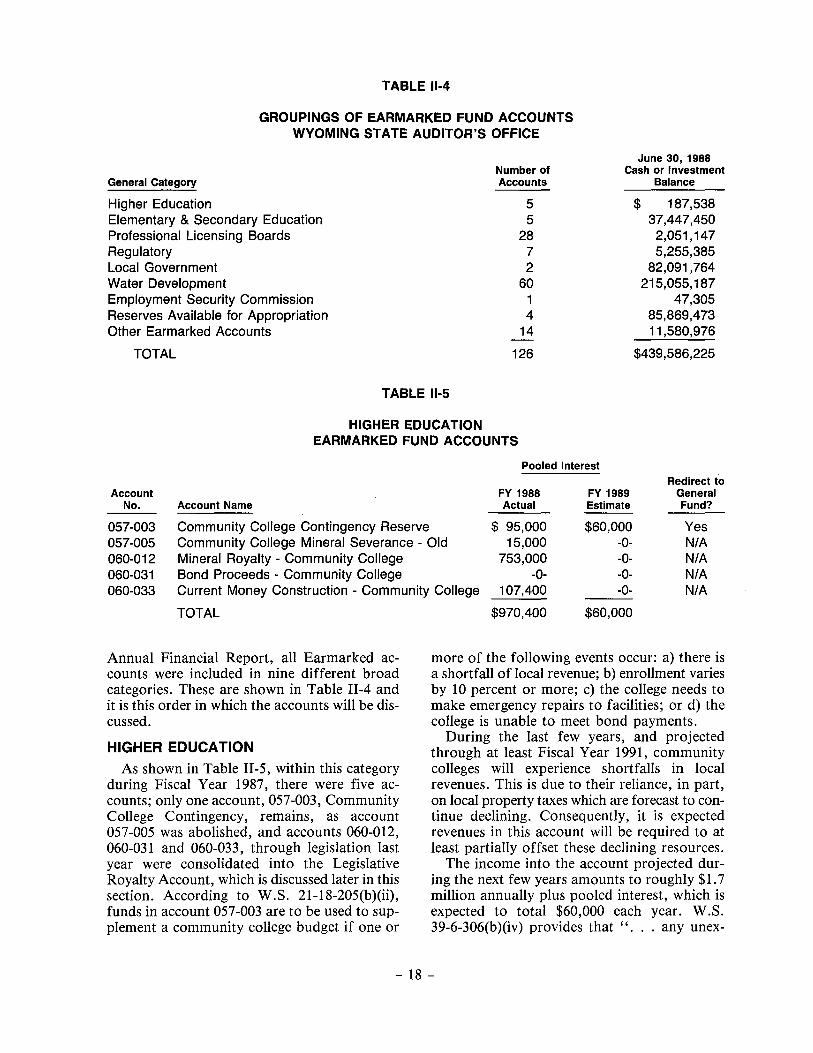

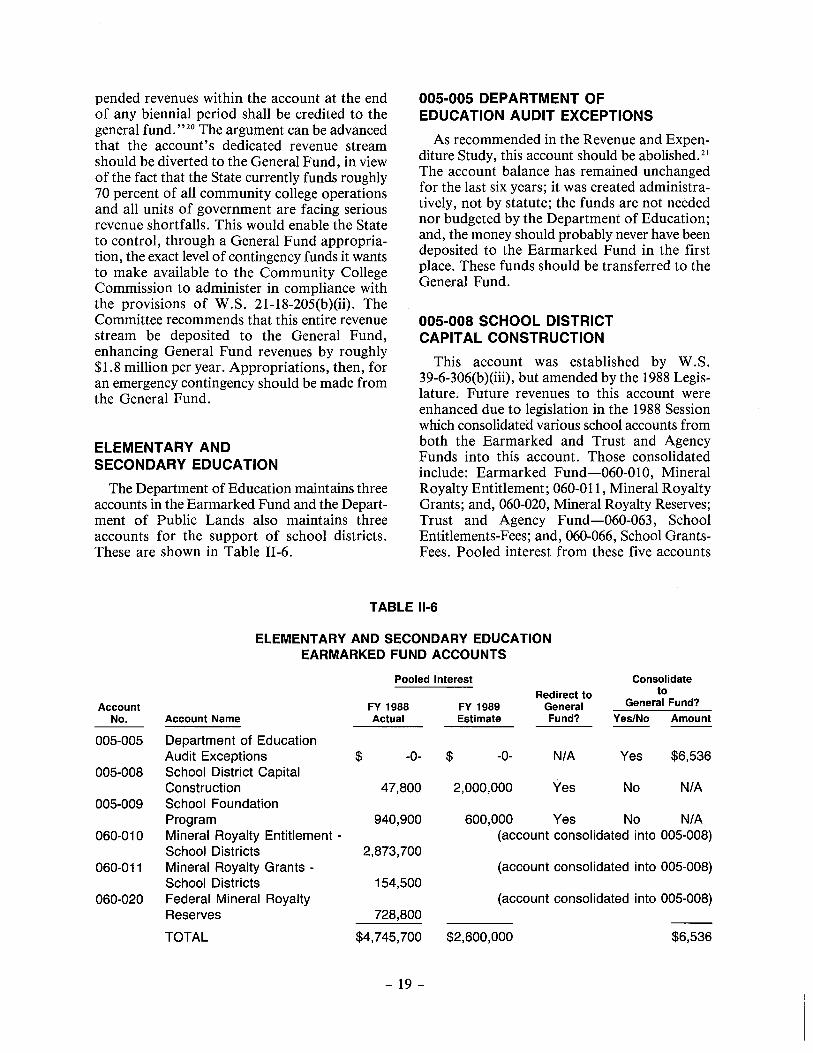

Higher Education ............................................ . Elementary and Secondary Education ........................... . Professional Licensing Boards ................................. . Regulatory Boards and Commissions ........................... . Local Government ........................................... . Water Development Accounts ................................. . Employment Security Commission ............................. . Reserves Available for Appropriation ........................... . Other Earmarked Accounts .................................... .

• The Federal Fund ............................................ . • Trust and Agency Fund ....................................... .

Governor's Office ............................................ . State Auditor's Office ........................................ . State Treasurer's Office ....................................... . Department of Education ..................................... . Department of Administration and Fiscal Control ................ . Adjutant General ............................................ . Public Defender ............................................. . Department of Agriculture .................................... . Revenue and Taxation ........................................ . Archives, Museums and Historical Sites ......................... . Arts Council ................................................ . Environmental Quality ........................................ . Water Development Commission ............................... . Emergency Management ...................................... . Employment Security Commission ............................. . State Engineer ............................................... . Pari Mutuel Commission ...................................... . State Examiner .............................................. . Game and Fish Commission ................................... . Fire Prevention and Electrical Safety ........................... . Geological Survey ............................................ . Wyoming Insurance Department ............................... . Manpower Planning Administration ............................ . Labor and Statistics Department ............................... . Economic Development and Stabilization Board ................. . Oil and Gas Conservation Commission ......................... .

-v-

PAGE

1 4 5 6 7 9

11 12 16 17 18 19 21 22 24 24 26 26 28 31 31 32 33 34 35 36 37 38 38 39 40 40 40 41 41 41 41 41 41 41 42 42 42 42 42 42 44

CHAPTER PAGE

III

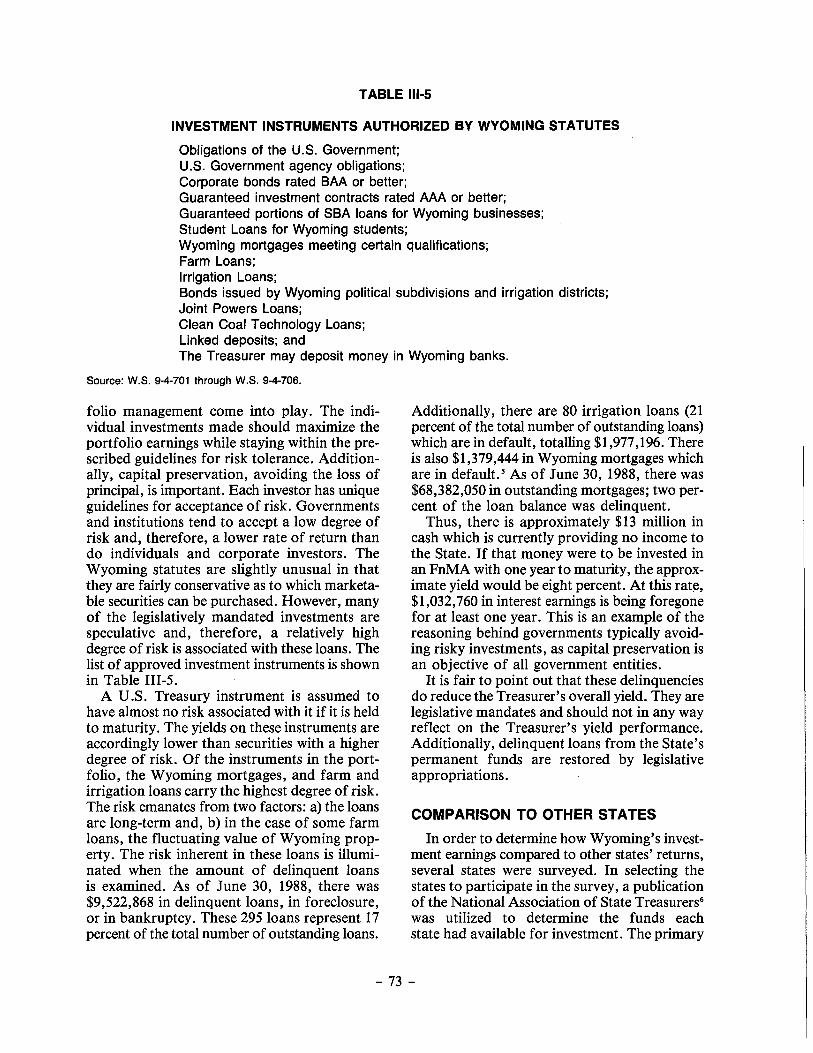

IV

Department of Public Lands . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44 State Library . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44 University of Wyoming . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45 Workers' Compensation and Wyoming Retirement System . . . . . . . . . 45 Health and Social Services . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45 Recreation Commission . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45 State Institutions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

• Debt Service Fund . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46 • Intragovernmental Fund . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46 • Highway Fund................................................ 47 • Game and Fish Fund . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48 • University of Wyoming Fund . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49 • In Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

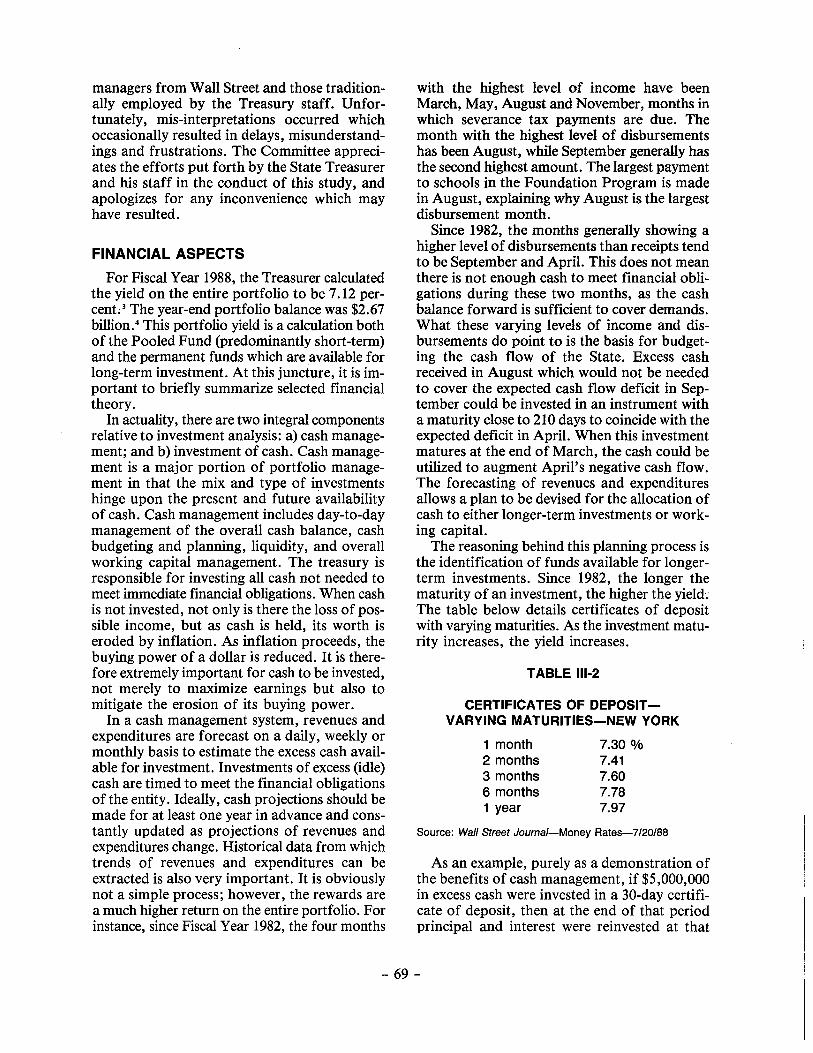

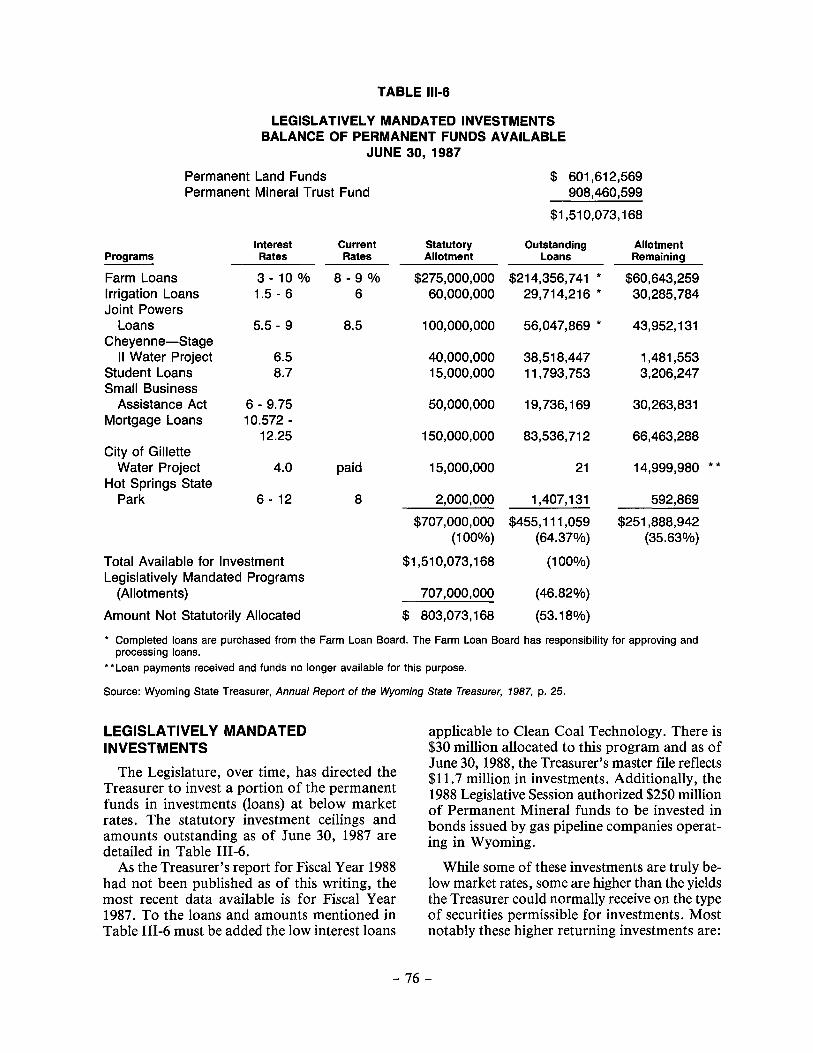

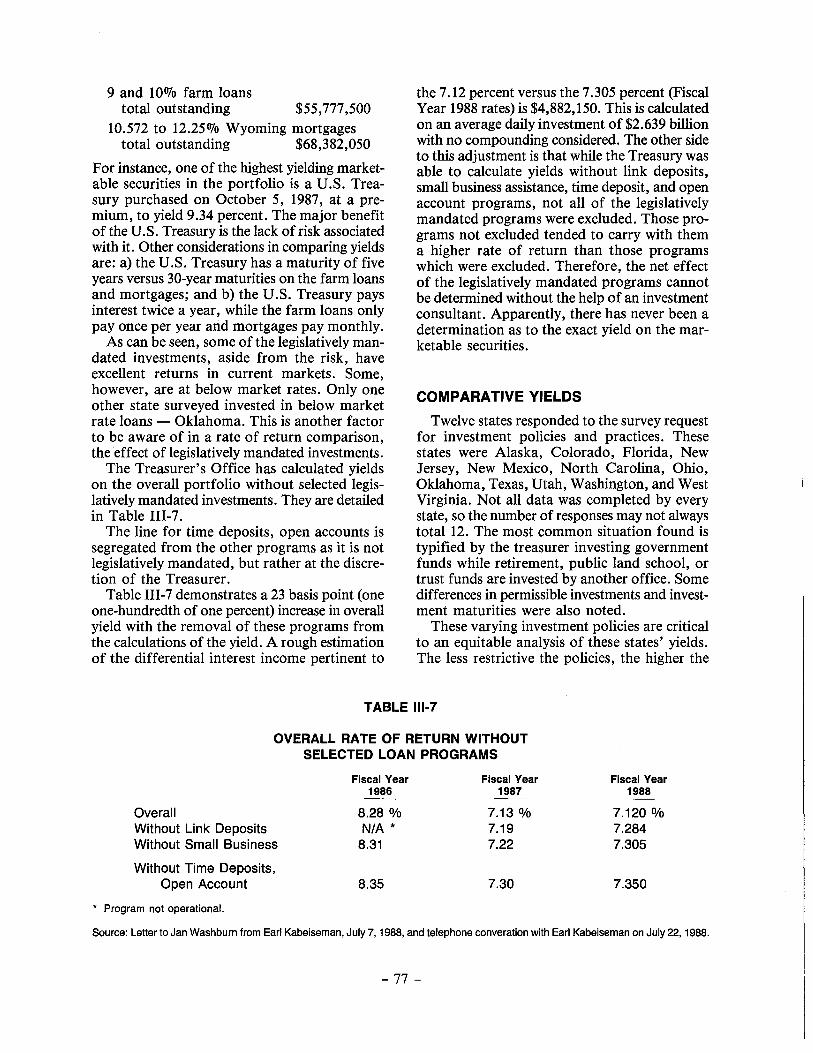

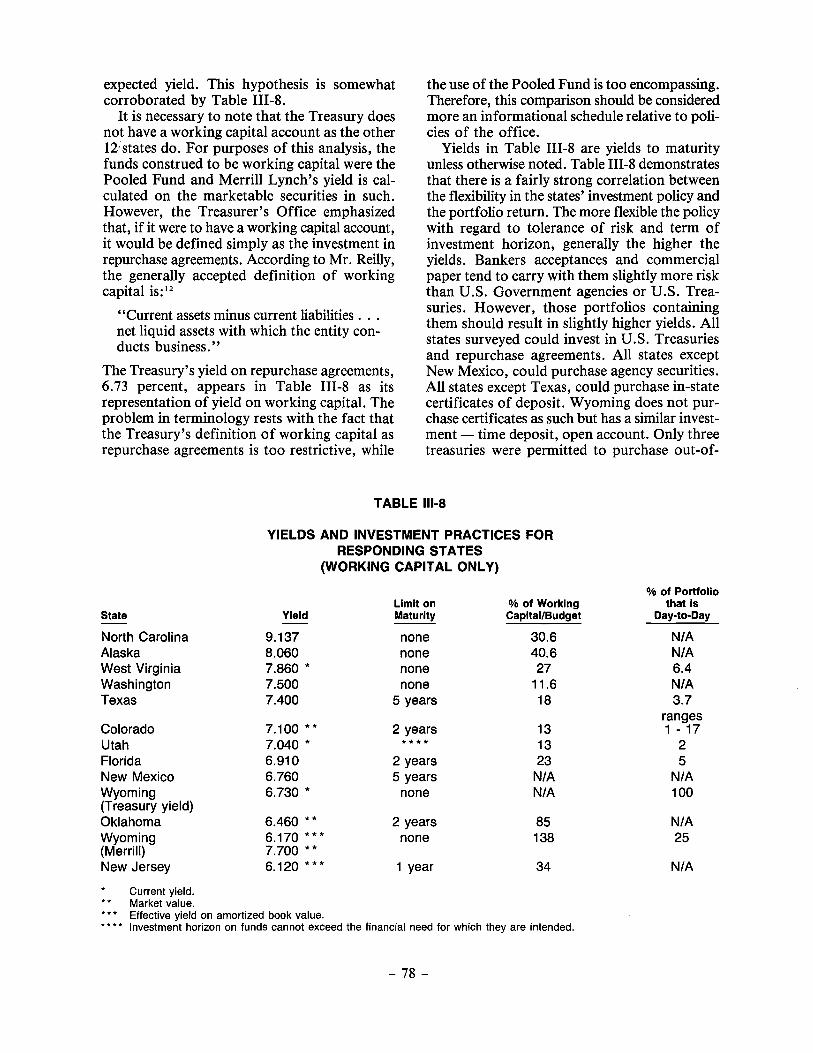

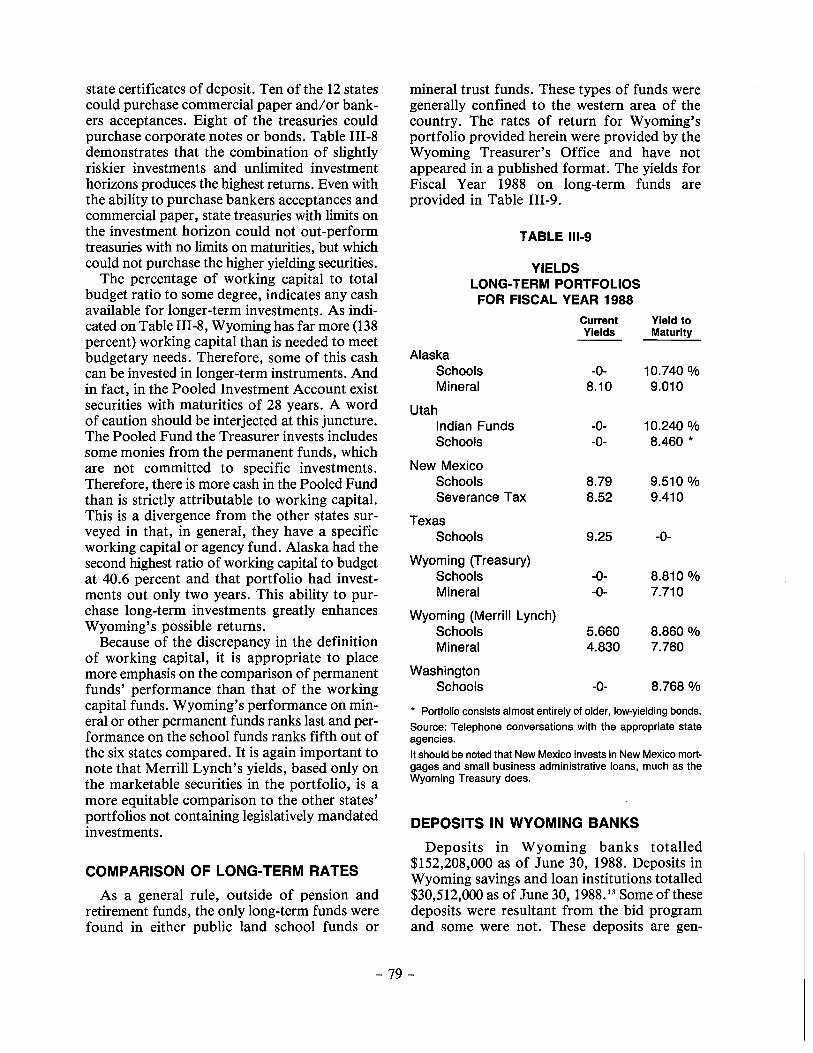

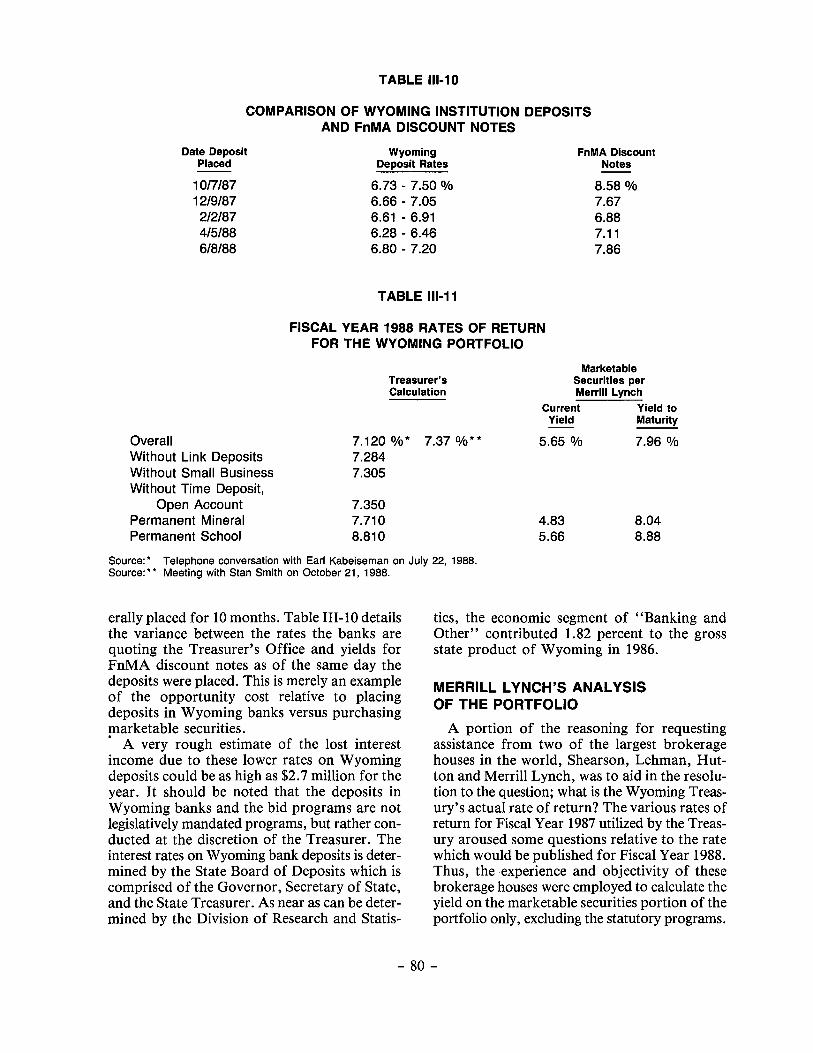

WYOMING'S INVESTMENTS AND CASH MANAGEMENT ..... . • Methodology ................................................ . • Financial Aspects ............................................ . • The Need for a Cash Management System ...................... . • Repurchase Agreements ....................................... . • Capital Preservation and Risk Tolerance ........................ . • Comparison to Other States ................................... . • Maximization and Calculation of Yields ........................ . • Investment Strategy .......................................... . • Wyoming Treasury Rate of Return ............................. . • Legislatively Mandated Investments ............................ . • Comparative Yields .......................................... . • Comparison of Long-Term Rates .............................. . • Deposits in Wyoming Banks ................................... . • Merrill Lynch's Analysis of the Portfolio ....................... . • GnMA's Held in Escrow ...................................... . • Professional Financial Management ............................ . • In Summary ................................................. . • Overall Recommendations ..................................... .

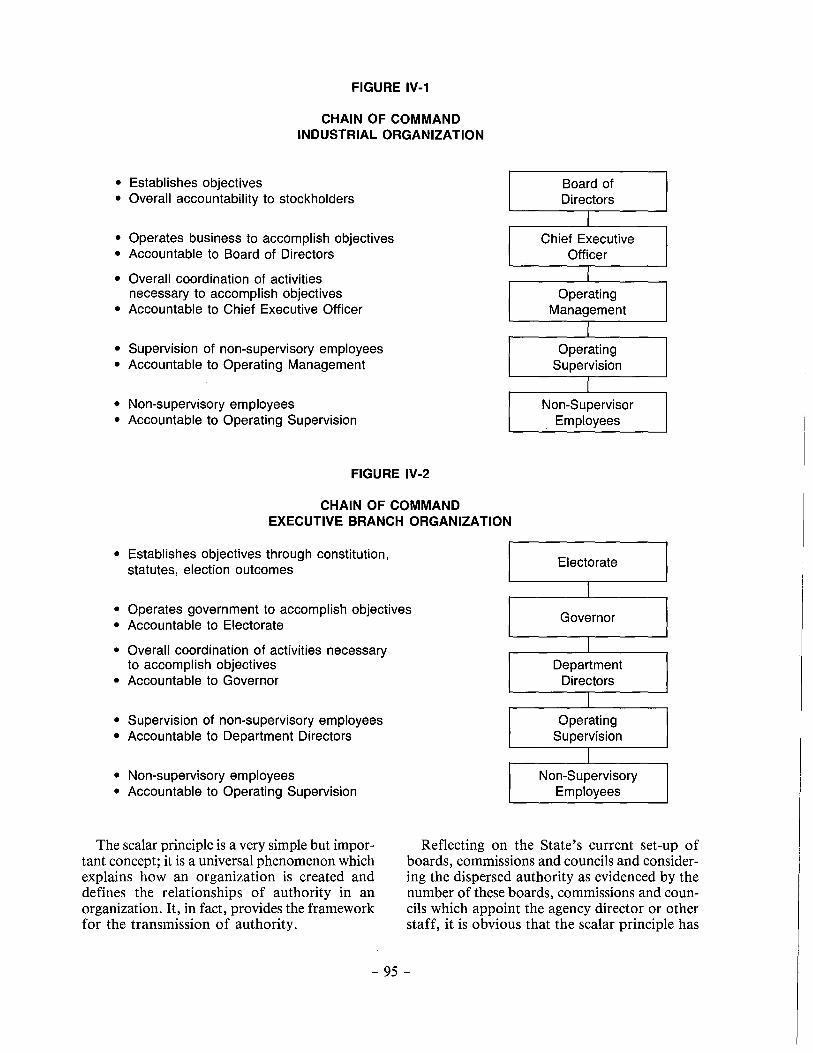

A FOUNDATION FOR RESTRUCTURING ...................... . • Why Reorganize? ............................................ . • Prevailing Typology of State Executive Branch Reorganization .... . • Key Activities ................................................ . • Wyoming Constitution ........................................ . • 49th Wyoming Legislature ..................................... . • Wyoming's Organizational Structure ............................ . • Appointment of Agency Directors .............................. . • The Principles of Organizational Structure ...................... .

The Scalar Principle .......................................... . The Principle of Unity of Command ........................... . The Principle of Span of Control .............................. . The Principle of Organizational Balance ........................ . The Principle of Organizational Simplicity ...................... . The Principle of Departmentation .............................. .

• Applying Organizational Principles to Reorganization in Wyoming ................................... .

-VI-

67 68 69 70 71 72 73 74 74 75 76 77 79 79 80 81 82 83 84

87 87 88 88 88 90 90 91 94 94 96 96 97 98 98

99

CHAPTER PAGE

v

VI

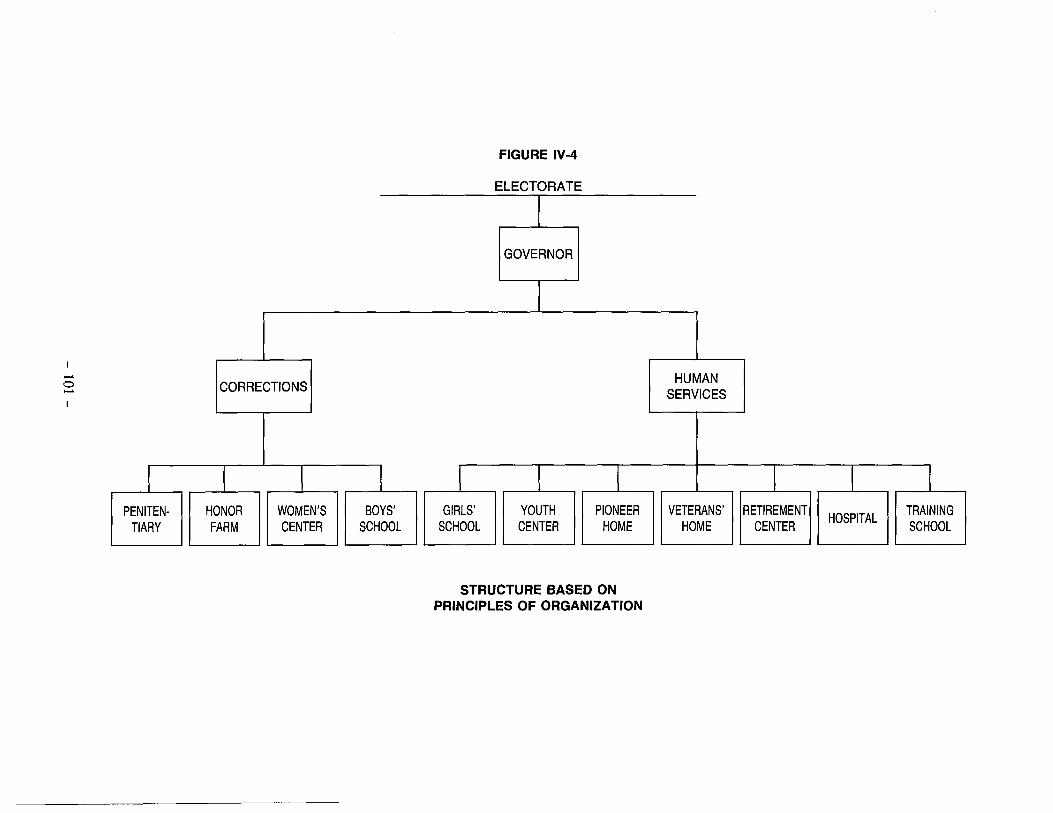

• Standards of Administrative Reorganization . . . . . . . . . . . . . . . . . . . . . . 99 • Current Structure- An Example . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 99 • Revised Structure Using Principles of Organization - An Example. . . 102 • In Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102

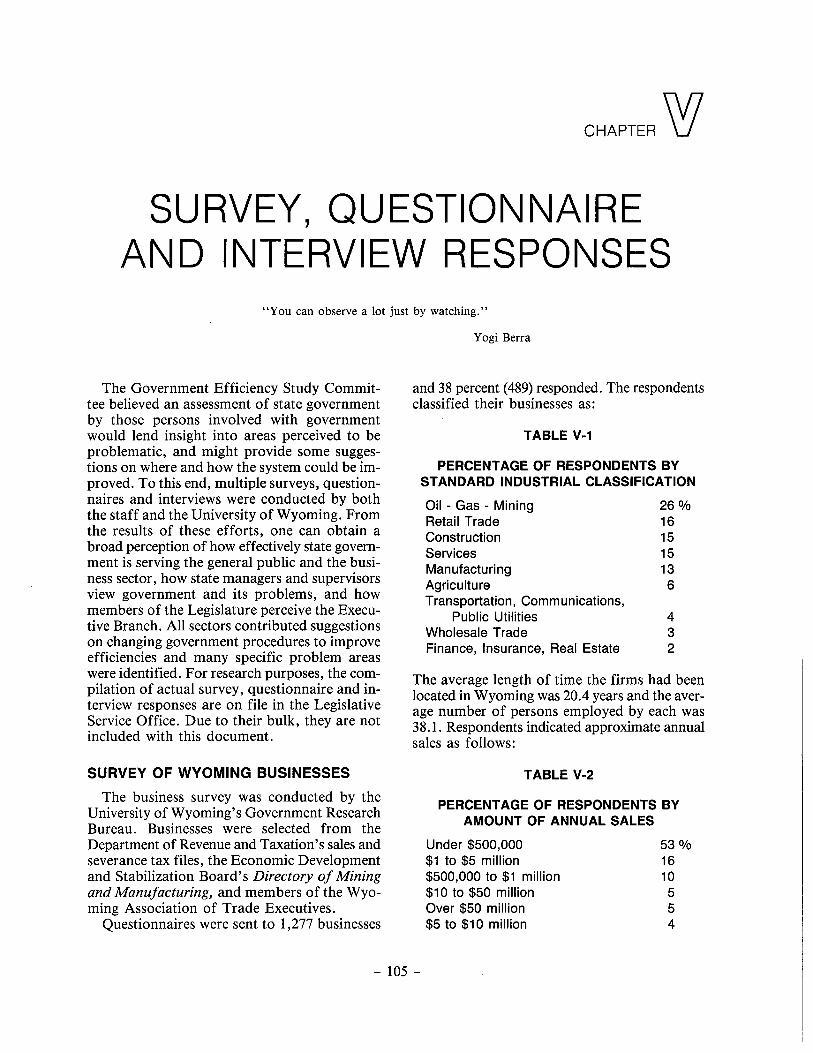

SURVEY, QUESTIONNAIRE AND INTERVIEW RESPONSES .... . • Survey of Wyoming Businesses ................................ .

General Perception of State Government ........................ . Analysis of Negative Responses ................................ . Suggestions from Businesses ................................... . Economic Development ....................................... . Tax Issues ................................................... . Privatization ................................................. .

• Survey of Wyoming Citizenry ................................. . General Perception of State Government ........................ . Analysis of Negative Responses ................................ . Problems Facing Wyoming .................................... . Tax Issues/Government Services and Spending .................. . Economic Development ....................................... . Privatization ................ ~ ................................ .

• Survey of State Agency Managers/Supervisors ................... . Problem Identification/Suggestions ............................. . Personnel Issues ............................................. . Organizational Structure ...................................... . Planning .................................................... . Fees ........................................................ . Administrative Functions ...................................... .

• Interviews with Legislators .................................... . Boards, Commissions and Councils ............................ . Structure of the Executive Branch .............................. . Current System of Elected Officials ............................ . Responsibilities of Elected Officials ............................ . Appointment Authority ....................................... . Budget Process .............................................. . Personnel Issues ............................................. . Privatization ................................................. . Audit ............................................. ··········· Education ................................................... . Role of the Legislature ....................................... .

• In Summary ................................................. .

CONCEPTUAL REORGANIZATION STRUCTURE FOR WYOMING • Process of Reorganization ..................................... . • Suggested Statutory Language ................................. .

Purpose ..................................................... . Definitions .................................................. . Reorganization Concept ....................................... . Structure of the Executive Branch .............................. . Directors of Departments - Powers and Duties ................... . Appointment and Removal Power .............................. . Method of Reorganization .................................... .

Type One Transfer ......................................... .

-vii-

105 105 106 107 108 110 111 112 112 112 113 113 114 115 115 115 116 117 119 120 120 121 122 122 122 123 123 123 123 124 124 124 124 124 125

129 129 130 130 131 131 132 132 133 133 134

CHAPTER PAGE

VII

Type Two Transfer . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 134 Type Three Transfer. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 134

Rights and Obligations of Succeeding Department. . . . . . . . . . . . . . . . . 134 Federal Aid, Bond Obligations; Not Impaired . . . . . . . . . . . . . . . . . . . . 134 Amendment of Conflicting Laws . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 134

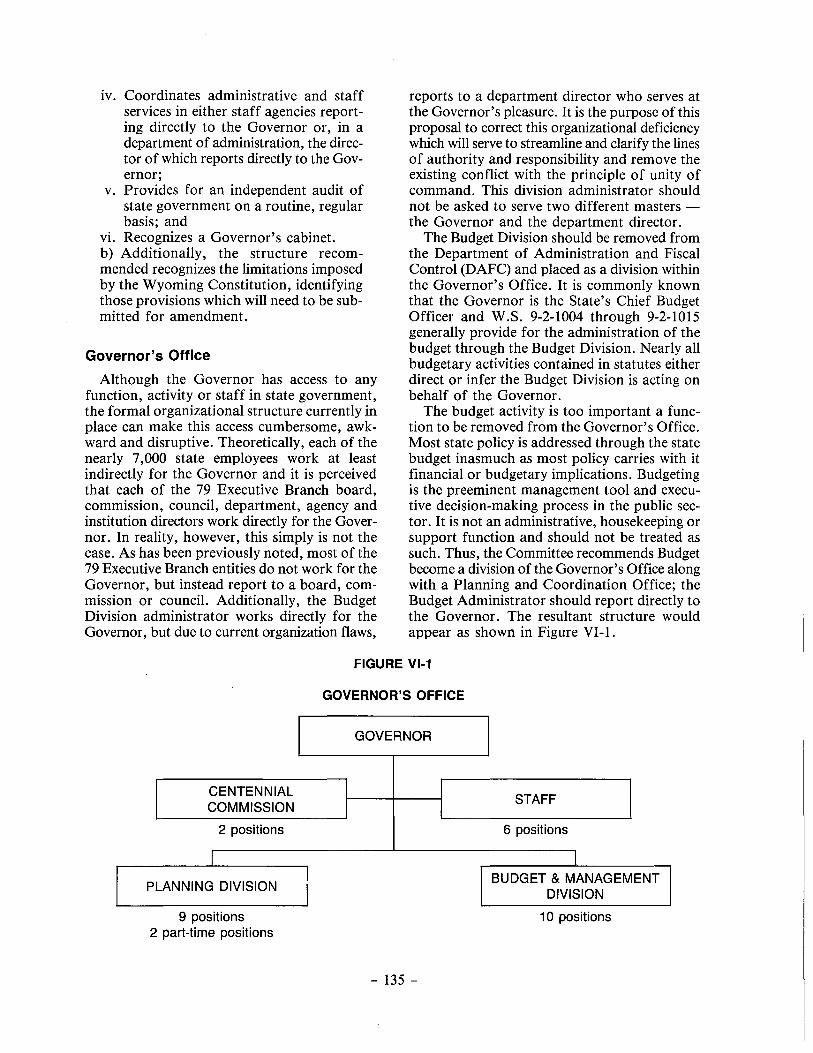

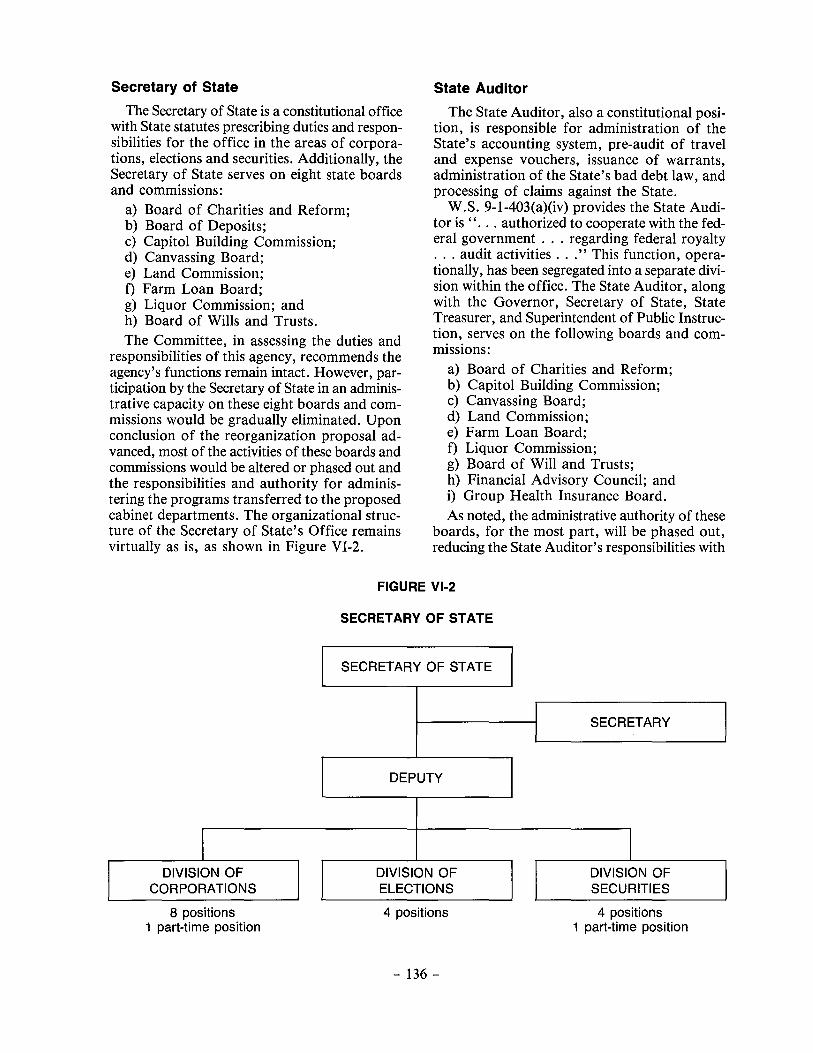

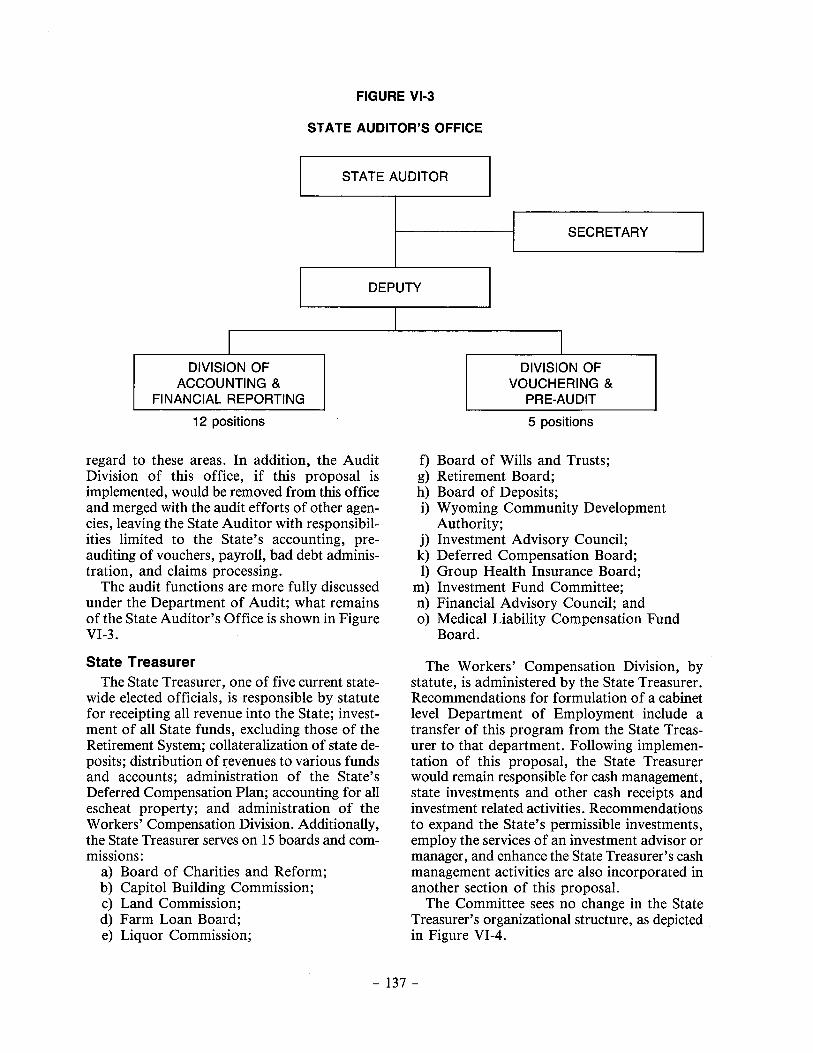

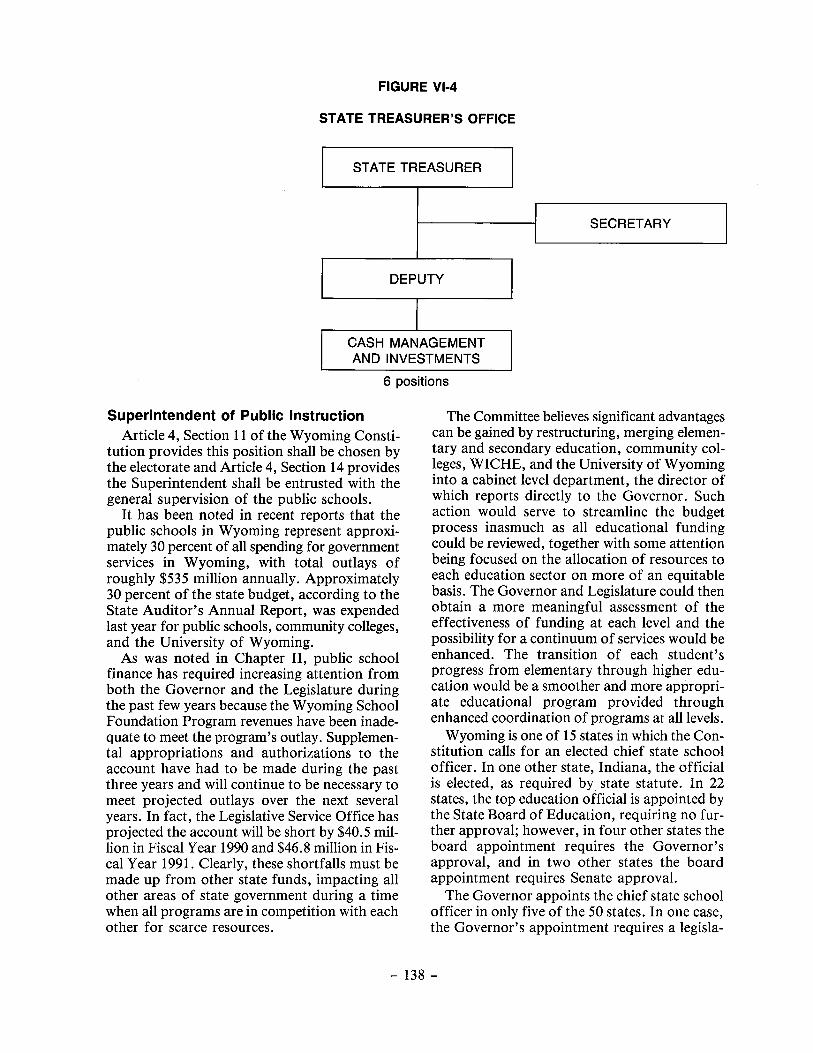

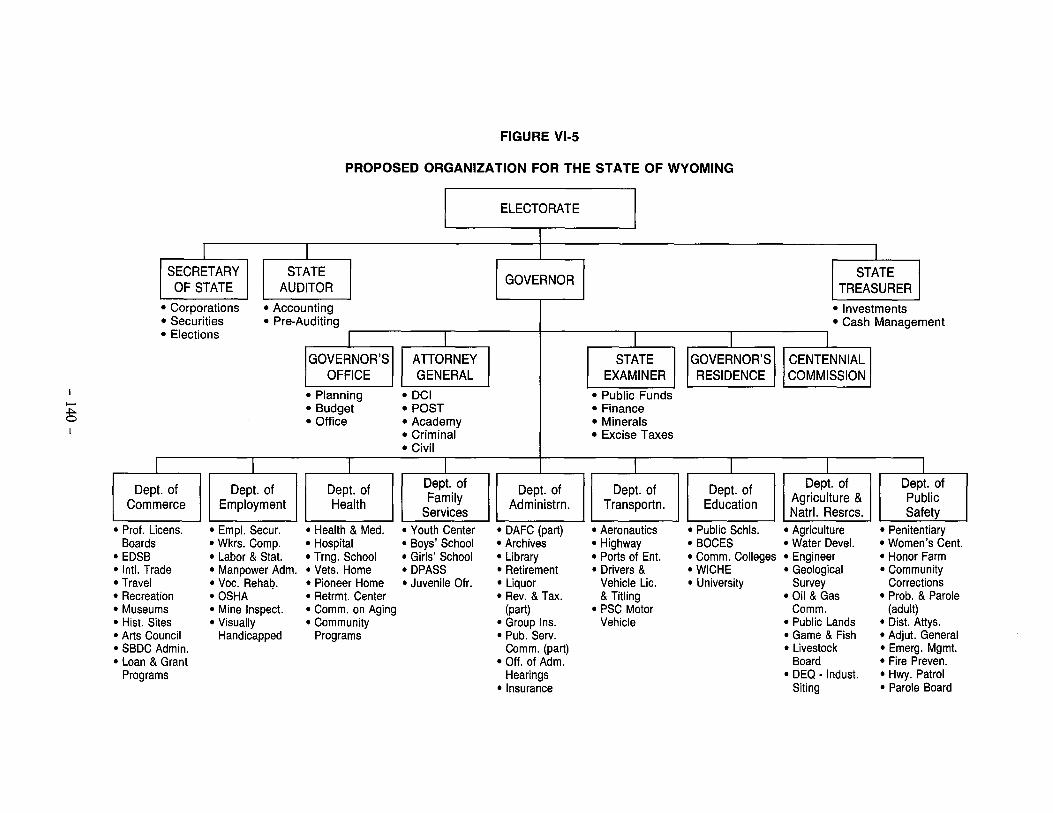

• Overall Structure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 134 Governor's Office.................................. . . . . . . . . . . . 135 Secretary of State . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 136 State Auditor..... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 136 State Treasurer . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 137 Superintendent of Public Instruction . . . . . . . . . . . . . . . . . . . . . . . . . . . . 138

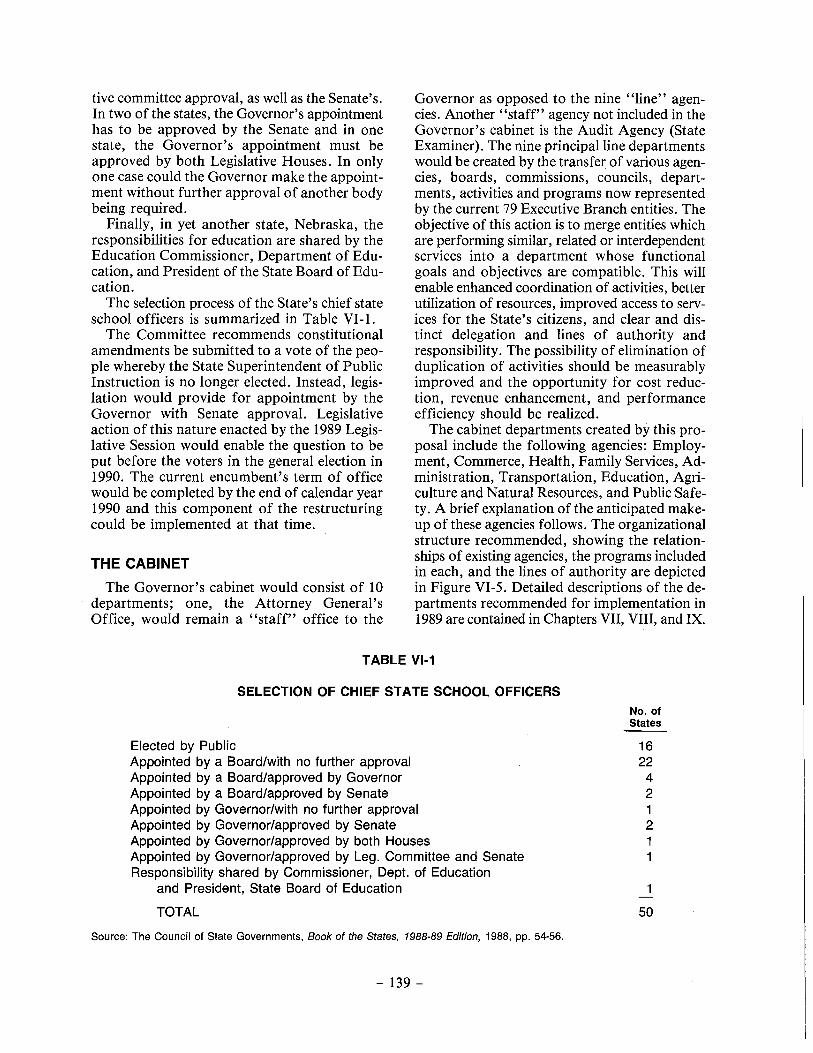

• The Cabinet . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 139 Department of Employment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 141 Department of Commerce...................................... 141 Department of Health . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 141 Department of Family Services . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 141 Department of Administration.............................. . . . . 141 Department of Transportation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 141 Department of Education . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 141 Department of Agriculture and Natural Resources . . . . . . . . . . . . . . . . 142 Department of Public Safety . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 142

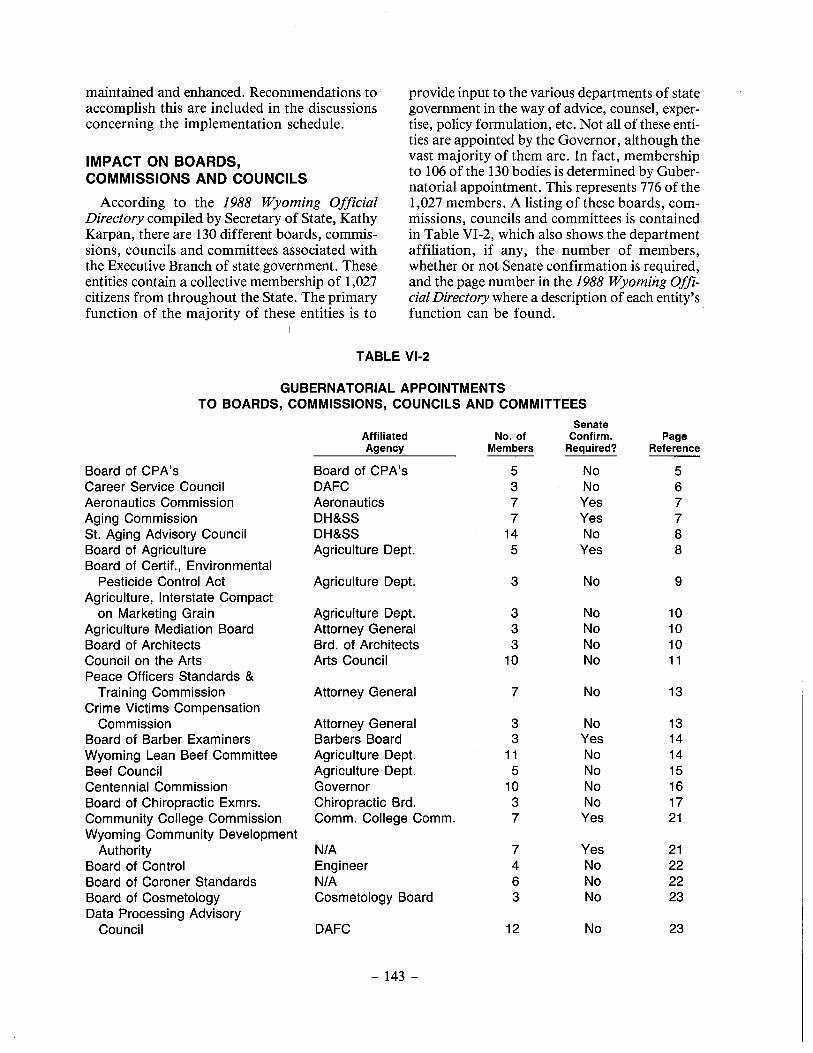

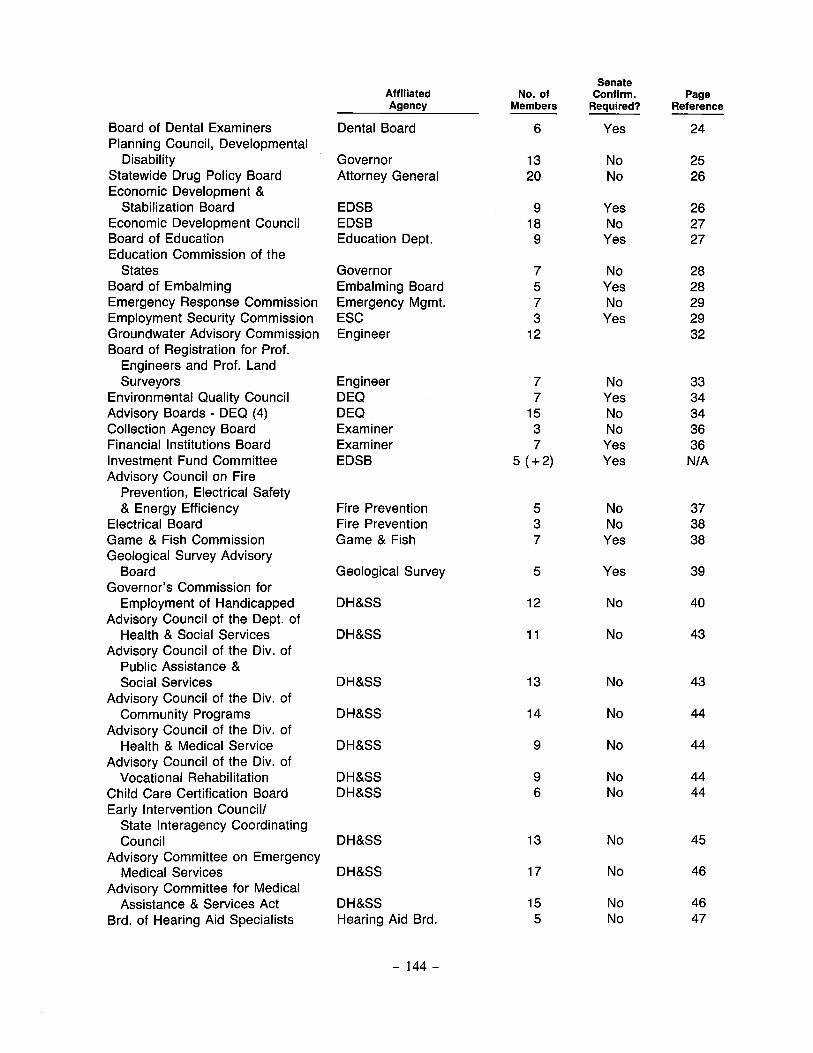

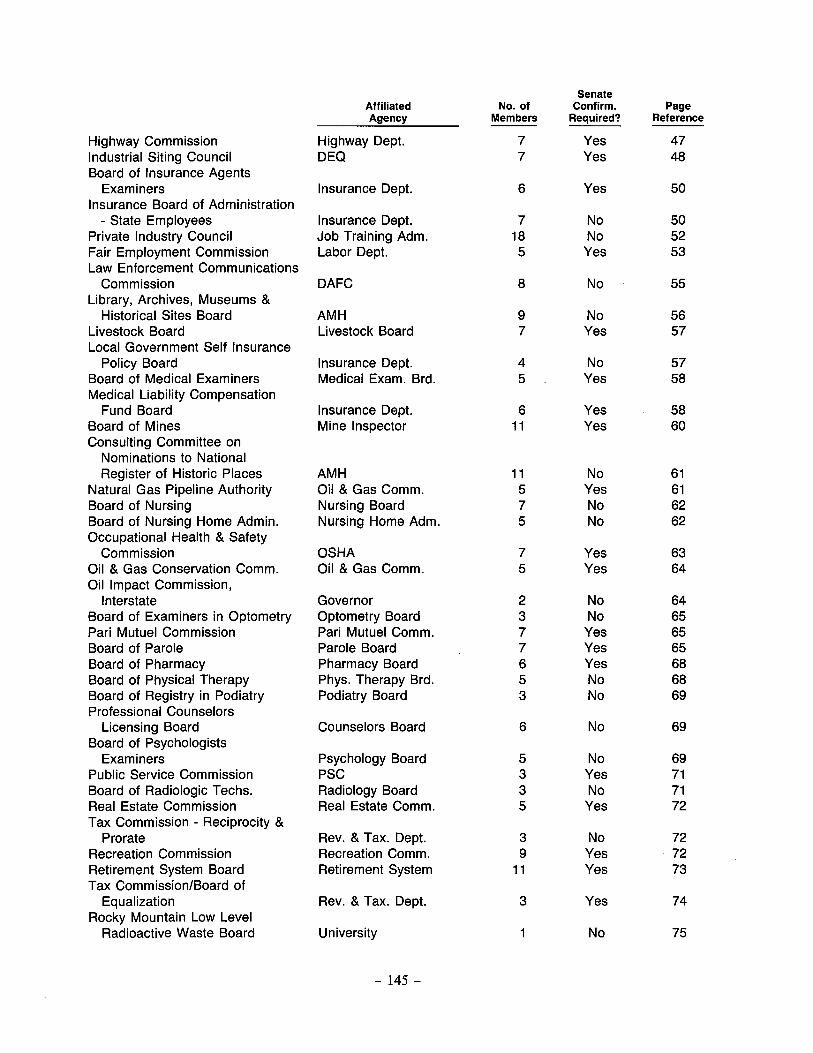

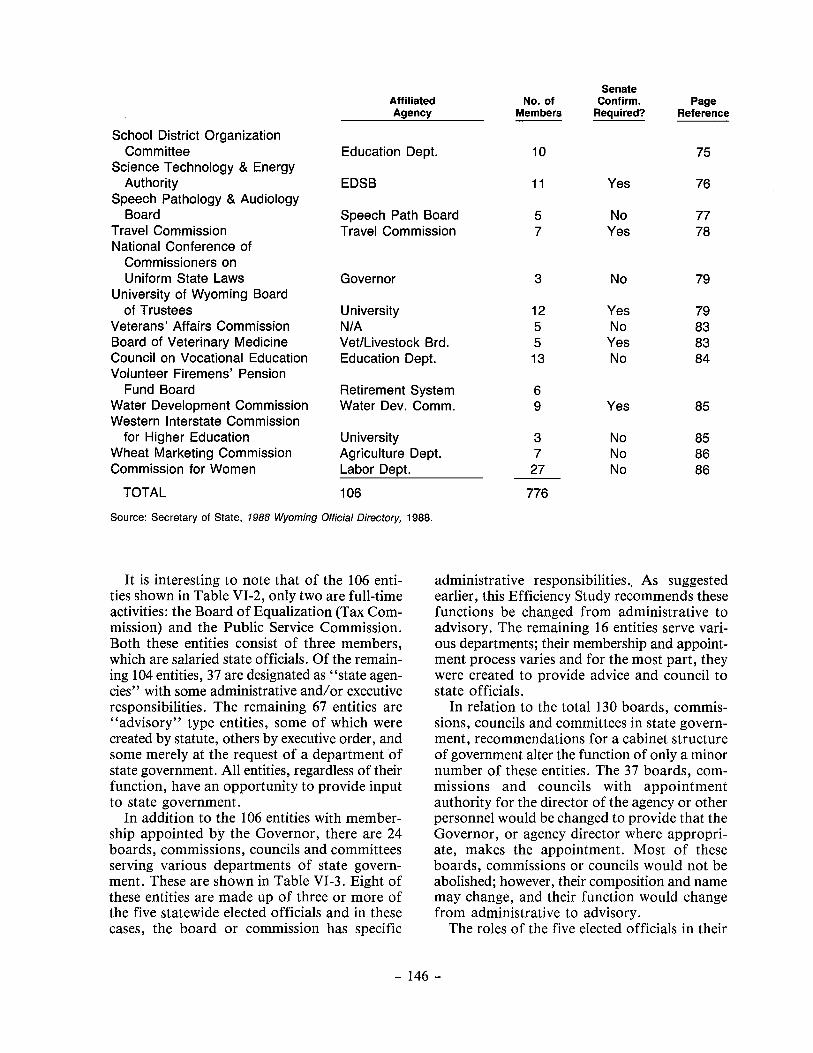

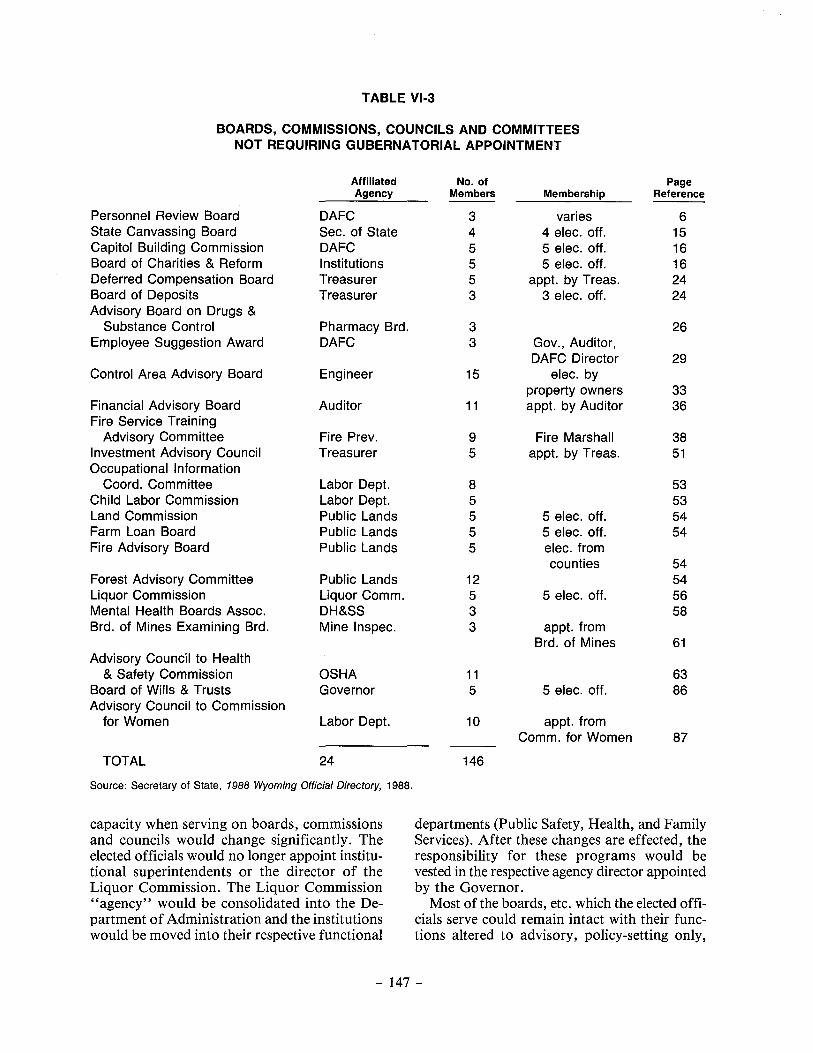

• Impact on Statewide Elected Officials . . . . . . . . . . . . . . . . . . . . . . . . . . . 142 • Impact on Boards, Commissions and Councils.................... 143 • Impact on the State's Personnel System...... . . . . . . . . . . . . . . . . . . . . 148

Creation of a Separate Classification and Compensation Plan for Exempt Positions . . . . . . . . . . . . . . . . . . . . . . . . 148 Reclassification of Existing Positions . . . . . . . . . . . . . . . . . . . . . . . . . . . . 149 Staff Development Programs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 150

• Impact on the State's Budgeting System . . . . . . . . . . . . . . . . . . . . . . . . . 151 • The Implementation Schedule. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 152

The State Government Reorganization Act of 1989.............. . . 152 Constitutional Amendments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 152 Departments to be Implemented in 1989 . . . . . . . . . . . . . . . . . . . . . . . . . 153 Governor's Office/DAFC . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 153 State Auditor's Office . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 153 Department of Revenue and Taxation . . . . . . . . . . . . . . . . . . . . . . . . . . . 153 Departments to be Implemented in 1990 and 1991....... . . . . . . . . . . 153

• In Summary.................................................. 153

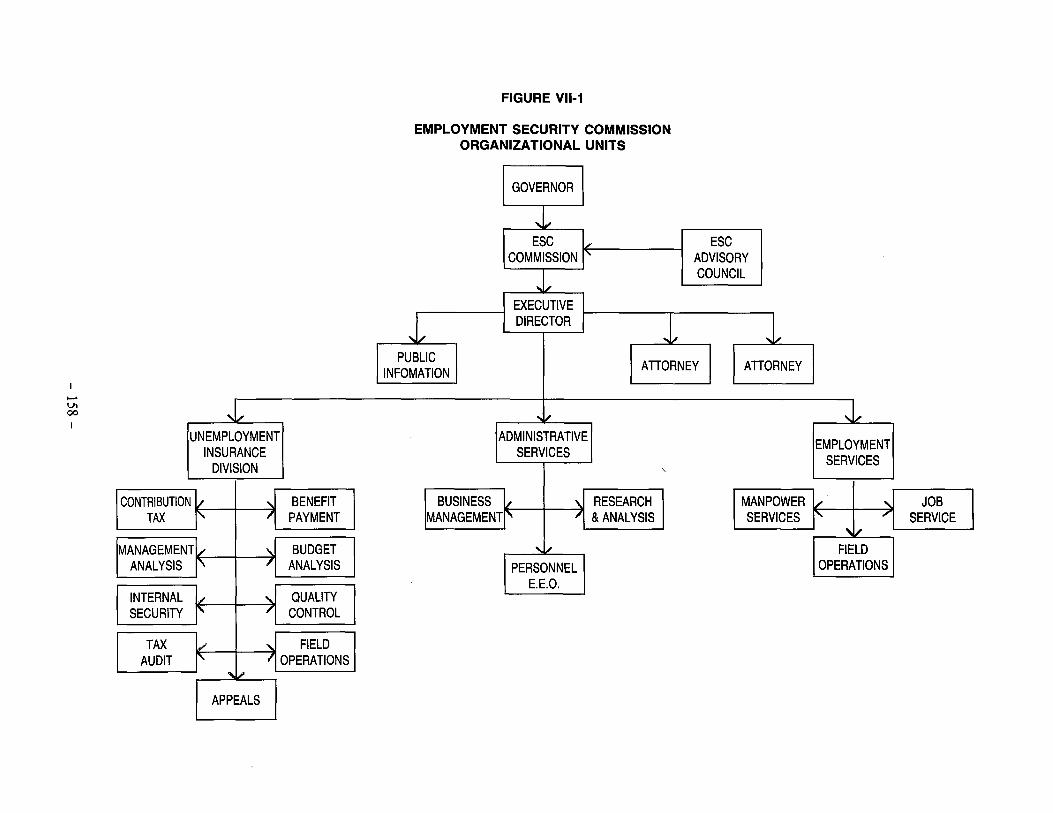

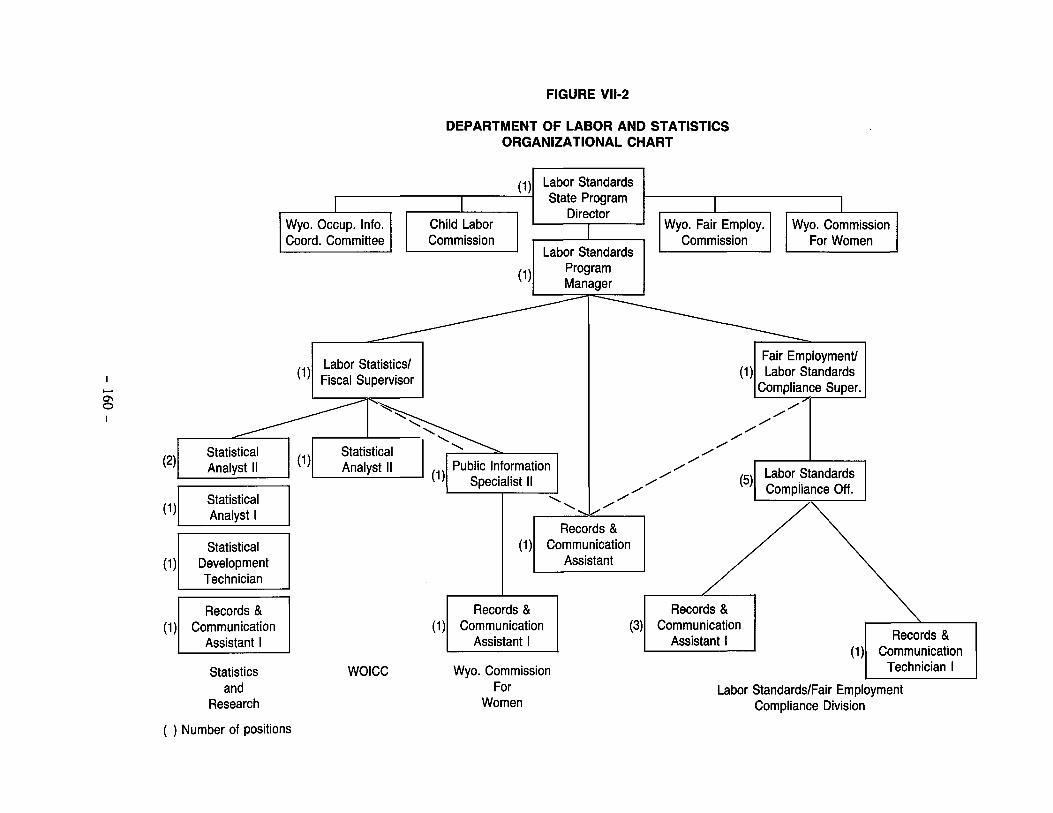

THE DEPARTMENT OF EMPLOYMENT ....................... . • Employment Security Commission ............................. . • Department of Labor and Statistics ............................ .

Wyoming Fair Employment Commission ........................ . Wyoming Commission for Women ............................. .

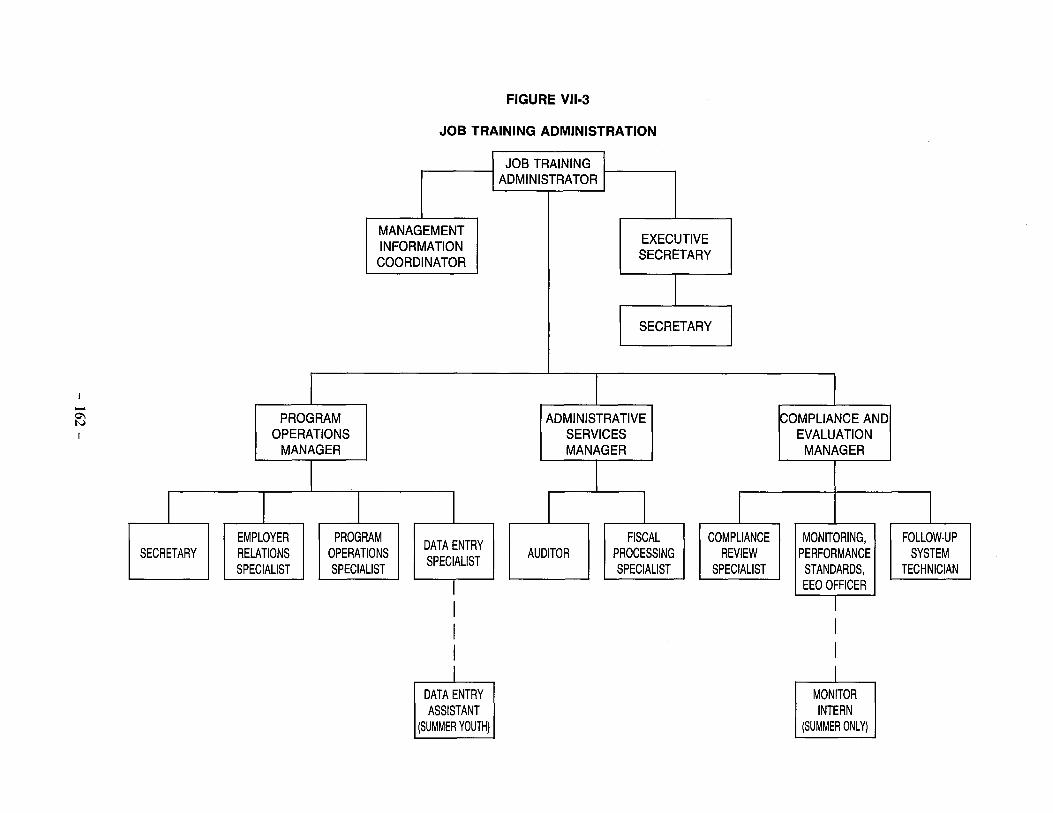

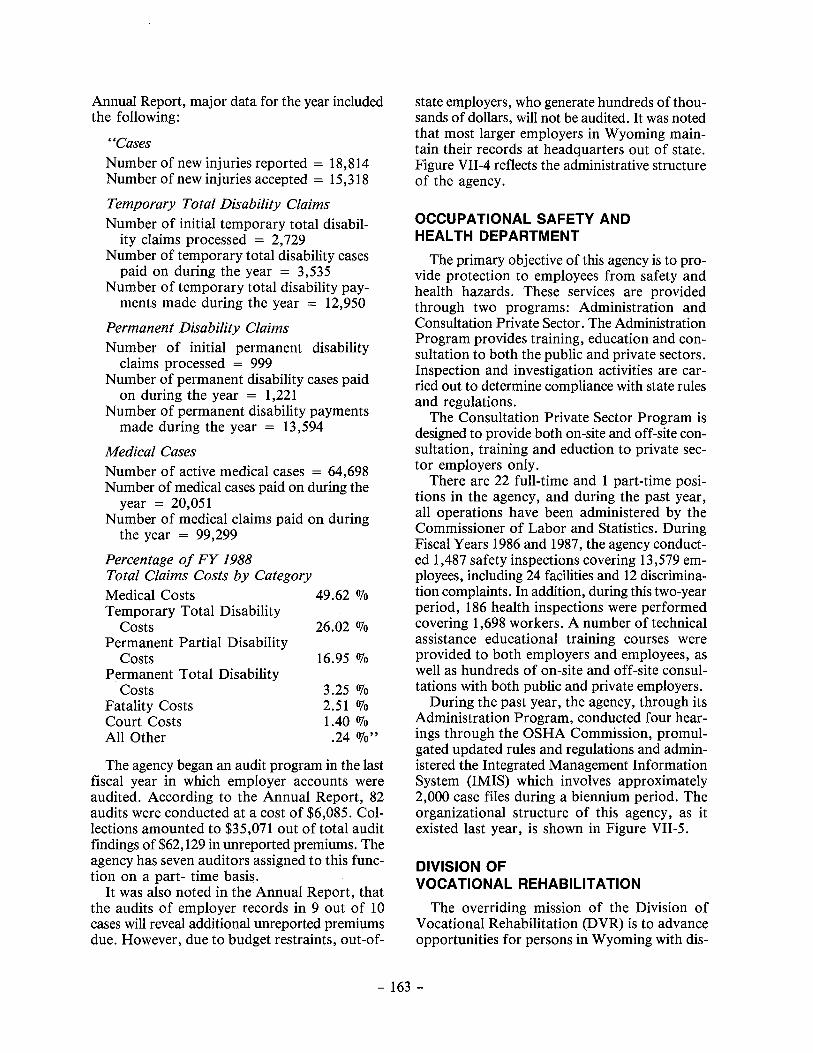

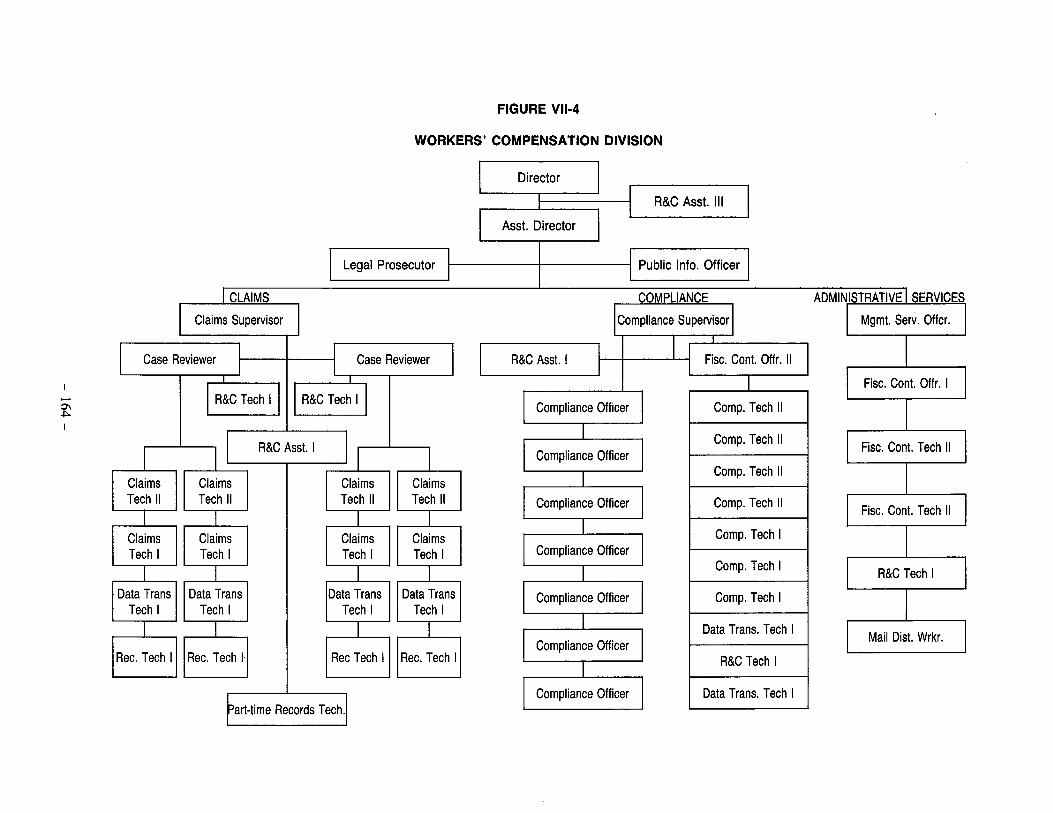

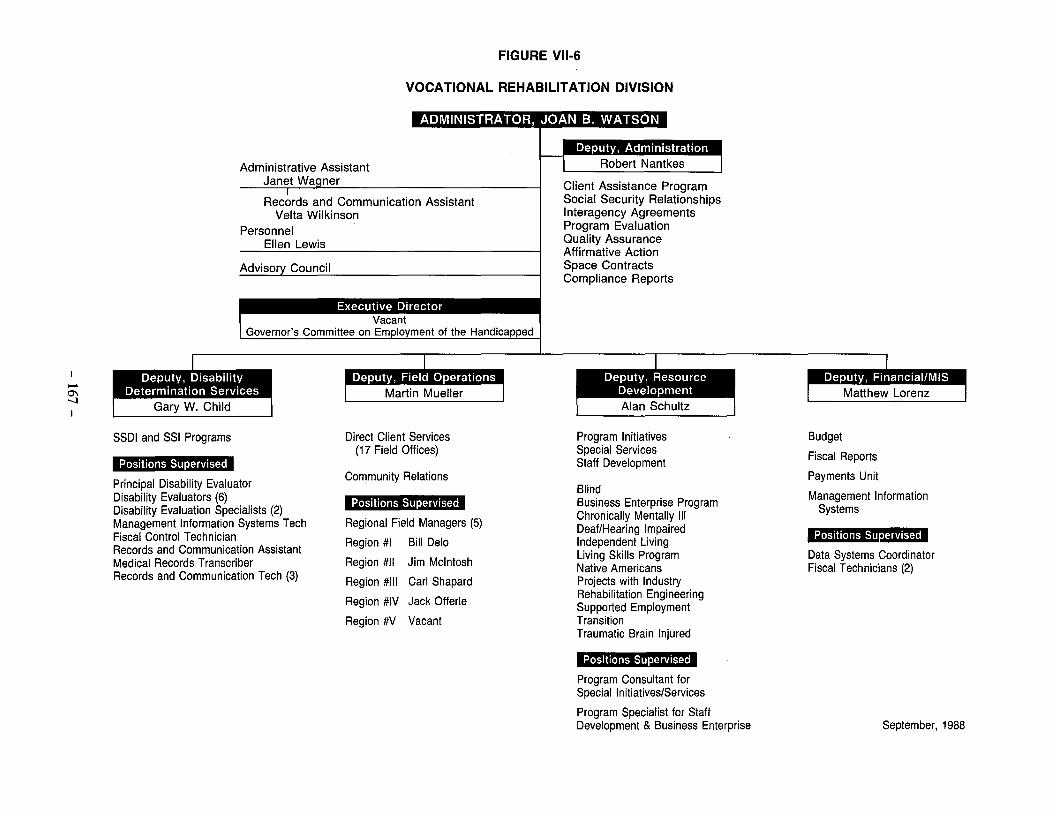

• Job Training Administration .................................. . • Division of Workers' Compensation ............................ . • Occupational Safety and Health Department .................... . • Division of Vocational Rehabilitation ........................... .

General Rehabilitation ........................................ . Independent Living ........................................... . Business Enterprises .......................................... . In-Service Training ........................................... .

- Vlll -

157 157 159 159 159 159 161 163 163 166 166 166 166

CHAPTER PAGE

VIII

IX

X

Living Skills . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 166 Social Security Disability Determination Services . . . . . . . . . . . . . . . . . . 168 Governor's Committee on Employment for the Handicapped....... 168 Supported Employment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 168

• Department of Education Visually Handicapped Services . . . . . . . . . . 168 • State Inspector of Mines . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 168 • The Need for Consolidation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 168

Labor Law Compliance........................................ 168 Payments to Individuals . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 169 Job Training . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 169 Labor Market Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 169

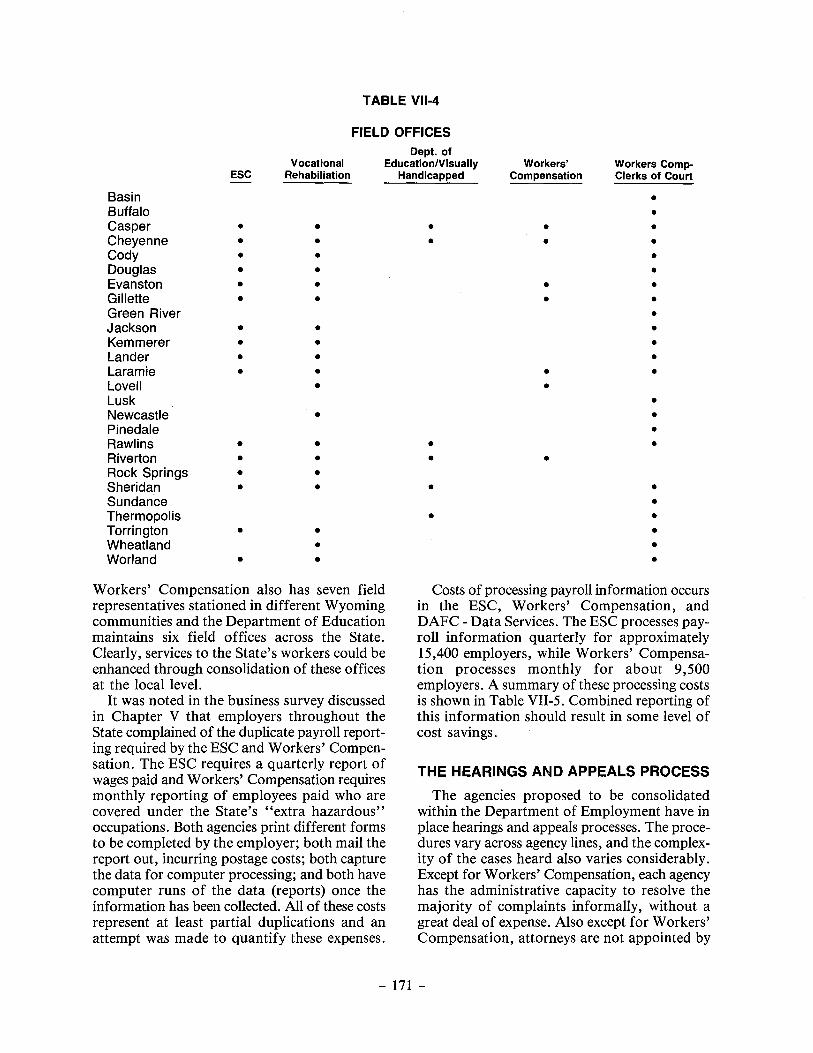

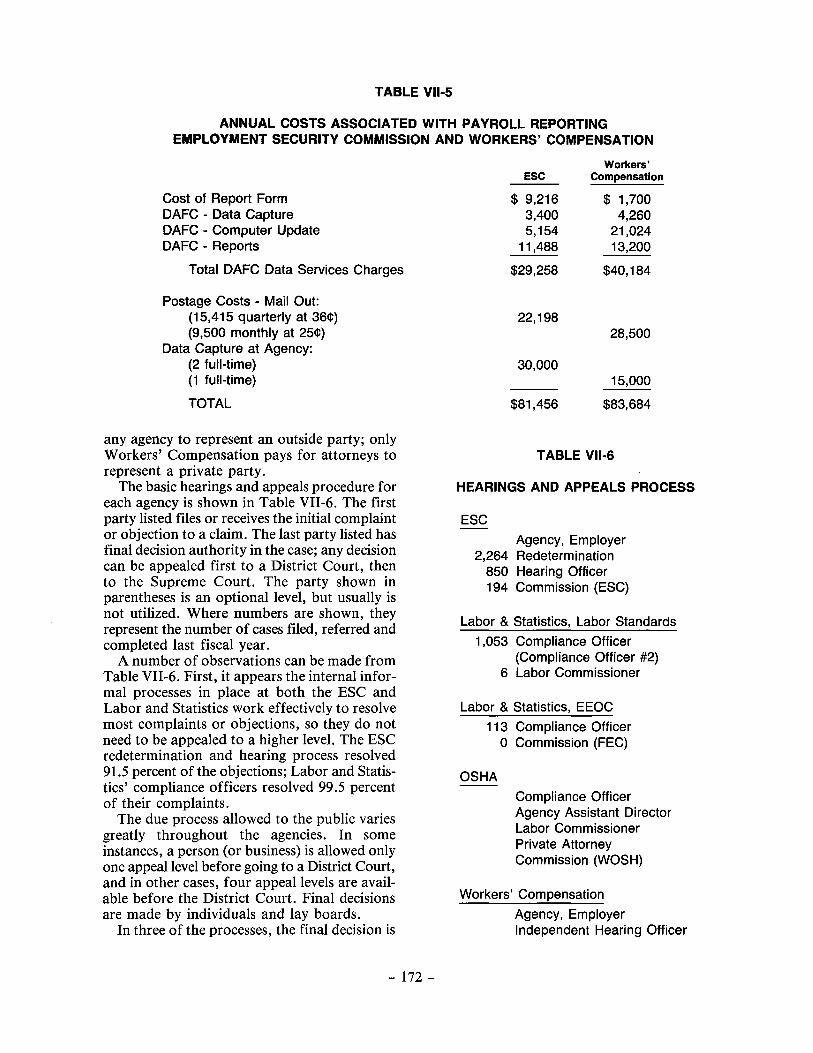

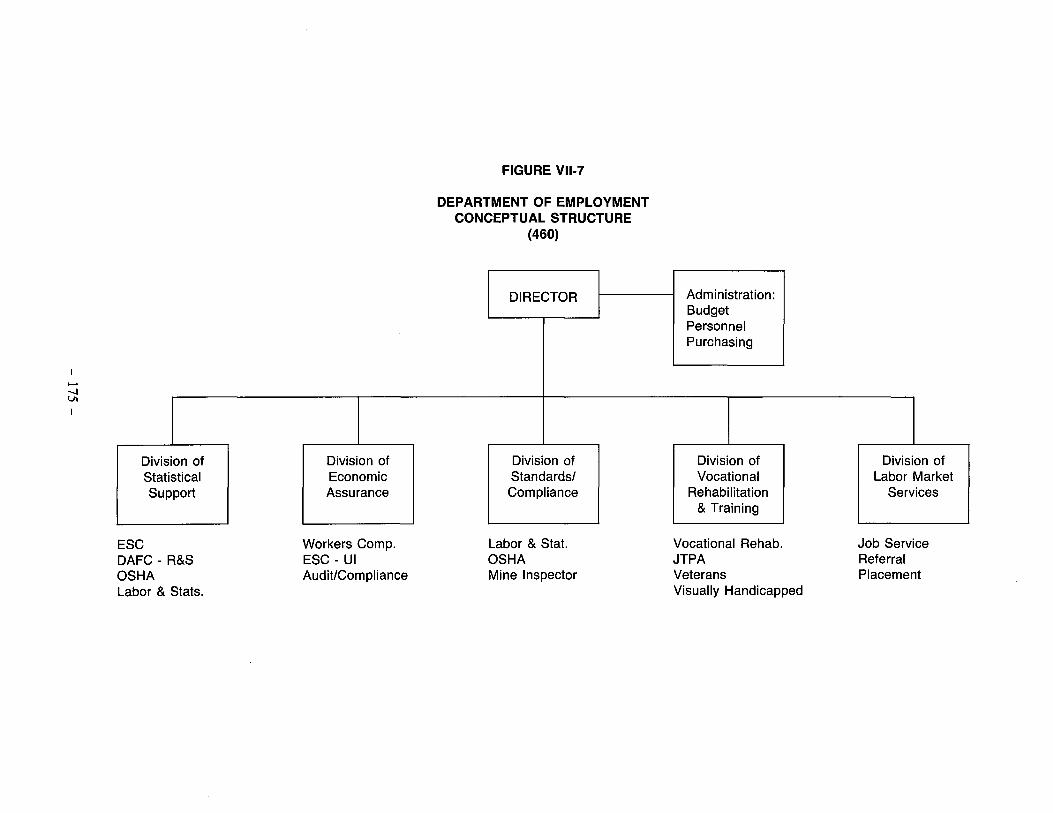

• The Hearings and Appeals Process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 171 • Boards, Commissions and Councils . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 174 • The Department's Proposed Organizational Structure . . . . . . . . . . . . . . 17 6 • In Summary.................................................. 176

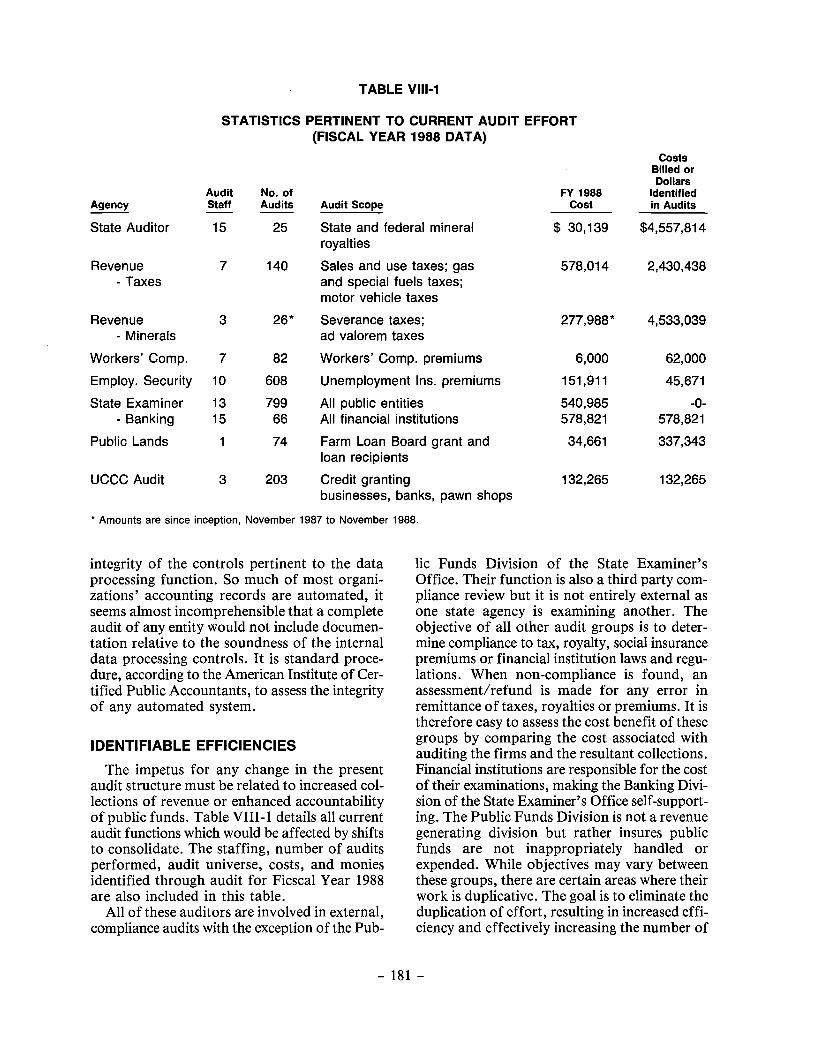

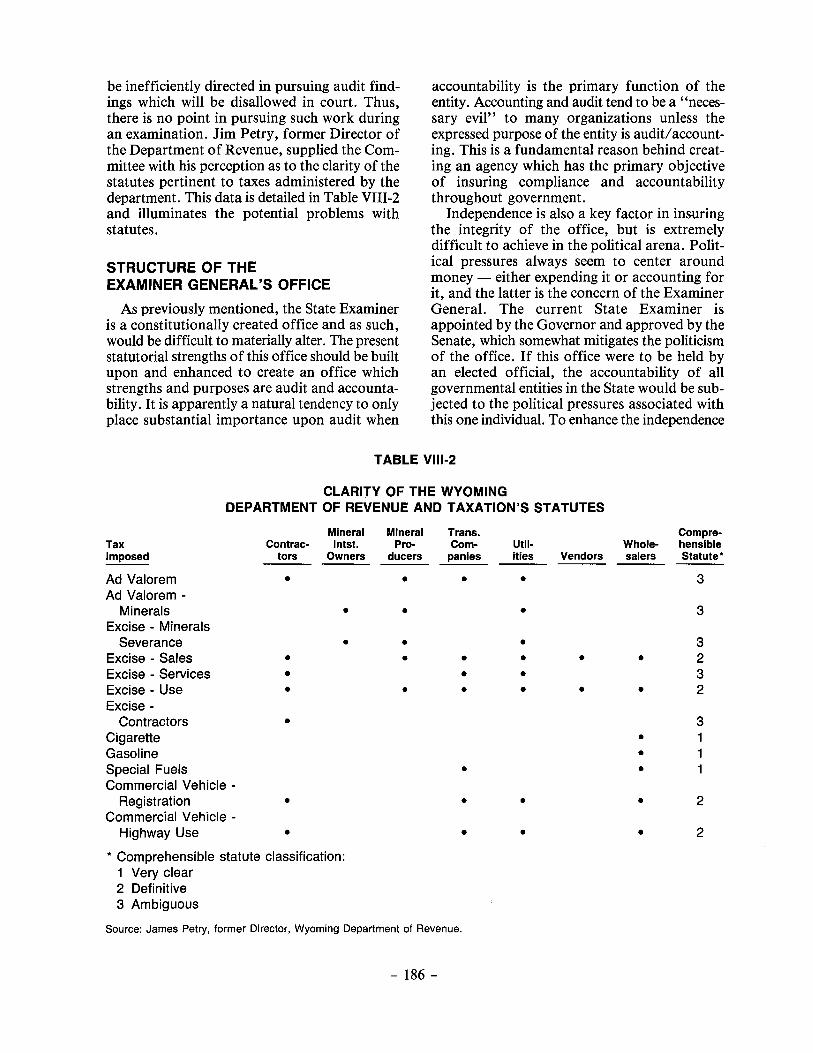

THE DEPARTMENT OF AUDIT ............................... . • Federal/State Requirements ................................... . • Current Audit Efforts ........................................ . • The Need for a Concentrated Audit ........................... . • The Need for Independence ................................... . • Proposed Examiner General's Office ........................... . • Identifiable Efficiencies ....................................... . • Workers' Compensation and Employment Security Commission ... . • Mineral Audits .............................................. . • Quantifying Efficiencies ....................................... . • Severance and Ad Valorem Statutes and Policies ................. . • Structure of the Examiner General's Office ...................... .

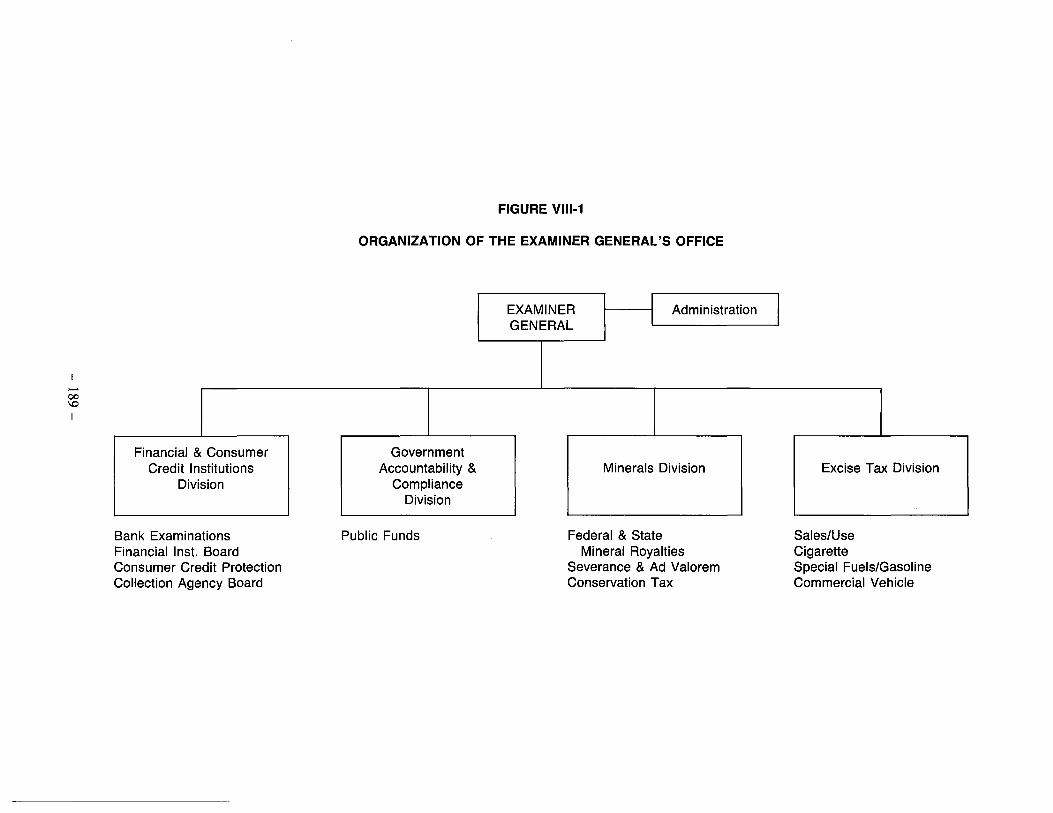

Financial and Consumer Credit Institutions Division ............. . Minerals Division ............................................ . Governmental Accountability and Compliance Division ........... . Excise Tax Division .......................................... .

• Performance Auditing ........................................ . • In Summary ................................................. .

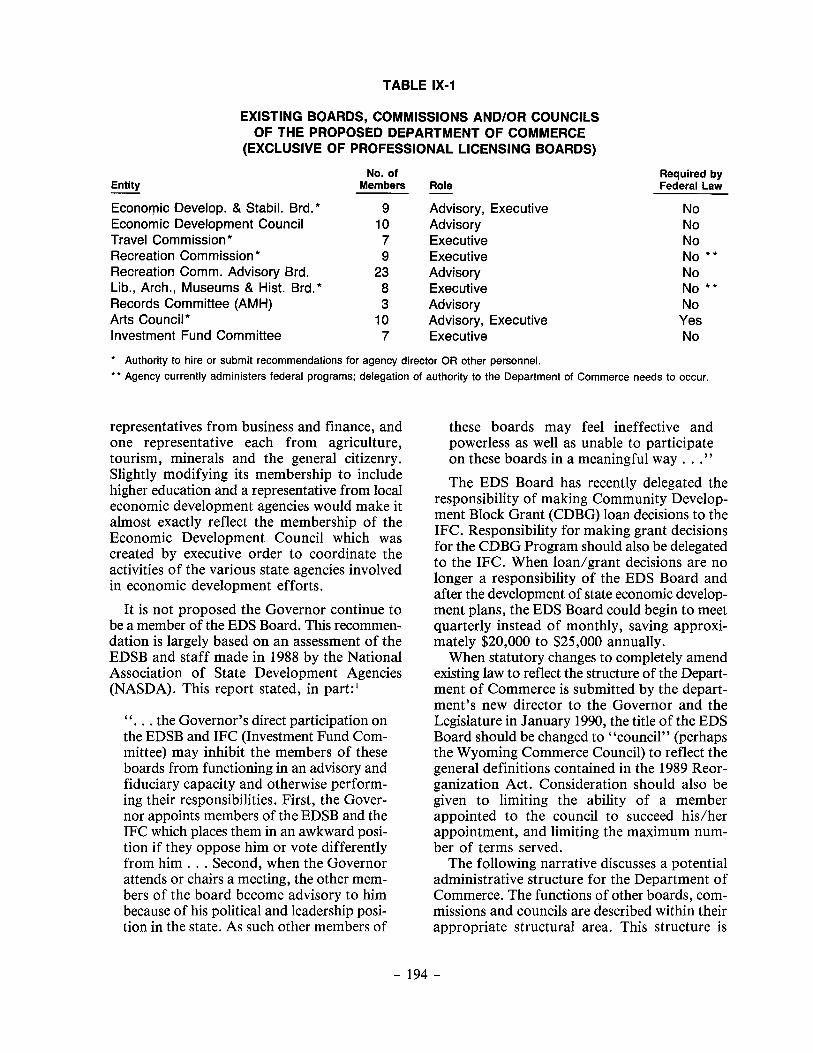

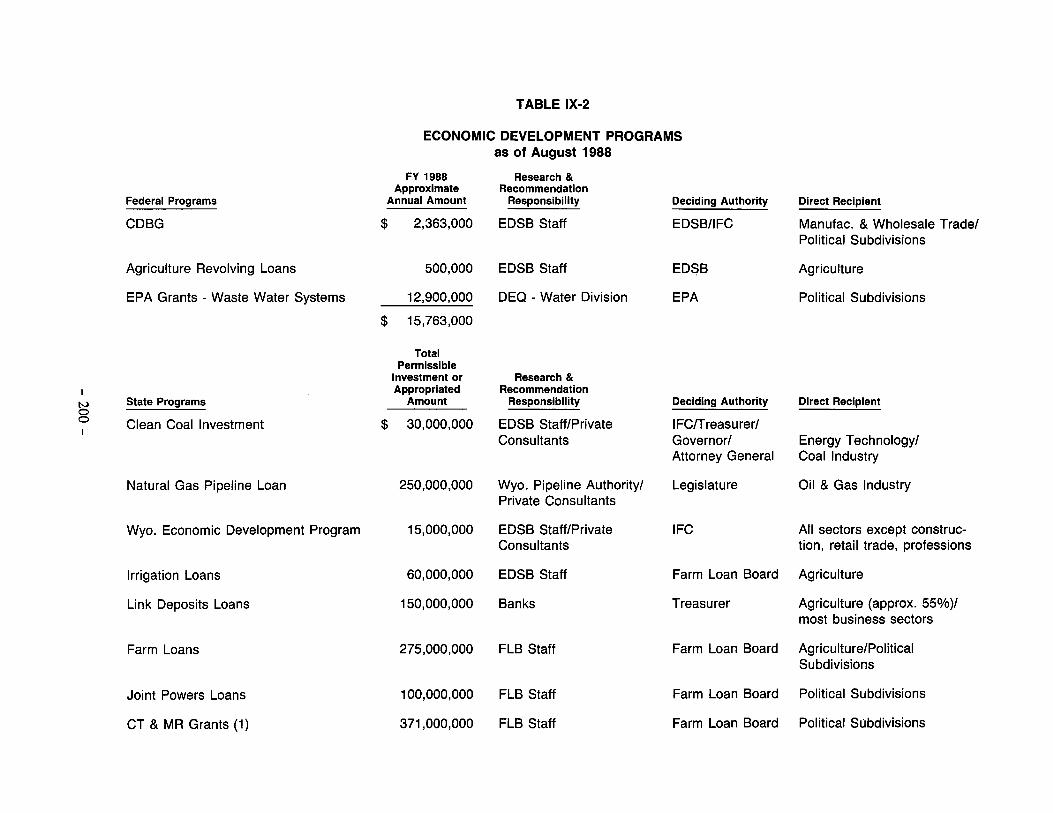

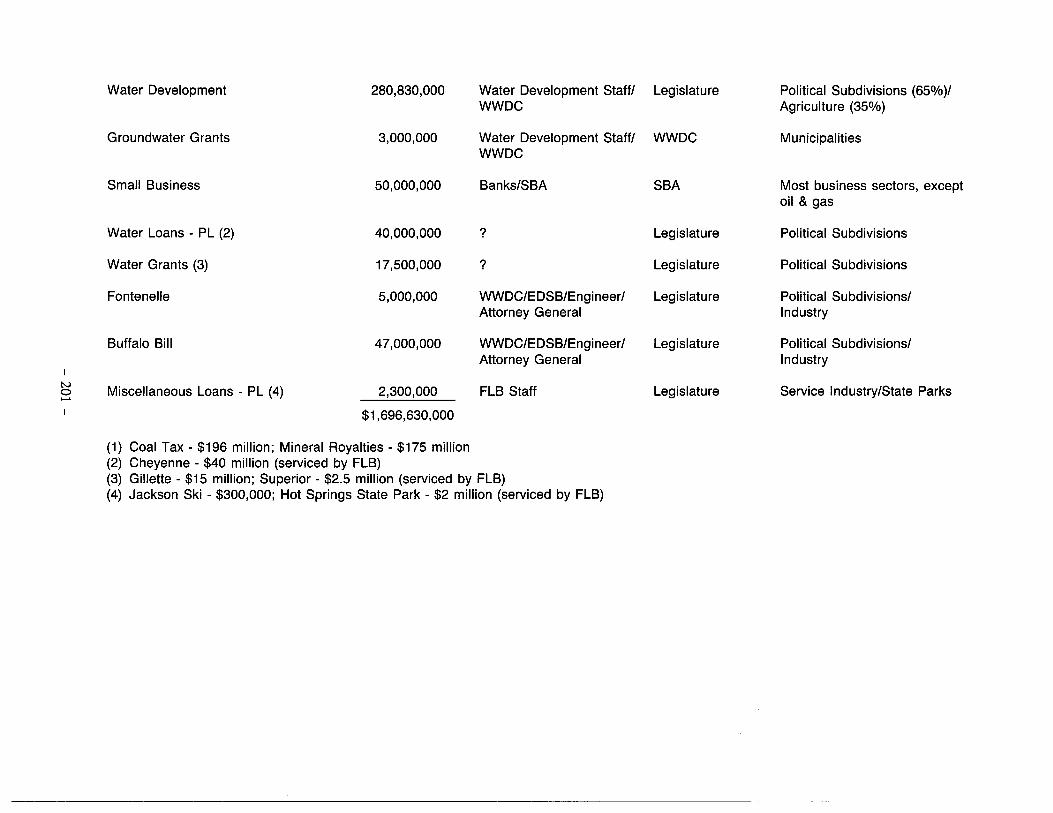

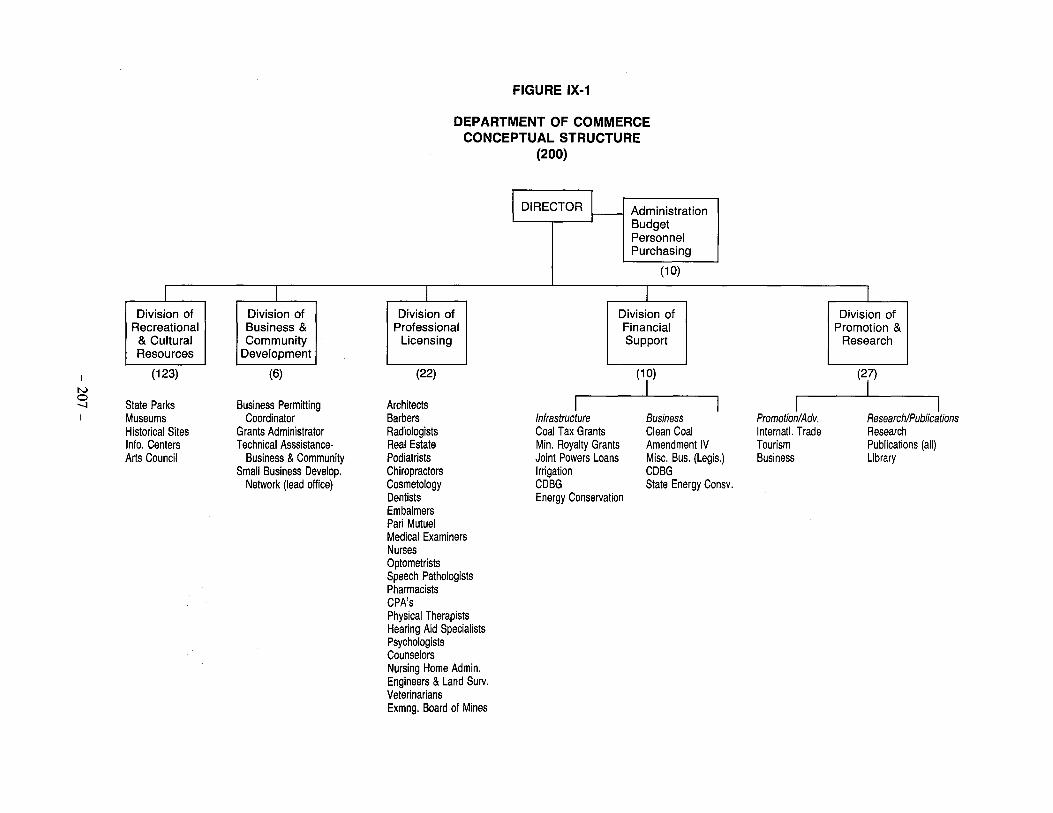

THE DEPARTMENT OF COMMERCE ......................... . • Division of Promotion and Research ........................... . • Division of Business and Community Development ............... . • Division of Financial Support ................................. . • Division of Professional Licensing ............................. . • Division of Recreational and Cultural Resources ................. . • Other Moves Suggested ...................... : ................ . • The Department's Proposed Organizational Structure ............. . • In Summary ................................................. .

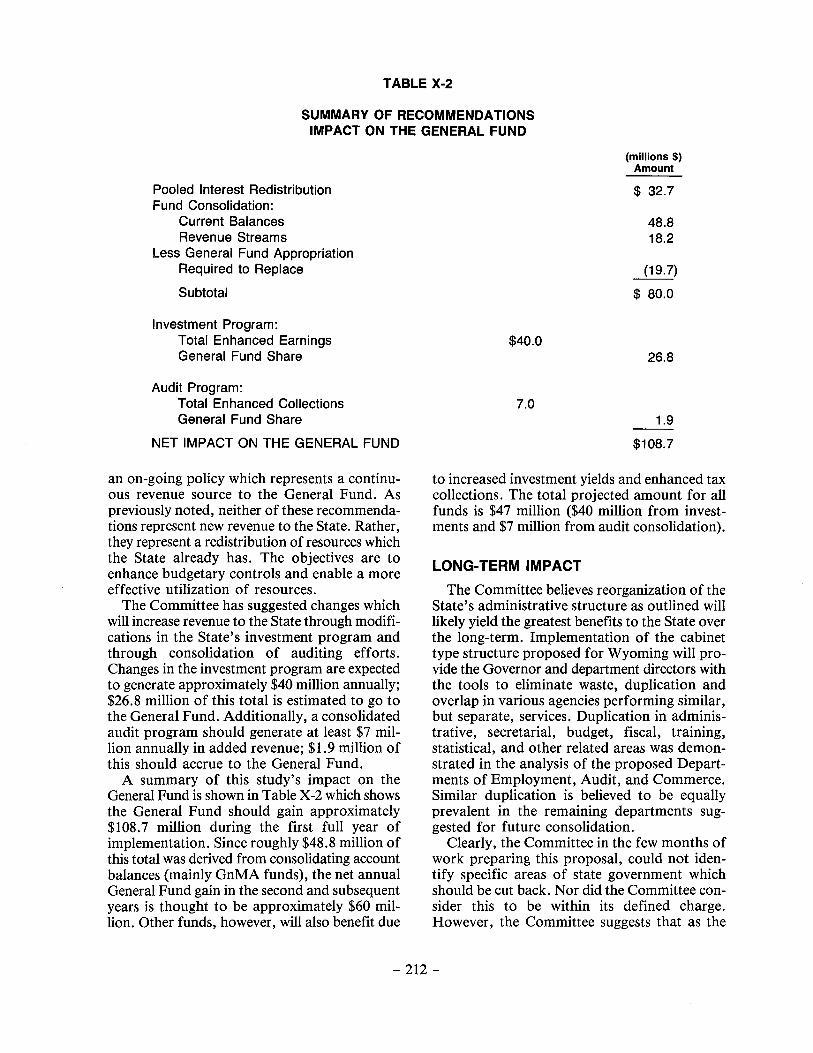

STUDY SUMMARY ........................................... . • Short-Term Revenue Shifts .................................... . • Long-Term Impact ........................................... . • Management Issues ........................................... .

-IX-

177 177 177 178 179 180 181 182 183 185 185 186 187 187 188 188 190 190

193 195 197 199 203 205 208 208 208

211 211 212 213

TABLE

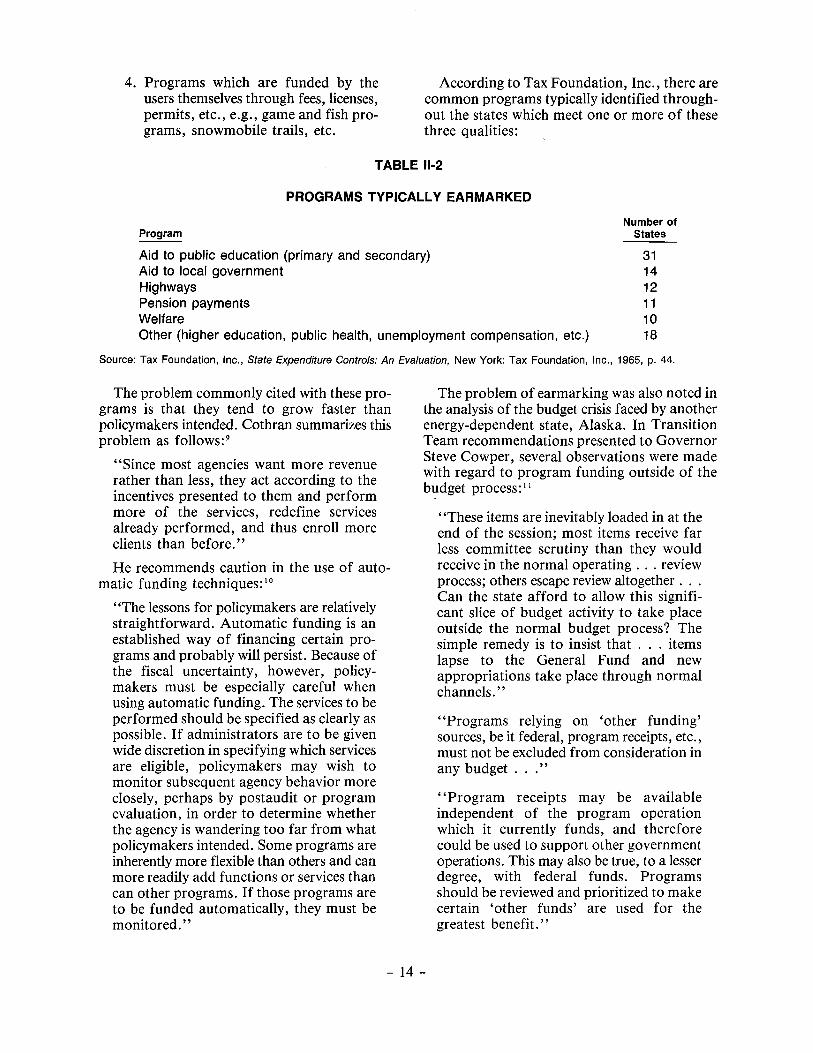

1-1 11-1 11-2 11-3

11-4 11-5 11-6 11-7

11-8 11-9 11-10 11-11 11-12 11-13 11-14 11-15 11-16 11-17 11-18

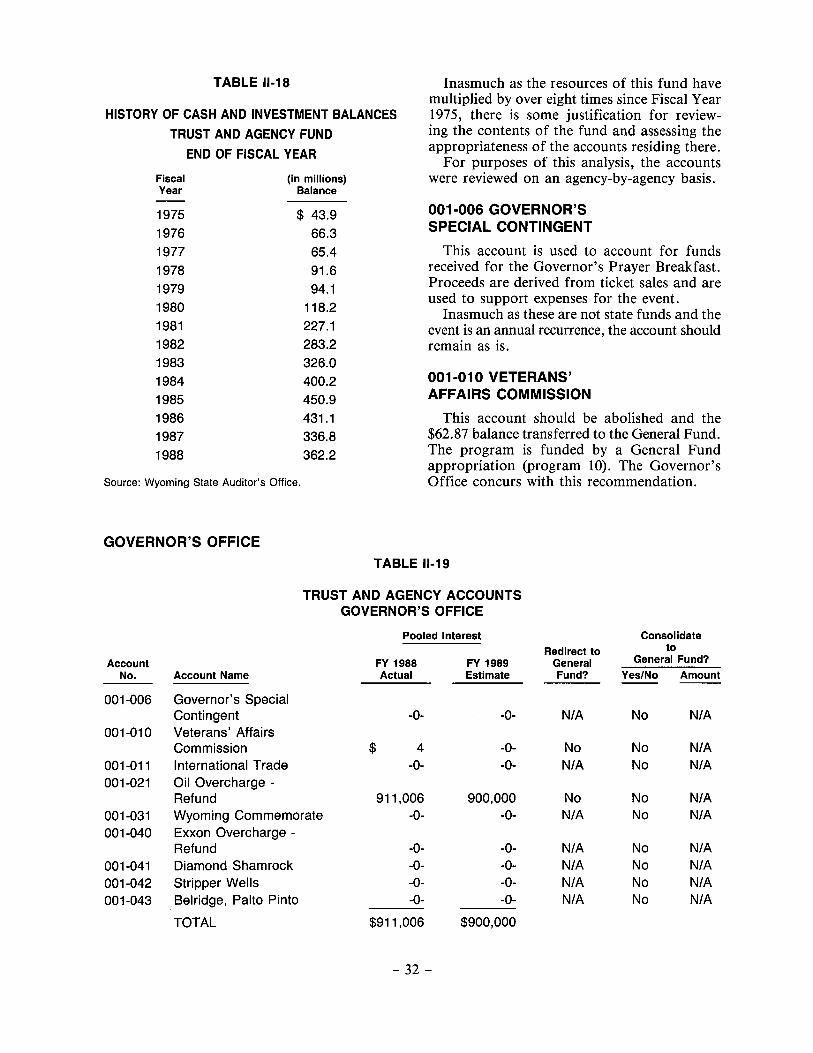

11-19 11-20 11-21 11-22 11-23

11-24 11-25 11-26 11-27

11-28 11-29

11-30 11-31 11-32 11-33

11-34 111-1

111-2 111-3 111-4

TABLES

Cash and Investment Balances, Selected Reserve Accounts .......... . Wyoming Fund Structure ....................................... . Programs Typically Earmarked .................................. . History of Cash and Investment Balances, Earmarked Revenue Fund, End of Fiscal Year ............................... . Groupings of Earmarked Fund Accounts ......................... . Higher Education Earmarked Fund Accounts ...................... . Elementary and Secondary Education, Earmarked Fund Accounts ... . Estimated Revenues, Expenditures and Cash Balances, Capital Construction Account ................................... . Appropriations to the School Foundation Program ................. . Professional Licensing .......................................... . Regulatory Boards and Commissions ............................. . Local Government Earmarked Accounts .......................... . Fiscal Profile, Water Development Account #1 .................... . Fiscal Profile, Water Development Account #2 .................... . Appropriations from Budget Reserve Account ..................... . Appropriations from Legislative Royalty Impact Assistance Account .. Fiscal Profile, Legislative Royalty Account ........................ . Other Earmarked Accounts ...................................... . History,of Cash and Investment Balances, Trust and Agency Fund, End of Fiscal Year. ...................... . Trust and Agency Accounts, Governor's Office .................... . Trust and Agency Accounts, State Auditor's Office ................ . Trust and Agency Accounts, State Treasurer's Office ............... . Trust and Agency Accounts, Department of Education ............. . Trust and Agency Accounts, Department of Administration and Fiscal Control ............................... . Trust and Agency Accounts, Department of Agriculture ............ . Trust and Agency Accounts, Department of Revenue and Taxation .. . Trust and Agency Accounts, Department of Environmental Quality .. . Trust and Agency Accounts, Economic Development and Stabilization Board ......................................... . Trust and Agency Accounts, Department of Public Lands .......... . Trust and Agency Accounts, Department of Health and Social Services ...................................... . Intragovernmental Fund ........................................ . Highway Fund ................................................. . Game and Fish Commission ..................................... . Summary of Recommendations, Enhancement to General Fund, Pooled Interest and Fund Consolidation .................... . Pooled Interest Distribution ..................................... . Major Increases in State Government Expenditure, Fiscal Year 1983 Through Fiscal Year 1987 ........................ . Certificates of Deposit, Varying Maturities ........................ . Processing and Depositing of Tax Receipts ........................ . Percentages of the Entire Wyoming Portfolio Invested in Repurchase Agreements .............................. .

-X-

PAGE

2 11 14

17 18 18 19

20 20 22 23 24 25 26 27 27 28 29

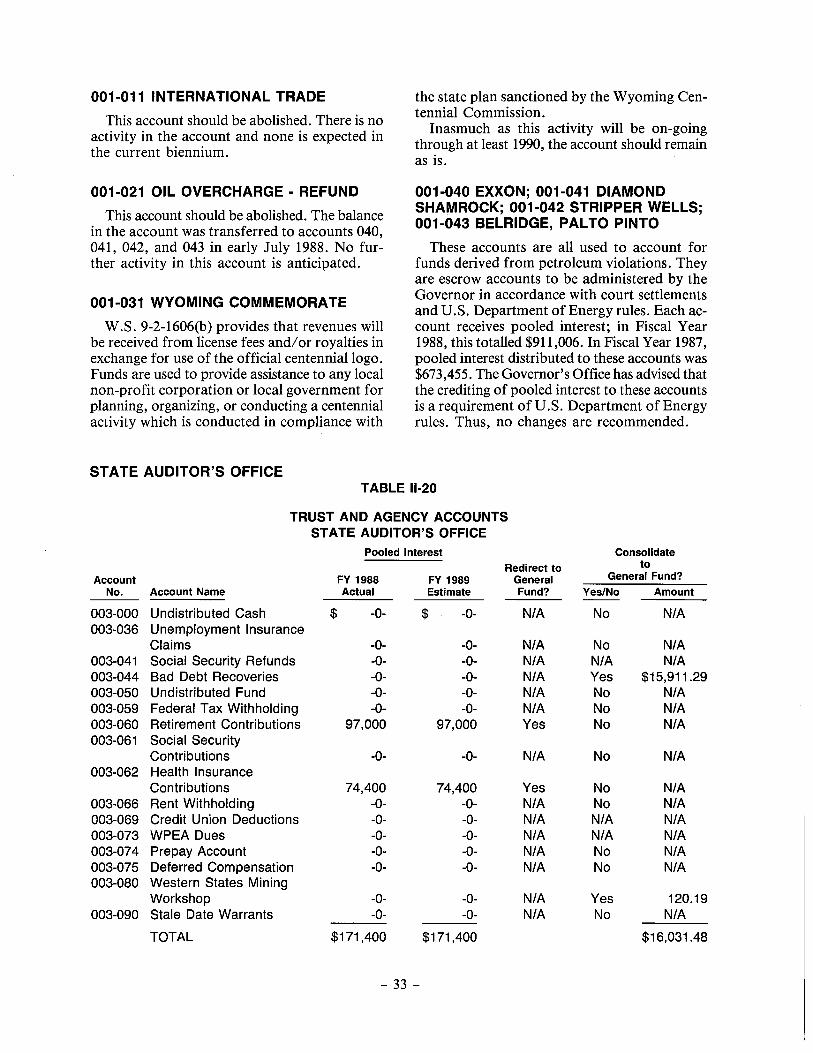

32 32 33 35 36

37 38 39 40

43 43

45 46 47 48

51 54

67 69 70

71

TABLE

III-5 III-6

III-7 III-8 III-9 III-10

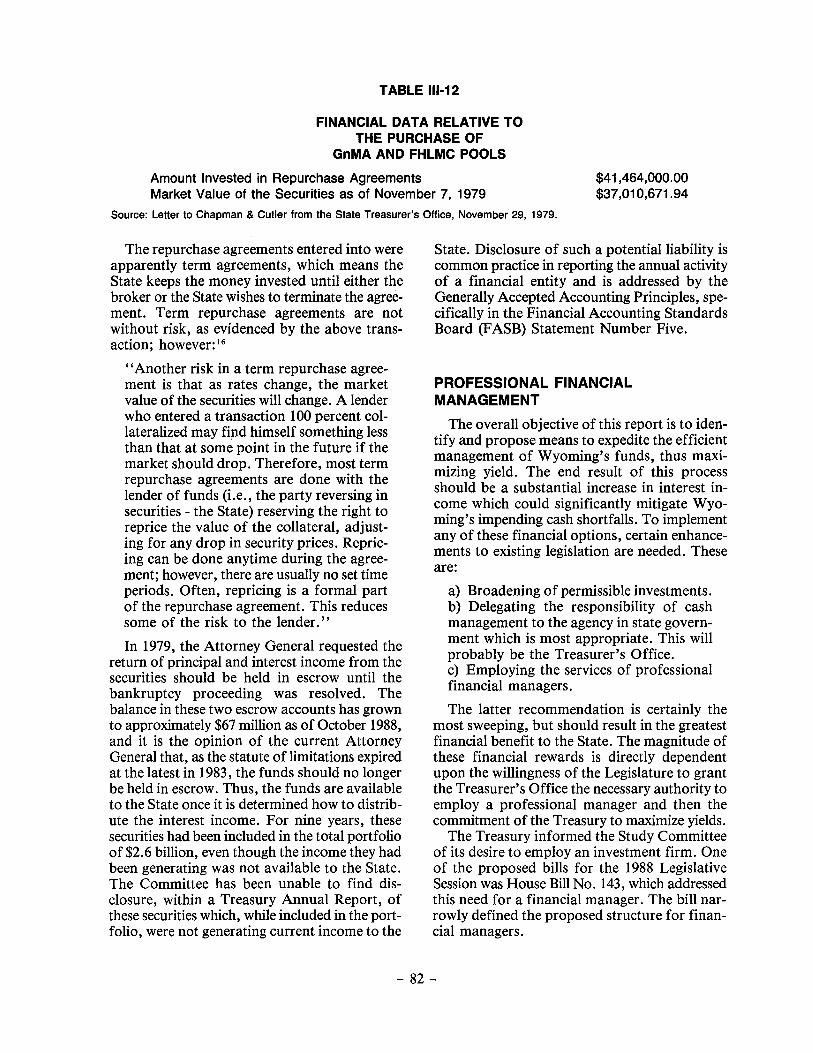

III-11 III-12

IV-1 IV-2

IV-3 IV-4

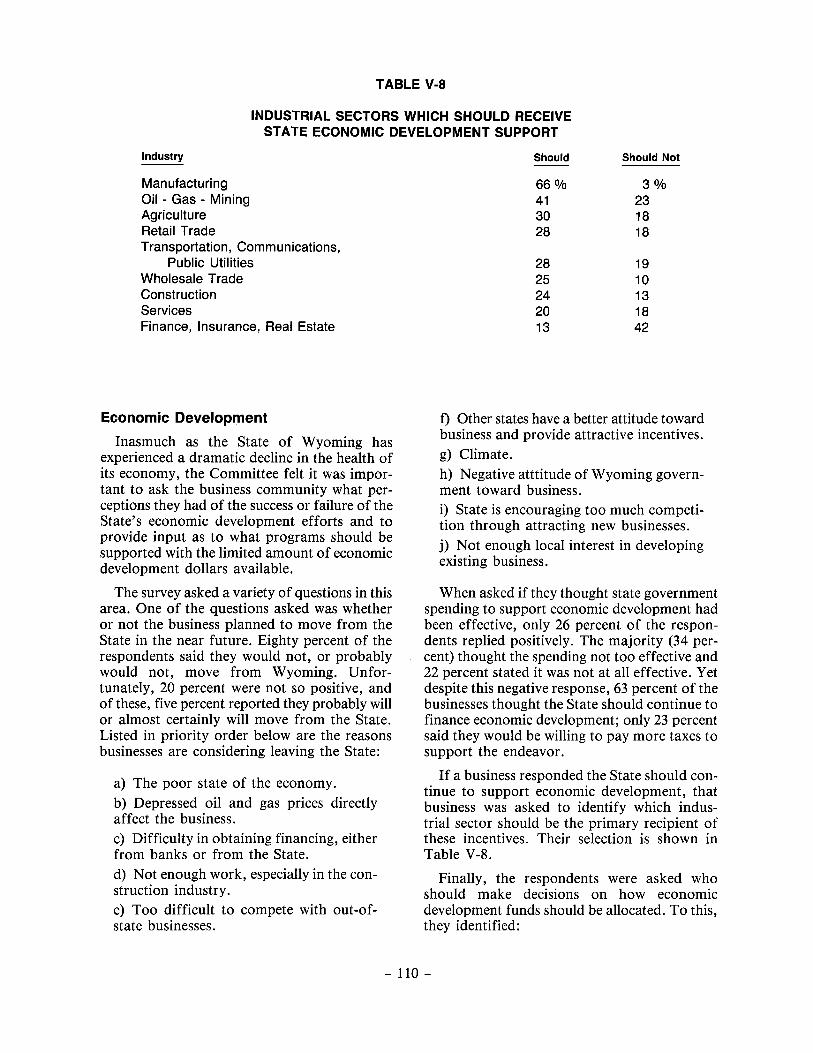

IV-5 V-1 V-2 V-3 V-4 V-5 V-6 V-7 V-8

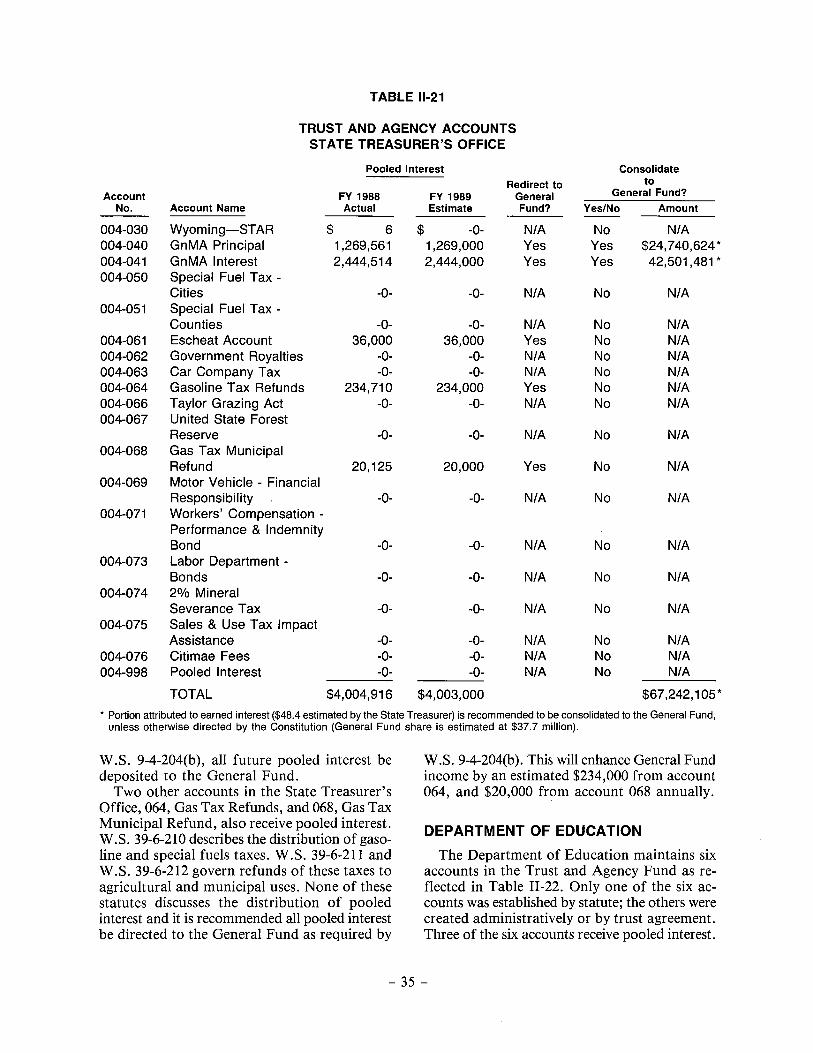

V-9 V-10 V-11

V-12 V-13 V-14 V-15 V-16 V-17 V-18 V-19 VI-1 VI-2

VI-3

VI-4 VII-1 VII-2 VII-3

VII-4 VII-5

Investment Instruments Authorized by Wyoming Statute ............ . Legislatively Mandated Investments, Balance of Permanent Funds Available June 30, 1987 ........................ . Overall Rate of Return Without Selected Loan Programs ........... . Yields and Investment Practices for Responding States ............. . Yield to Maturity on Long-Term Portfolios for Fiscal Year 1988 .... . Comparison of Wyoming Institution Deposits and FnMA Discount Notes ...................................... . Fiscal Year 1988 Rates of Return for the Wyoming Portfolio ........ . Financial Data Relative to the Purchase of GnMA and FHLMC Pools ................................... . Governor Appointment of Agency Directors ....................... . Governor Appoints Board, Commission or Council, Which Appoints Agency, Division or Program Manager ................... . Governor Appoints Boards ...................................... . Boards, Commissions and Councils with Hiring Authority Below the Level of Agency Director ..................... . Appointments Made by the Five Statewide Elected Officials ......... . Percentage of Respondents by Standard Industrial Classification ..... . Percentage of Respondents by Amount of Annual Sales ............ . Response to Business Survey, General Perceptions ................. . Agencies Identified as Overstaffed or Overfunded .................. . Agencies Identified as Understaffed or Underfunded ............... . Increase or Decrease in Government Expenditure Areas ............. . Forms Identified as Too Complex ..................... , .......... . Industrial Sectors Which Should Receive State Economic Development Support ................................. . Preferred Allocator of Economic Development Monies ............. . Practices Used by Businesses to Avoid Paying Taxes ............... . Most Effective Method of Eliminating Non-Compliance with Tax Laws ................................................. . Government Services Which Could be Privatized ................... . Response to Citizen Survey, General Perceptions ................... . Most Important Problems Wyoming Faces ........................ . Potential Government Action to Solve Problems ................... . Increase or Decrease in Government Expenditure Areas ............. . Businesses Which Should Receive Economic Development Support ... . Services Which Could be Privatized .............................. . Services for Which Fees Could be Charged or Increased ............ . Selection of Chief State School Officers .......................... . Gubernatorial Appointments to Boards, Commissions, Councils and Committees ....................................... . Boards, Commissions, Councils and Committees Not Requiring Gubernatorial Appointment ............................ . State Government Levels Held by Political Appointees ............. . Agency Staffing, Administrative/Statistical/Business Services ........ . Agency Staffing, Other ......................................... . States With a Single Agency for Workers' Compensation and Unemployment Insurance ................................... . Field Offices .................................................. . Annual Costs Associated With Payroll Reporting, ESC and Workers' Compensation ................................ .

-xi-

PAGE

73

76 77 78 79

80 80

82 91

92 92

93 93

105 105 106 106 107 107 108

110 111 111

112 112 113 114 114 115 115 115 121 139

143

147 149 170 170

170 171

172

TABLE

VII-6 VII-7 VII-8

VIII-1 VIII-2 IX-1

IX-2 IX-3 IX-4 X-1 X-2

Hearings and Appeals Process ................................... . Proposed Labor Standards, Hearings and Appeals Process .......... . Current Boards, Commissions, Councils of the Proposed Department of Employment ............................ . Statistics Pertinent to Current Audit Effort ....................... . Clarity of Wyoming Department of Revenue Statutes ............... . Current Boards, Commissions, Councils of the Proposed Department of Commerce .............................. . Economic Development Programs ................................ . Agencies/Boards to be Moved to the Department of Commerce ..... . Staffing Levels, Site Administration .............................. . Distribution of GnMA Funds .................................... . Summary of Recommendations .................................. .

- xii -

PAGE

172 173

174 181 186

194 200 204 206 211 212

FIGURE

I-1 I-2 III-1

IV-1 IV-2 IV-3 IV-4 VI-1 VI-2 VI-3 VI-4 VI-5 VII-1 VII-2 VII-3 VII-4 VII-5 VII-6 VII-7 VIII-1 IX-1

FIGURES

General Fund Revenues ......................................... . Declining Reserve Balances ...................................... . 18-Month Historical Trend, Treasury Bond Index and Federal Fund Rates ......................................... . Chain of Command, Industrial Organization ...................... . Chain of Command, Executive Branch Organization ............... . Current Structure of the Board of Charities and Reform ............ . Structure Based on Principles of Organization ..................... . Governor's Office .............................................. . Secretary of State .............................................. . State Auditor .................................................. . State Treasurer ................................................ . Proposed Organization for the State of Wyoming .................. . Employment Security Commission, Organization ................... . Department of Labor and Statistics, Organization .................. . Job Training Administration, Organization ........................ . Workers' Compensation Division, Organization .................... . Occupational Safety and Health, Organization ..................... . Vocational Rehabilitation Division, Organization ................... . Department of Employment, Conceptual Structure ................. . Department of Audit, Conceptual Structure ....................... . Department of Commerce, Conceptual Structure ................... .

- xiii -

PAGE

1 2

72 95 95

100 101 135 136 137 138 140 158 160 162 164 165 167 175 189 207

CHAPTER D

INTRODUCTION AND OVERVIEW "The hardest crossword puzzle to solve is the one in which we have penciled in a wrong word and are too stubborn or fixated to erase it; in much the same way, it is often easier to solve a problem when you are merely ignorant than when you are wrong."

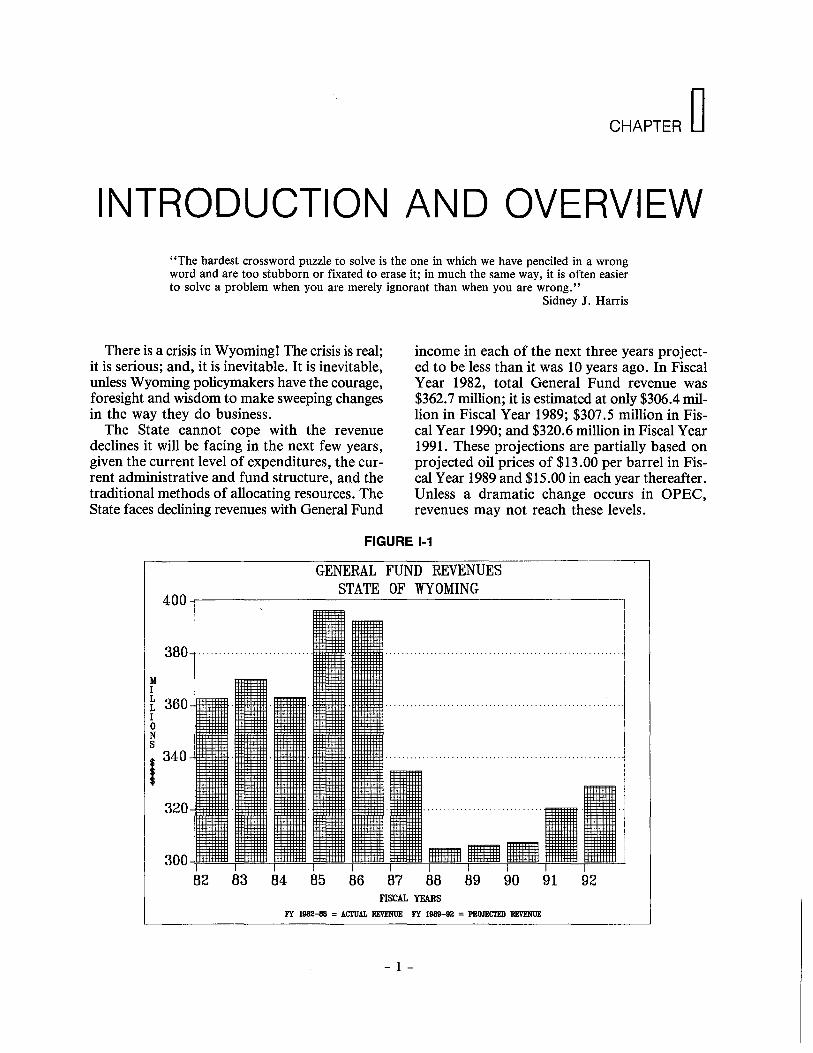

There is a crisis in Wyoming! The crisis is real; it is serious; and, it is inevitable. It is inevitable, unless Wyoming policymakers have the courage, foresight and wisdom to make sweeping changes in the way they do business.

The State cannot cope with the revenue declines it will be facing in the next few years, given the current level of expenditures, the current administrative and fund structure, and the traditional methods of allocating resources. The State faces declining revenues with General Fund

Sidney J. Harris

income in each of the next three years projected to be less than it was 10 years ago. In Fiscal Year 1982, total General Fund revenue was $362.7 million; it is estimated at only $306.4 million in Fiscal Year 1989; $307.5 million in Fiscal Year 1990; and $320.6 million in Fiscal Year 1991. These projections are partially based on projected oil prices of $13.00 per barrel in Fiscal Year 1989 and $15.00 in each year thereafter. Unless a dramatic change occurs in OPEC, revenues may not reach these levels.

FIGURE 1-1

GENERAL FUND REVENUES STATE OF WYOMING

400~-----------------------------------------.

!

M I

380 ········· ................ .

~ 360-tt±:I:IJ:ltt:l:tl· I 0 N s 1340

3 2 0 -!t±t:lltl±J±tl·

I i

················································ ·····J

300~~~~~~~~'""'-~-"'---i~~~~'---T'·~~=--r="'~ I I I

82 83 84 85 86 87 88 89 90 91 92 FISCAL YEARS

FY 1982-88 = ACI'UAL REVENUE FY 1989-92 = PROJECTED REVENUE

- 1 -

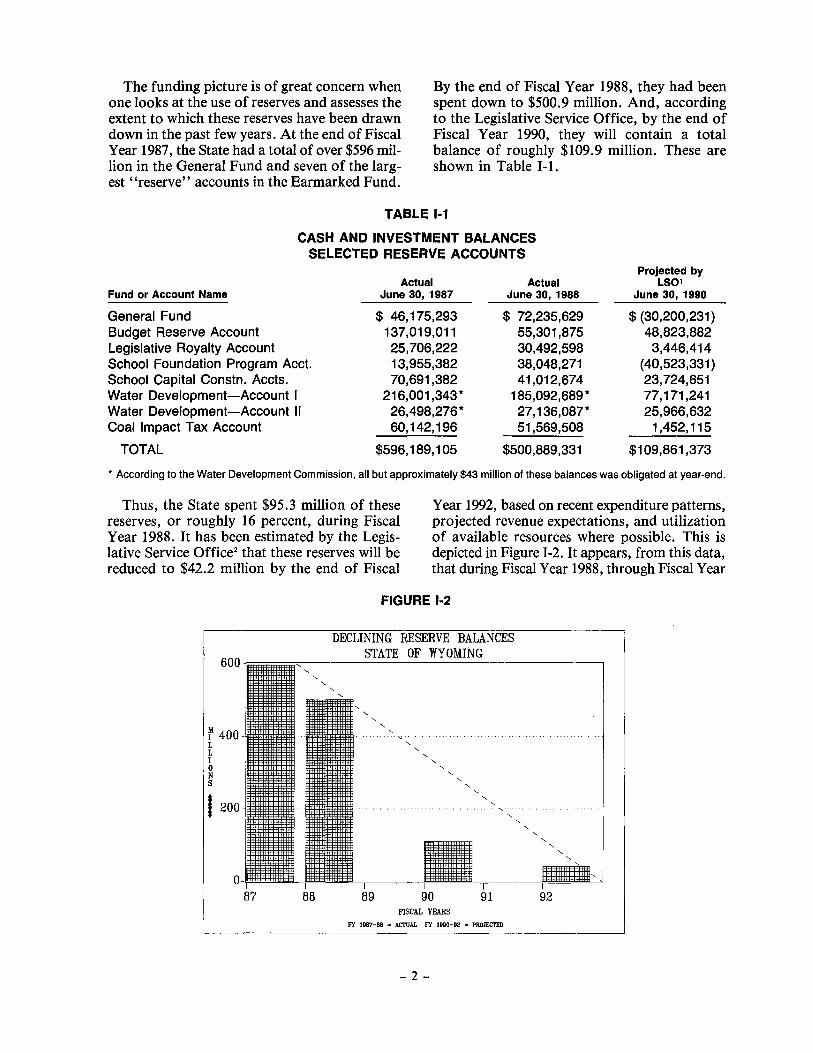

The funding picture is of great concern when one looks at the use of reserves and assesses the extent to which these reserves have been drawn down in the past few years. At the end of Fiscal Year 1987, the State had a total of over $596 million in the General Fund and seven of the largest "reserve" accounts in the Earmarked Fund.

By the end of Fiscal Year 1988, they had been spent down to $500.9 million. And, according to the Legislative Service Office, by the end of Fiscal Year 1990, they will contain a total balance of roughly $109.9 million. These are shown in Table I -1.

TABLE 1-1

CASH AND INVESTMENT BALANCES SELECTED RESERVE ACCOUNTS

Actual Actual Fund or Account Name June 30, 1987 June 30, 1988

General Fund $ 46,175,293 $ 72,235,629 Budget Reserve Account 137,019,011 55,301,875 Legislative Royalty Account 25,706,222 30,492,598 School Foundation Program Acct. 13,955,382 38,048,271 School Capital Constn. Accts. 70,691,382 41,012,674 Water Development-Account I 216,001 ,343 * 185,092,689 * Water Development-Account II 26,498,276* 27, 136,087* Coal Impact Tax Account 60,142,196 51,569,508

TOTAL $596,189,1 05 $500,889,331

Projected by LS01

June 30, 1990

$ (30,200,231) 48,823,882

3,446,414 (40,523,331) 23,724,651 77,171,241 25,966,632

1 ,452,115

$109,861 ,373

* According to the Water Development Commission, all but approximately $43 million of these balances was obligated at year-end.

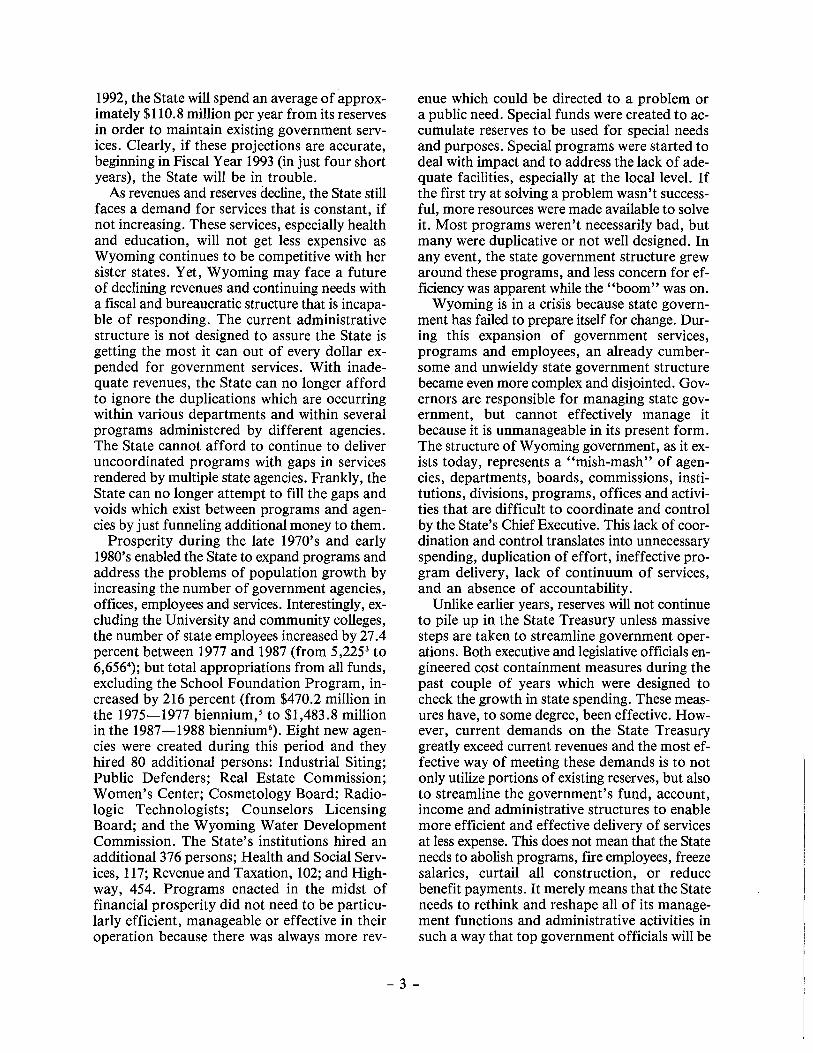

Thus, the State spent $95.3 million of these reserves, or roughly 16 percent, during Fiscal Year 1988. It has been estimated by the Legislative Service Office2 that these reserves will be reduced to $42.2 million by the end of Fiscal

Year 1992, based on recent expenditure patterns, projected revenue expectations, and utilization of available resources where possible. This is depicted in Figure 1-2. It appears, from this data, that during Fiscal Year 1988, through Fiscal Year

FIGURE 1-2

DECLINING RESERVE BALANCES STATE OF WYOMING

600·-~~---------l

r 4oo L L I 0 N s

88

' ' '''''"""''-.:"

'

89 90 FISCAL YEARS

91

FY 1987-88 = AcruAL FY 1990-92 = PROIECTED

-2-

1992, the State will spend an average of approximately $110.8 million per year from its reserves in order to maintain existing government services. Clearly, if these projections are accurate, beginning in Fiscal Year 1993 (in just four short years), the State will be in trouble.

As revenues and reserves decline, the State still faces a demand for services that is constant, if not increasing. These services, especially health and education, will not get less expensive as Wyoming continues to be competitive with her sister states. Yet, Wyoming may face a future of declining revenues and continuing needs with a fiscal and bureaucratic structure that is incapable of responding. The current administrative structure is not designed to assure the State is getting the most it can out of every dollar expended for government services. With inadequate revenues, the State can no longer afford to ignore the duplications which are occurring within various departments and within several programs administered by different agencies. The State cannot afford to continue to deliver uncoordinated programs with gaps in services rendered by multiple state agencies. Frankly, the State can no longer attempt to fill the gaps and voids which exist between programs and agencies by just funneling additional money to them.

Prosperity during the late 1970's and early 1980's enabled the State to expand programs and address the problems of population growth by increasing the number of government agencies, offices, employees and services. Interestingly, excluding the University and community colleges, the number of state employees increased by 27.4 percent between 1977 and 1987 (from 5,225 3 to 6,6564

); but total appropriations from all funds, excluding the School Foundation Program, increased by 216 percent (from $470.2 million in the 1975-1977 biennium, 5 to $1,483.8 million in the 1987-1988 biennium6

). Eight newagencies were created during this period and they hired 80 additional persons: Industrial Siting; Public Defenders; Real Estate Commission; Women's Center; Cosmetology Board; Radiologic Technologists; Counselors Licensing Board; and the Wyoming Water Development Commission. The State's institutions hired an additional376 persons; Health and Social Services, 117; Revenue and Taxation, 102; and Highway, 454. Programs enacted in the midst of financial prosperity did not need to be particularly efficient, manageable or effective in their operation because there was always more rev-

enue which could be directed to a problem or a public need. Special funds were created to accumulate reserves to be used for special needs and purposes. Special programs were started to deal with impact and to address the lack of adequate facilities, especially at the local level. If the first try at solving a problem wasn't successful, more resources were made available to solve it. Most programs weren't necessarily bad, but many were duplicative or not well designed. In any event, the state government structure grew around these programs, and less concern for efficiency was apparent while the "boom" was on.

Wyoming is in a crisis because state government has failed to prepare itself for change. During this expansion of government services, programs and employees, an already cumbersome and unwieldy state government structure became even more complex and disjointed. Governors are responsible for managing state government, but cannot effectively manage it because it is unmanageable in its present form. The structure of Wyoming government, as it exists today, represents a "mish-mash" of agencies, departments, boards, commissions, institutions, divisions, programs, offices and activities that are difficult to coordinate and control by the State's Chief Executive. This lack of coordination and control translates into unnecessary spending, duplication of effort, ineffective program delivery, lack of continuum of services, and an absence of accountability.

Unlike earlier years, reserves will not continue to pile up in the State Treasury unless massive steps are taken to streamline government operations. Both executive and legislative officials engineered cost containment measures during the past couple of years which were designed to check the growth in state spending. These measures have, to some degree, been effective. However, current demands on the State Treasury greatly exceed current revenues and the most effective way of meeting these demands is to not only utilize portions of existing reserves, but also to streamline the government's fund, account, income and administrative structures to enable more efficient and effective delivery of services at less expense. This does not mean that the State needs to abolish programs, fire employees, freeze salaries, curtail all construction, or reduce benefit payments. It merely means that the State needs to rethink and reshape all of its management functions and administrative activities in such a way that top government officials will be

- 3-

in a position to effectively manage the State's resources. A reduction in expenditures, "cutbacks," "down-sizing," and other cost containment benefits should be a natural outcome, as well as enhanced tax collections and investment earnings.

Though revenues are declining, the State still has substantial resources at its disposal, and the 1988 Legislature again used a portion of its reserves to keep state government afloat. It appears that as long as the State's reserves are available to supplement General Fund needs, Wyoming's policymakers have a tendency to continue to allocate these reserves in reaction to demands. Such practices, however, will be shortlived, for it also appears that the reserves which can be utilized without structural changes will soon be gone. And when reserves are gone, changes will be forced on the State whether it has planned for them or not.

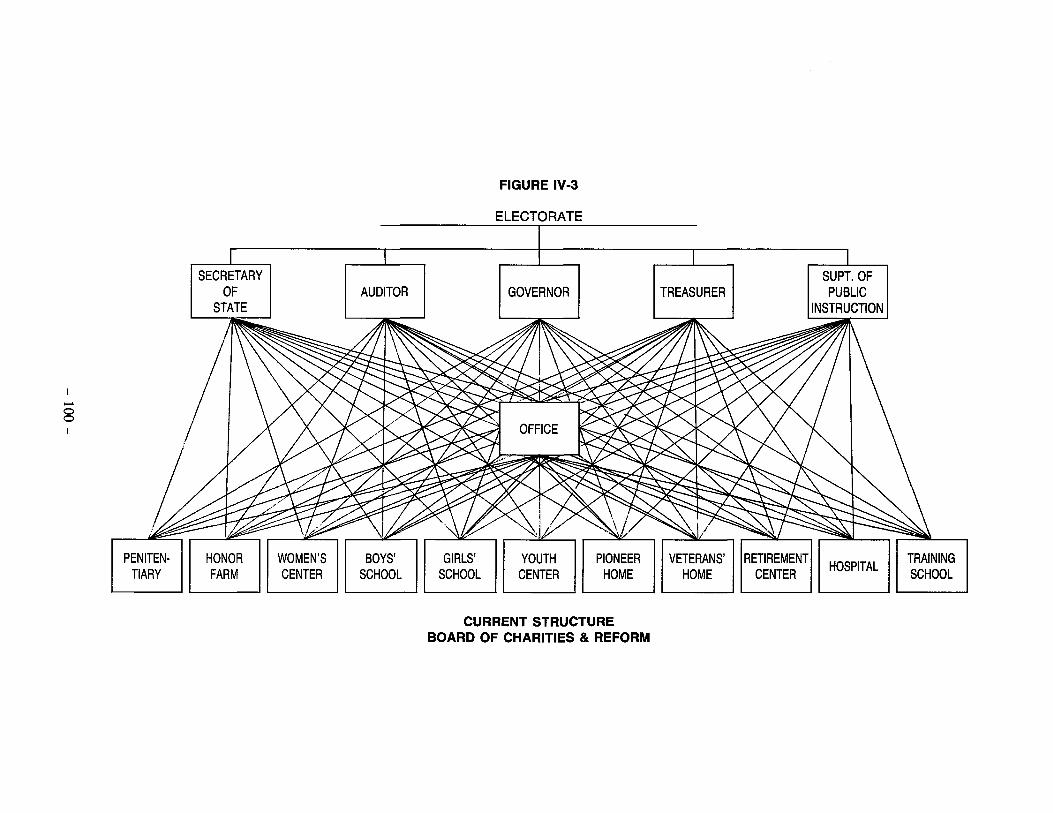

Little has been done to respond to this crisis. The State has an administrative structure very similar to what was in place in its early statehood in 1890. The structure is more cumbersome today because of the addition of boards, commissions, agencies, offices, functions and programs which have been created over the past 100 years. But the basic structure is the same. There are still five state elected officials, each with their area of limited responsibility and in concert, their joint responsibilities for the State's charitable and penal institutions. They also still serve on the State's Liquor Commission, State Land Board, Farm Loan Board, and others. And, serving in these various capacities, they still effectively eliminate the Governor's ability to efficiently manage any of these functions.

It was noted in the Joint Legislative-Executive Revenue and Expenditure Study' that there are some 108 boards, commissions, agencies, departments, institutions, districts and other separate entities in state government. Seventy-nine of these are in the Executive Branch, and each of these is either directly or indirectly the responsibility of the Governor. This structure can be described as a sprawling government, running along a horizontal plane. It can be depicted as 79 individual boxes, each representing a board, commission or agency, and each with a direct or indirect line connected to the Governor. The Governor is responsible for the hiring and firing of some agency or department directors, the appointment of board/commission members, and is responsible to see that the entities are

-4-

performing as intended in the most efficient and economical manner; but strong and indisputable statutory and constitutional authority to handle the State's affairs is not present. Some boards, commissions and councils function without a clear definition of their role or their responsibilities; many members do not understand the potential for the State's or their own personal liability due to conflicts of interest. They sometimes do not act in accordance with the Governor's prerogatives and, on occasion, actually undermine direction from the Executive Branch. No Governor, no matter how capable, can contend with such a dysfunctional administrative structure. Peter Drucker, 8 himself, would be hard pressed to describe how such a cumbersome, disjointed entity could be made to function efficiently.

It is because of this tremendously complex organization and the confusion surrounding its funding, with earmarking of funds and special accounts, that the 1988 Budget Session of the Wyoming Legislature authorized a study of state government efficiency.

STATE GOVERNMENT EFFICIENCY STUDY

Enrolled Act No. 52, Senate, Forty-Ninth Legislature of the State of Wyoming, 1988 Budget Session, was signed into law on March 14, 1988 by Governor Mike Sullivan. The Act is commonly referred to as the State Government Efficiency Study and the study's objective, scope and expected contents are generally defined in Section (1), paragraph (a): 9

"On or before January 1, 1989, a report shall be made to the legislature by the governor on the efficiency in state government and shall recommend abandonment, modification or combination of any agencies, departments, boards, commissions or other entities of the executive branch of state government or the creation of new departments and the termination or transfer into the general fund of all special accounts, as may be required for the most economical and efficient operation of state government. Drafts of any constitutional revisions and proposed legislation necessary to implement recommendations shall be included with the report as well as a complete accounting of funds expended for purposes of this section."

The Act created an eight-member Joint Legislative-Executive Committee to oversee the study. The President of the Senate appointed two members of the Senate to the Committee, Senators Alvin Wiederspahn and John Perry, while the Speaker of the House appointed Representatives Craig Thomas and Bill Rohrbach. Governor Mike Sullivan appointed Paul Cleary, Deputy State Land Commissioner, and Frank Galeotos, Manpower Planning Administrator, from the Executive Branch of state government. The Governor also appointed Rodger McDaniel and Robert Pettigrew, two citizens from the private sector, to contribute to the eight-member Committee. The Governor selected Mr. Pettigrew to serve as the Committee's Chairman.

An appropriation of $200,000 was contained in the Act to fund the study and the Cheyenne consulting group of Ferrari, Sommers & Washburn was contracted to conduct the study.

The legislation clearly called for recommendations to reorganize the administrative structure of state government when it addressed such topics as " ... modification or combination of any agencies, departments ... " It further required recommendations for the consolidation of funds and/ or accounts in the State Treasury, with language such as '' ... termination or transfer into the General Fund of all special accounts, as may be required for the most economical and efficient operation of state government.'' From these provisions, the focus of the required study was reasonably clear. However, in addition to these requirements, Governor Sullivan also requested that the study encompass a thorough investigation of the State's investment program. The Governor correctly observed that a study of "efficiency in state government" would be incomplete without such an analysis.

On June 13, 1988, the Joint LegislativeExecutive Efficiency Study Committee conducted its first meeting and the direction of the study was charted. It was decided the study would concentrate on three major topics: a study of the consolidation of funds and pooled interest; an analysis of the investment program and cash management techniques; and a study of the reorganization of the administrative structure of state government.

CONSOLIDATION OF FUNDS AND ANALYSIS OF POOLED INTEREST

In 1973, the Wyoming Funds Consolidation Act was enacted and the Legislature's policy with regards to funds coming into the State Treasury was specified: 10

"It is the policy of the Legislature that all general government programs, activities, and functions shall be subject to its review regardless of the sources of revenue ... except as otherwise provided."

Of course, one of the problems with having such a clear statement of legislative intent is that it is obvious when such policy is partially ignored. Clearly, if the Legislature intends to review all general governmental programs, activities and functions, regardless of funding source, then it ought to do so. If the Legislature has no intention of reviewing all general governmental programs, activities and functions, as has apparently been its desire for at least the last dozen years, then this language ought to be repealed or amended, for the Legislature has reviewed only a fraction of general government in recent sessions.

The consolidation of funds efforts of the Legislature in 1973 and 1974 resulted in the establishment of 13 funds in the State Treasury. For accounting purposes, the State Auditor created a 14th fund in 1986 to accommodate the accounting of Retirement System Accounts. Within these 14 funds, however, are nearly 750 accounts. And, nearly 500 of these are outside of the General Fund and thus are, for the most part, not subjected to legislative nor gubernatorial scrutiny through the State's budget process. The number of accounts escaping detailed analysis is probably not so important, as these are merely accounting entities necessary for some logical grouping and reporting of data. What is important is the amount of taxpayer funds contained in these 500 accounts. During Fiscal Year 1987, these 500 accounts received over $1 billion of the State's $1.4 billion in revenue ( exclusive of fiduciary-type funds), or roughly 71.1 percent of the total. Conversely, only 28.9 percent of the State's revenue was deposited to the General Fund and thus subjected to the budget process and made available for the support of general government operations. In other words, over $1 billion, or 71.1 percent of the State's resources were earmarked or allocated for other

- 5-

than general governmental operations. The crisis referred to earlier, then, may not be that of inadequate resources for state government, but rather of inadequate or inappropriate allocation of these resources. Chapter II attempts to examine this issue and present recommendations for consideration.

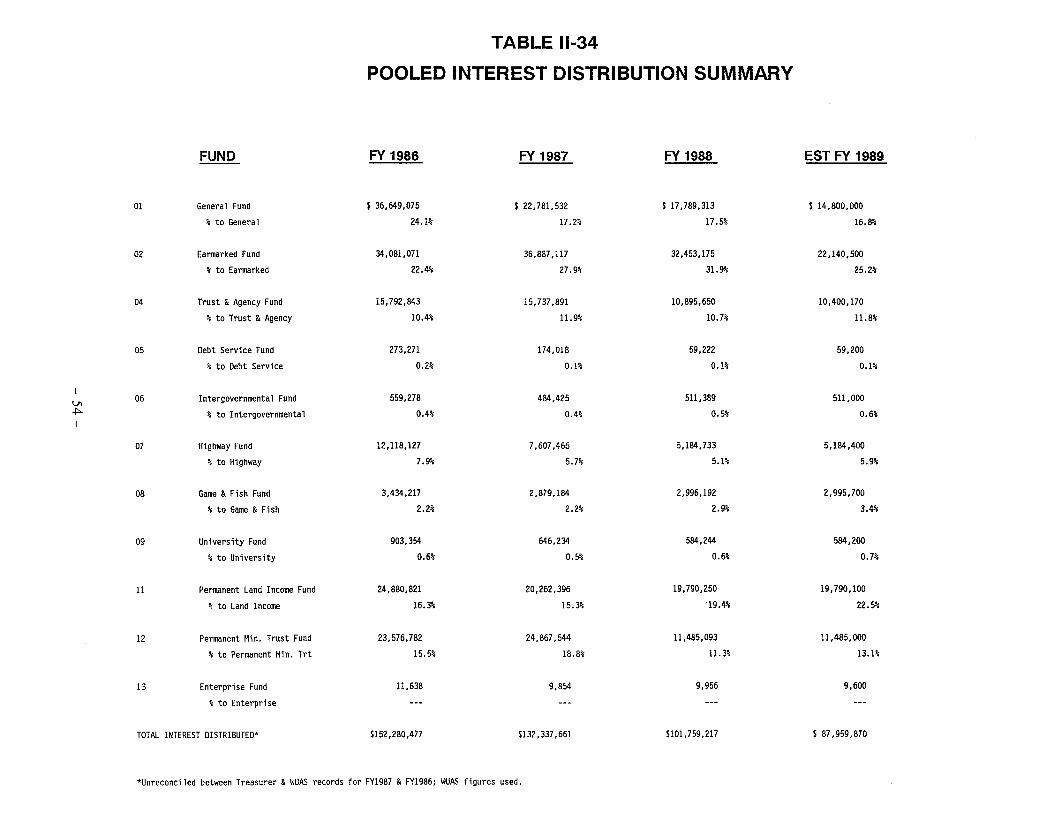

Chapter II also discusses and considers alternatives for the allocation of pooled interest. During the past three years, pooled interest in the State Treasury has been $152.3 million in Fiscal Year 1986, $132.3 million in Fiscal Year 1987, and $101.8 million last year. In all of these years, most of this interest was used for other than General Fund purposes. Including the pooled interest transferred from the Permanent Wyoming Mineral Trust Fund, the General Fund in fact received only $60.2 million in Fiscal Year 1986, $47.6 million in Fiscal Year 1987, and $29.3 million last year.

The Legislature's practice of diverting pooled interest to special projects or special interests is perhaps reflected in the total amount received by the Earmarked Fund, which has been the second largest receiver of this source. Last year, $32.5 million, or 31.9 percent of the total, was deposited here. In Fiscal Year 1987, it was $36.9 million, or 27.9 percent of the total, and in Fiscal Year 1986, it was $34.1 million, or 22.4 percent of the total.

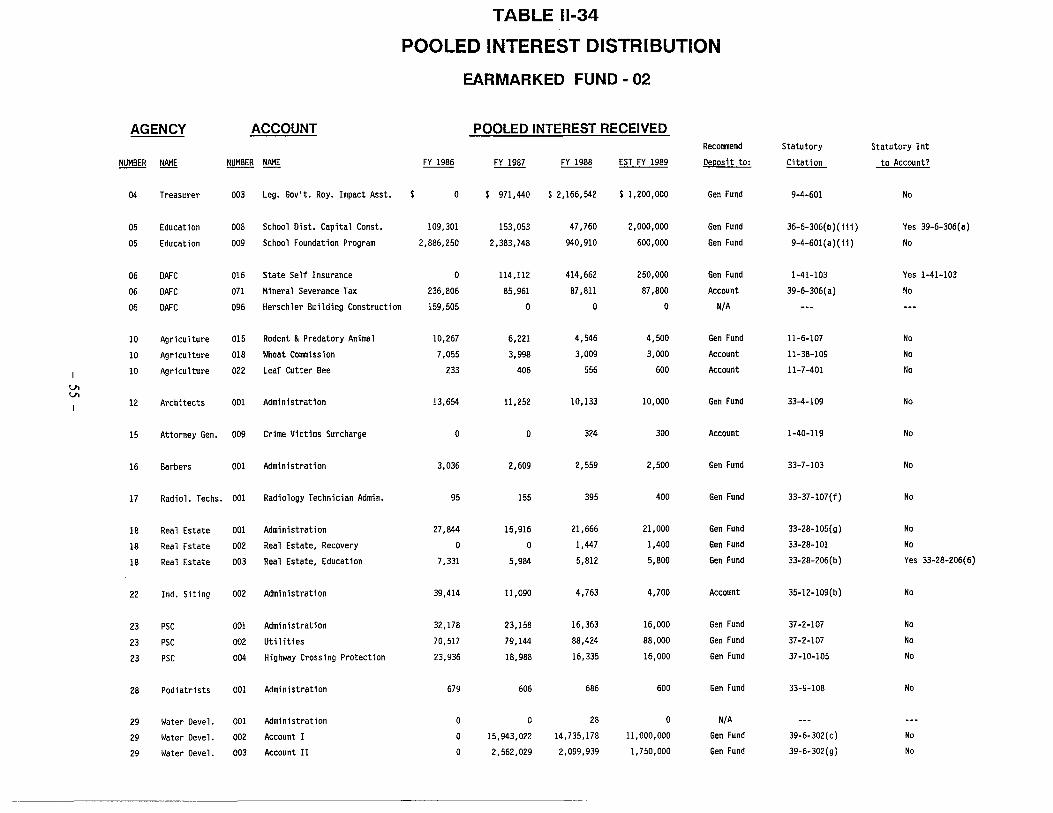

One of the problems associated with pooled interest is that often the deposition of this income is made in the absence of statutory guidance. Distributions are made to accounts within the State's funds on the basis of their average daily cash balances. Although this basis may be deemed appropriate, the method by which the accounts are selected to receive interest is questionable. Out of the total of nearly 500 accounts outside of the General Fund, only 209 have been credited with pooled interest; nearly 300 accounts received none. Most statutes are silent with regard to which accounts should or should not receive interest earnings. In these situations, the decision must be made administratively, and is. The decision is made on the basis of discussions between the State Treasurer's and the State Auditor's Offices. Although the decisions, over the years appear sensible and reasonable, it can be argued that many of them were made at the expense of the General Fund and they ought to be reviewed and perhaps challenged. Such is done in Chapter II, and recommendations for a redistribution of many interest earnings allo-

-6-

cations are accompanied by suggested enabling legislation.

INVESTMENT PROGRAM AND CASH MANAGEMENT TECHNIQUES

Governor Sullivan requested this topic be incorporated in the State Government Efficiency Study in an effort to find ways to increase the State's current yield on investments. The investment program is an integral part of the State's total revenue picture, generating from 12.6 percent to 12.9 percent of the State's total revenue (projected at $162.2 million to $171.9 million each year over the next three years, based on current yields). As the State's total budget resources continue to decline, investment income takes on an increasingly important role as one way to help endure the State's economic problems.

The State Treasurer, in 1988, reported an average yield on the State's investments of 7.37 percent. 11 This yield pertains to the State Treasury's entire portfolio, both short and long-term. In the recent financial markets, longer-term portfolios tended to yield higher returns than shortterm portfolios. Therefore, it is entirely possible that the State Treasury's yield on short-term (only) investments is significantly less than the 7.37 percent reported as the overall portfolio yield. The following yields from other states are included for informational purposes only and a more detailed comparison is included in Chapter III. The Treasurer's rate, although debatable, can be compared to the short-term working capital yield obtained by several other states: North Carolina, 9.137 percent; West Virginia, 7.86 percent; Texas, 7.40 percent; Alaska, 8.06 percent; and Oklahoma, 6.46 percent. Arguably, there are many factors to be considered when comparing one state's performance with the performance of another. Examples include: the portion of a state's portfolio which is dedicated to low interest, subsidy-type, loan programs; the mix of short-term versus long-term investments; the statutory level and degree of risk as it varies among the states; and the portfolio investment mix itself, i.e., portion of U.S. Treasury Notes, deposits in state banks, U.S. government backed mortgages, notes, bonds and debentures, dayto-day and term repurchase agreements.

In order to examine possible methods of increasing the State's investment yield, professional institutional investment experts were asked to study the State's investment portfolio, with the

objectives of: recommending alternative investment decisions; assessing the true rate of return (yield); and ascertaining the market value of the State's total portfolio. Such analysis excludes the State's legislatively mandated programs, concentrating only on the State's "discretionary" investment decisions. The outcome of this section of the study (Chapter III) is a formula for increasing the State's total yield by from one to three percent, which will generate anywhere from $20 to $57 million annually in additional revenue. Legislation necessary to enable desired changes in the State's investment program is suggested.

In conjunction with the analysis of the State's investment program, Chapter III of the study also discusses the State's cash management system, and touches on specific techniques, i.e., electronic fund transfers, lock box systems, and revenue and expenditure daily forecasting models. The objectives of this phase of the study are to point out not only procedures to get revenues into the State earlier, but also recognizes the need to more precisely forecast daily cash flow, so the State can shift more of its resources into the best performing investments, thus enhancing yields.

REORGANIZATION OF THE STATE'S ADMINISTRATIVE STRUCTURE

Like most states, Wyoming's organizational structure has basically been dictated by its economy. State government grew during the prosperous first two decades of the 1900's, and the State assumed the responsibility for services traditionally administered by local governments or private enterprise. 12 Post-war depression and reduced tax revenues resultant from decreased property valuations demanded a down-sizing in government in 1923 and 1925. During the late 1920's and 1930's, the expansion of federal government programs actually increased the number of state agencies as Wyoming responded to national policies formulated in response to the Great Depression. In 1933, the State, for the first time, systematically studied comprehensive reorganization and hired consultants to analyze the State's organization and revenue potential. The report, written by Griffenhagen & Associates, was ignored by lawmakers. Its suggestions were drastic and upsetting. 13 Some consolidation did take place independent of the formal study. Substantial salary cuts were enacted and admin-

istrative expenses were reduced by 30 percent from 1933 to 1939. 14

The push for government reorganization receded after 1939 as economic prosperity returned. During the next 30 years, the State's structure was largely modified in response to federal programs. The Great Society legislation of the 1960's had significant ramifications on states. New federal legislation, coupled with the State's economic and population growth, emphasized the need for the State to control its own destiny. 15 Better state government was the key to better home rule.

The most significant recent changes in state government organization occurred under the Hathaway administration, which began in 1967. A Commission on Government Reorganization and Constitutional Revision was created and within one year made sweeping recommendations to streamline state government operations.16 The basic findings were that the State had responded to additional federal programs by merely adding new departments, agencies and boards on a horizontal basis. These new units had been left without clear lines of authority or responsibility. 17

The 40th Legislative Session created the State Planning Coordinator, the Department of Economic Planning and Development, and the Department of Health and Social Services. The executive powers of the Governor were broadened and the Executive-Legislative Commission on Reorganization of State Government was established on a continuing basis. 18 In 1971, the Legislature ratified all four proposals the Commission submitted and created the Department of Administration and Fiscal Control, the Legislative Service Office, a lay Board of Parole, and a legislative budget session.

In 1973, the Department of Fire Prevention and Electrical Safety was created to encompass two previously independent agencies. The Environmental Quality Act was passed and consolidated six separate entities. The state police force was replaced with a special investigative unit, and the Funds Consolidation Act was passed. 19

In 1977, a proposed constitutional amendment to limit the number of state agencies, offices and boards to 20 failed to pass the Legislature. 20 The creation of the Department of Highways and Public Transportation was recommended to consolidate management of highways, air, rail, pipelines and public transportation, but a bill was not drafted. 21

- 7-

Little restructural organization has taken place since the Hathaway administration. The Commission on Reorganization of State Government died quietly and was formally abolished in statute in 1982. Despite the significant steps taken in the early 1970's to consolidate the State's operations, some of the efforts were piece-meal, subject to political compromise, and rendered somewhat inconsequential. Many agency structures are still weak in that lines of authority are muddled through board appointments of directors, or through gubernatorial appointment of administrators under department heads. The major power pockets in state government have not been touched by reorganization, and many boards and commissions still operate with little accountability.

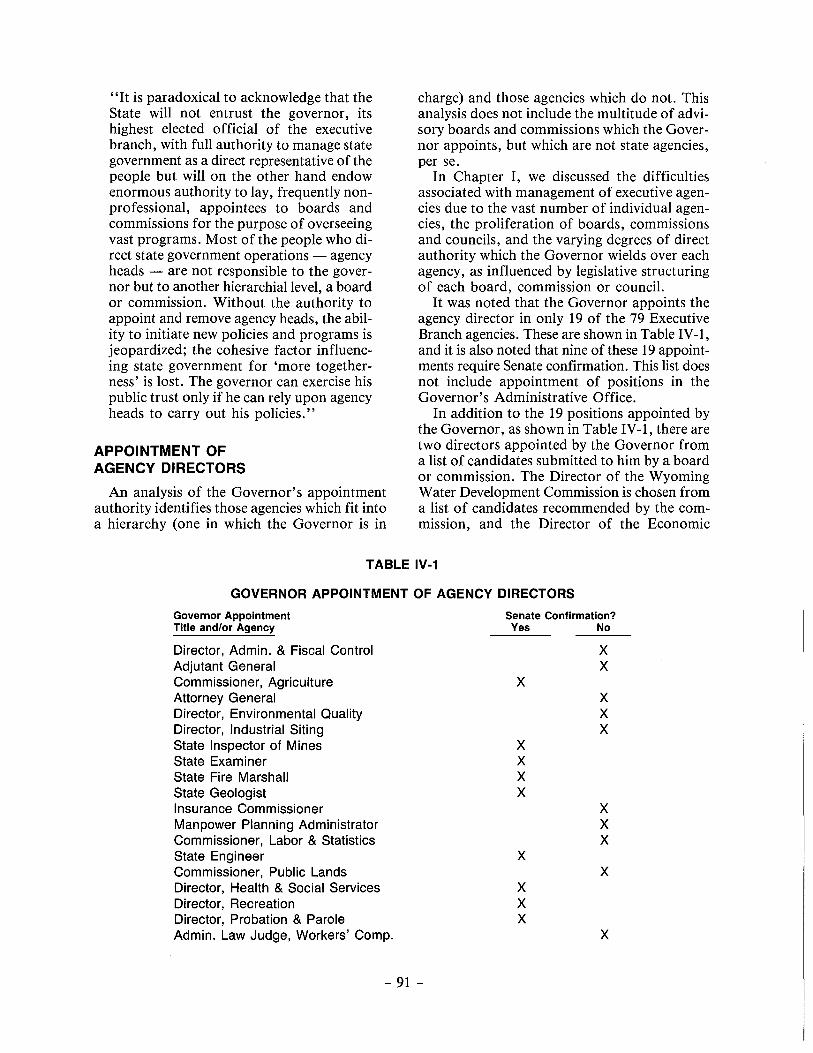

The Executive Branch of government is made up of 79 agencies. There are more than 100 boards, commissions and councils, with over 700 appointees involved in running the State's business. The dominance of boards and commissions is reflected in the fact that 52 of the 79 state agencies are run either by boards, commissions or councils, or the appointees of these bodies. The Governor, though he is held responsible by the State's citizenry, has little authority or control over most state activities, inasmuch as he singularly appoints and supervises only 19 directors of the operating agencies of state government. All other appointments require the approval of another authority, or are actually appointed by another authority.

The Revenue and Expenditure Study describes the confusion associated with the role and impact of so many different boards and commissions:22

''The state currently operates under a system which has agencies with no boards or commissions, agencies with one or more boards or commissions, boards and commissions with no agencies, and boards and commissions which act as agencies. Agencies are titled departments, divisions, offices, councils, commissions, and authorities; agency heads are called commissioners, directors, superintendents, coordinators, and executive directors."

The proliferation of boards and commissions in state government reflects Wyoming's philosophy of citizen input into the operations of its government. The expansion over the years in the membership and makeup of these boards, un-

fortunately, has mitigated their effectiveness and the cohesiveness of state government has been all but eliminated. The authority and power of the Governor has gradually deteriorated with this proliferation and has reached a point where, today, the Chief Executive has little capacity to manage this sprawling bureaucracy.

Most states over the past 30 years have experienced similar problems but have responded by undergoing a certain degree of reorganization. The basic premise of these efforts has been primarily to: concentrate more power in the Governor's office; consolidate similar functions along departmental lines; eliminate the adminstrative responsiblities of boards and commissions to reflect more of an advisory role; coordinate administrative services of all state entities; strengthen the Governor's control over budgeting and accounting; and provide the Legislature with more effective reporting and audit controls.

The Governor's span of control, with some 79 different executive agencies, is clearly in conflict with accepted management principles. According to one of the nation's leading authorities on management, Peter F. Drucker, the span of control: 23

" ... is rarely cited properly. It is not how many people report to a manager that matters. It is how many people who have to work with each other report to a manager. What counts are the number of relationships rather than the number of men (or women)."

Drucker went on to say that: 24

''The president of a company who has reporting to him a number of senior executives, each concerned with a major function, should indeed keep the number of direct subordinates to a fairly low number -between eight and twelve is probably the limit. For these men (and women) ... have to work with each other and with the company's president. If they do not work together, they do not work at all."

These observations from Drucker are focusing as much on the "sideways" relationships in an organization as they are on the vertical, superior/subordinate relationships. Drucker says we need to replace the traditional span of control concept with what he terms a more important concept - that of the span of managerial relationships. 25

- 8 -

The problem which has long been observed in state government is that the various agencies, though many are performing similar or related services, do not necessarily work together. Perhaps, as Drucker professes, they "do not work at all" as a result. The duplication of services, lack of coordination, and lack of continuum in our activities is no doubt an outgrowth from the fact that it is difficult for these 79 separate agencies of state government to work together. This has recently been recognized in some functional areas and, under new management direction, one or two functional groups have begun formal and frequent meetings to help eliminate conflicts and move toward common goals. One of the major objectives of this study is to present an administration whereby the various agencies are grouped according to the type and nature of the services performed, to present a manageable span of control so that the structure which results will enable these "sideways" relationships to take place and will provide the Governor with an administrative structure through which he can effectively manage state government. Chapters IV through X address this portion of the study.

IN SUMMARY

The study of efficiency and accountability in state government stemmed primarily from a recognition that Wyoming has experienced a period of declining revenues, reserves are being "tapped" to sustain the current level of government services, and a desire on the part of the Governor and the Legislature, to examine the current administrative and funding structures of state government.

Wyoming is facing a fiscal crisis. Though this crisis may not "hit" until sometime in Fiscal Year 1993, it is nonetheless real, and it is serious. Revenues are projected to remain at levels lower than those enjoyed 10 years ago, yet demands for public services and the outlays to support these services remain at all time highs. Reserves have had to be seriously depleted during the past few years in order to sustain these services. In fact, between June 30, 1987 and June 30, 1988, reserves in seven of the State's major

accounts were reduced by an estimated $95.3 million. It is expected the balances in these accounts will decline by an additional estimated $459 million over the next four years, leaving only $42.2 million by June 30, 1992.

The need for enhanced efficiency in state government is evidenced perhaps most clearly by the State's lack of an adequate auditing effort in the area of mineral severance taxes and ad valorem taxes. No consensus can be achieved as to the size of revenue losses experienced, but some experts indicate that the number is in the millions of dollars. Investment returns on the State's portfolio are also suspect, especially in relation to that enjoyed by several neighboring states. Enhanced interest earnings and collections of all taxes due are but two ways for the State to painlessly respond to the impending crisis.

The lack of an efficient administrative structure hampers the Governor's ability to manage and control state government. Due to the large number of boards, commissions, councils, agencies, departments and institutions, coordination of related programs is difficult, if at all possible. Relationships between and among entities performing similar or related services need improvement if the State is to maximize its effectiveness. Duplication and overlap of service deliveries are difficult to eliminate when they are occurring in possibly 79 different Executive Branch entities. Responsibility and authority are diffused and unclear due to the existence of 700 or more individuals serving in various capacities on boards, commissions, councils and committees.

This study is a joint effort of both the Legislative and Executive Branches of state government. Citizen input was also provided through the conduct of public hearings, opinion polls, surveys and questionnaires. The report which follows reflects no piecemeal reorganization suggestions and contains no political compromises. It is a comprehensive plan to enhance and improve state government efficiency, designed to be implemented in several phases over a period of years. It does not reflect the desires and pleasures of a select few, but rather embraces the needs and welfare of the public. The only special interests addressed are those of all the citizens of Wyoming.

-9-

FOOTNOTES-CHAPTER I

1. Jim Orr, Fiscal Specialist, Legislative Service Office, memo to members, 49th Wyoming Legislature, "Enclosed Fiscal Profiles," October 27, 1988.

2. Jim Orr, Fiscal Specialist, Legislative Service Office, memo to members, 49th Wyoming Legislature, "Final Green Sheets," March 15, 1988.

3. James B. Griffith, Wyoming State Auditor, Appropriations and Employment in Wyoming Government, for the Biennial Periods 1975-77 through 1985-86, February 1, 1986, p. 13.

4. Research and Statistics Division, Administration and Fiscal Control, Wyoming Data Handbook 1987, December 31, 1987, p. 107.

5. James B. Griffith, op. cit., pp. 36, 41 and 42. 6. Mike Sullivan, Governor, 1989-90 State Budget,

December 1, 1987, p. xiii. 7. David G. Ferrari, Ruth C. Sommers and Janet E.

Washburn, Wyoming, 1988, A Study of Revenue and Expenditures, Volume II, State of Wyoming Joint Legislative-Executive Committee, January 1988, p. 4.

8. Peter F. Drucker is one of the nation's leading management experts. Mr. Drucker was professor of management at the Graduate Business School of New York University from 1950 to 1972. Since 1972, he was the Distinguished University Lecturer at New York University and since 1971, he has been Clarke Professor of Social Science at the Claremont Graduate School, Claremont, California. His books in-

elude: The New Society, The Effective Executive, The Practice of Management, America's Next Twenty Years, Landmarks of Tommorrow, Managing for Results, The Age of Discontinuity, and two volumes of essays, Technology, Management and Society and Men, Ideas and Politics.

9. Chapter 57, Session Laws of Wyoming, 1988, p. 136. 10. Wyoming Statutes, Cummulative Supplement, June

1987, Section 9-4-202. 11. Wyoming State Treasurer Annual Report, 1988, p.

16. 12. Nancy Bedont, The History of Government Reor

ganization in the State of Wyoming, July 20, 1977, p. 16.

13. Ibid., p. 36. 14. Ibid., p. 44. 15. Ibid., p. 54. 16. Ibid., p. 55. 17. Ibid., p. 56. 18. Ibid., p. 59. 19. Ibid., p. 64. 20. Ibid., p. 70. 21. Ibid., p. 68. 22. Ferrari, Sommers & Washburn, op. cit., p. 507. 23. Peter F. Drucker, Management Tasks, Responsibil

ities and Practices, Harper and Row, Publishers, 1974, p. 412.

24. Ibid. 25. Ibid., p. 413.

-10-

CHAPTER 0 0

FUND CONSOLIDATION AND POOLED INTEREST

"Adde parnum parvo magnus acervus erot. "a

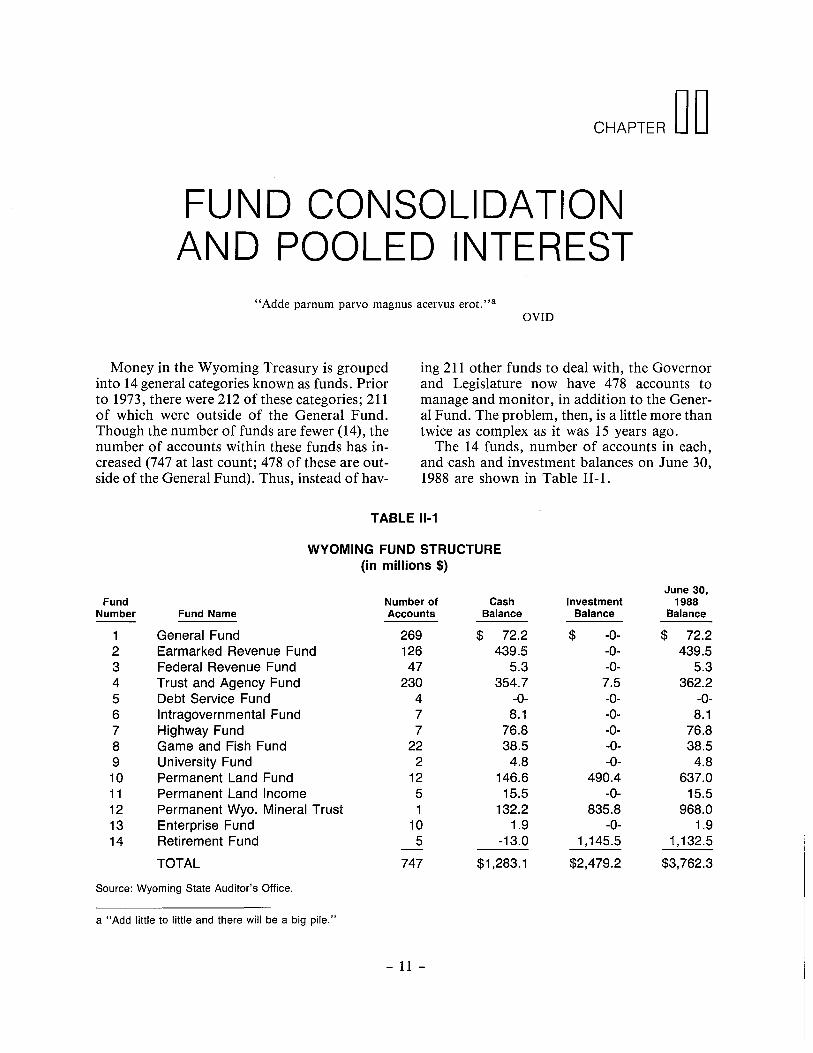

Money in the Wyoming Treasury is grouped into 14 general categories known as funds. Prior to 1973, there were 212 of these categories; 211 of which were outside of the General Fund. Though the number of funds are fewer (14), the number of accounts within these funds has increased (747 at last count; 478 of these are outside of the General Fund). Thus, instead of hav-

OVID

ing 211 other funds to deal with, the Governor and Legislature now have 478 accounts to manage and monitor, in addition to the General Fund. The problem, then, is a little more than twice as complex as it was 15 years ago.

The 14 funds, number of accounts in each, and cash and investment balances on June 30, 1988 are shown in Table 11-1.

TABLE 11-1

WYOMING FUND STRUCTURE (in millions $)

Fund Number of Cash Number Fund Name Accounts Balance

1 General Fund 269 $ 72.2 2 Earmarked Revenue Fund 126 439.5 3 Federal Revenue Fund 47 5.3 4 Trust and Agency Fund 230 354.7 5 Debt Service Fund 4 -0-6 lntragovernmental Fund 7 8.1 7 Highway Fund 7 76.8 8 Game and Fish Fund 22 38.5 9 University Fund 2 4.8 10 Permanent Land Fund 12 146.6 11 Permanent Land Income 5 15.5 12 Permanent Wyo. Mineral Trust 1 132.2 13 Enterprise Fund 10 1.9 14 Retirement Fund 5 -13.0

TOTAL 747 $1,283.1

Source: Wyoming State Auditor's Office.

a "Add little to little and there will be a big pile."

- 11 -

June 30, Investment 1988

Balance Balance

$ -0- $ 72.2 -0- 439.5 -0- 5.3 7.5 362.2 -0- -0--0- 8.1 -0- 76.8 -0- 38.5 -0- 4.8

490.4 637.0 -0- 15.5

835.8 968.0 -0- 1.9

1,145.5 1 '132.5

$2,479.2 $3,762.3

The conditions which led to the Funds Consolidation Act in 1973 were not unlike the conditions found in Wyoming government today. That is, there were a large number of accounts containing significant sums of money which were never contained in the executive budget and therefore were not analyzed and scrutinized in a consistent manner. The existence of numerous funds and accounts, with revenues being transferred between funds and between accounts within the same funds, and with expenditures being made directly from some funds and accounts but not from others, has resulted in confusion, misunderstandings and uncertainty about the State's finances. The example which follows may serve to illustrate this problem. John Doe and his wife, Jane, receive income from five sources:

John's Salary Jane's Salary Stocks Rental Income John's Second Job

$20,000/yr. 10,000/yr. 1,000/yr. 6,000/yr. 5,000/yr.

$42,000/yr.

John deposits his salary in a checking account from which most monthly bills are paid. Jane's salary is deposited in a different checking account and if John's account balance is insufficient to pay the bills, Jane transfers money by check into John's account. She also buys groceries occasionally from her account, and purchases a few other items from time to time.

The stock account income is split: 50 percent is allocated as a savings account for their son and 50 percent is earmarked into a savings account to build up until they can buy a new car. The rental income is placed in a broker's account for stock purchases unless the money is needed for a vacation, in which case they buy traveler's checks from Jane's checking account and then reimburse it from the broker's account. Income from John's second job is put into the cookie jar and periodically used to pay the paperboy, library fines, movie rentals, etc.

When Internal Revenue Service audits John's tax returns, he says he is not quite sure of his income or expenses. John does not think the stock income should count since, in part, it is being saved for his son unless it is needed for the car. Because John's expenses are paid from five different accounts, as well as the cookie jar, John is not quite sure which of these are deduct-

ible. John thinks that the best thing would be for him to review all of his income, expenditures and transfers before the IRS can make any final decisions.