Embed Size (px)

Citation preview

2002 NCCI Holdings, Inc.

Analysis of Workers Compensation Loss TrendsUnderstanding and Modeling the Change in Frequency

Recent Research Findings from NCCI

Casualty Loss Reserve Seminar

Casualty Actuarial Society

September 23, 2002

Presented by

Harry Shuford

Chief Economist

2 2002 NCCI Holdings, Inc.

Analysis of Workers Compensation Loss TrendsUnderstanding and Modeling the Change in Frequency

Outline

1. Key Findings

2. Some Insights from the Bureau of Labor Statistics • Trends and Cycles in Workplace Injuries• The 1990’s Were Different• But the US Was Not• Wal-Mart Told Us - It’s Just Business

3. Applying the Knowledge to Support Loss Cost Filings

3 2002 NCCI Holdings, Inc.

Looking at Three Decades of Experience

The key findings include:

Frequency changes are cyclical around a long-term tendency to decline.

Over long periods of time the relative importance of these two factors varies considerably.

4 2002 NCCI Holdings, Inc.

Looking at Three Decades of Experience

The key findings include:

Swings in the business cycle, especially as reflected in changes in employment, are associated with similar swings in frequency –

downward pressure in recession

upward pressure during periods of robust growth.

5 2002 NCCI Holdings, Inc.

Looking at Three Decades of Experience

The key findings include:

The 1990s diverge from earlier periods;

the business cycle effects were present but

were overcome by changes in the workplace as reflected by marked improvements in productivity.

6 2002 NCCI Holdings, Inc.

The Industry Wants to Know:

• What Happened in the 1990s?

• Can It Continue?

• The Approach – Compare Areas with Dramatic Declines vs. Those with Limited Declines and Increases – Identify Key Underlying Differences

• It Didn’t Get Us Very Far!

7 2002 NCCI Holdings, Inc.

It Is Useful to Understand Why It Didn’t Work

Why?

Because the decline has been broad-based –

across industries and occupations and across virtually all injury “demographics” including

age, gender, event, source, body part injured, tenure with employer.

8 2002 NCCI Holdings, Inc.

The key findings include:

In spite of the dramatic declines

There is virtually no change in the relative position of industries and occupations.

In general

The most risky remain the most risky;

The safest are still the safest. Relative shifts from high to lower frequency was not a factor

9 2002 NCCI Holdings, Inc.

Searching for the Factors Driving the Change in Frequencywith Special Interest in the Decline of the 1990s

The key findings include:

In spite of the diverse nature of the decline at least one clear factor stands out

the dramatic decline in back injuries outstrips the declines in all other injury categories.

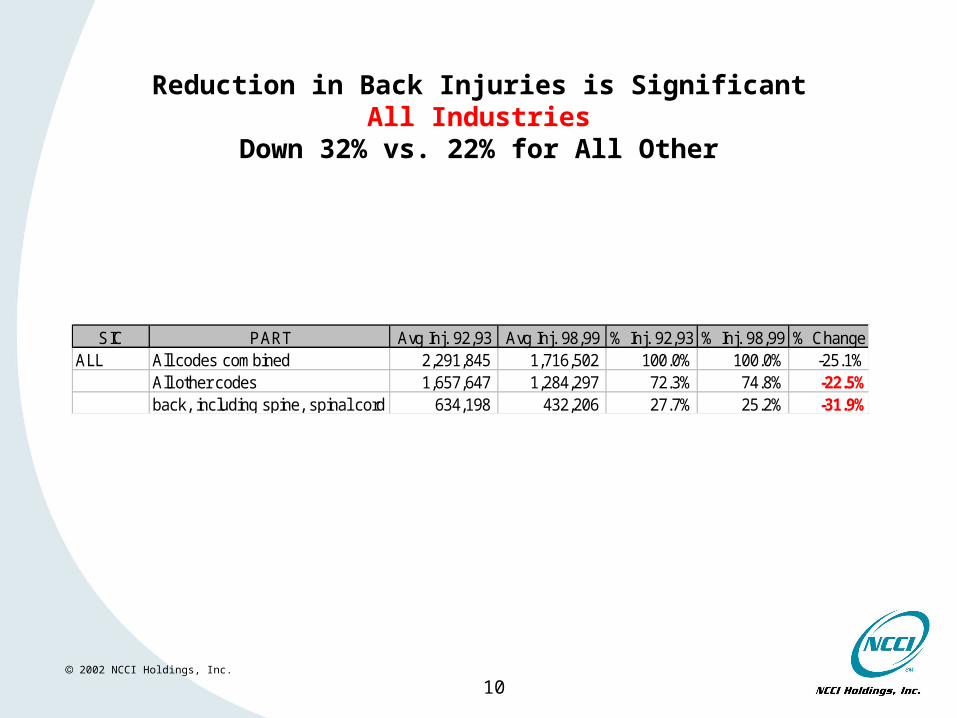

10 2002 NCCI Holdings, Inc.

Reduction in Back Injuries is SignificantAll Industries

Down 32% vs. 22% for All Other

SIC PART Avg Inj. 92,93 Avg Inj. 98,99 % Inj. 92,93 % Inj. 98,99 % ChangeALL All codes combined 2,291,845 1,716,502 100.0% 100.0% -25.1%

All other codes 1,657,647 1,284,297 72.3% 74.8% -22.5%back, including spine, spinal cord 634,198 432,206 27.7% 25.2% -31.9%

11 2002 NCCI Holdings, Inc.

Trends and Cycles in Workplace Injury Rates

The Longer Term View

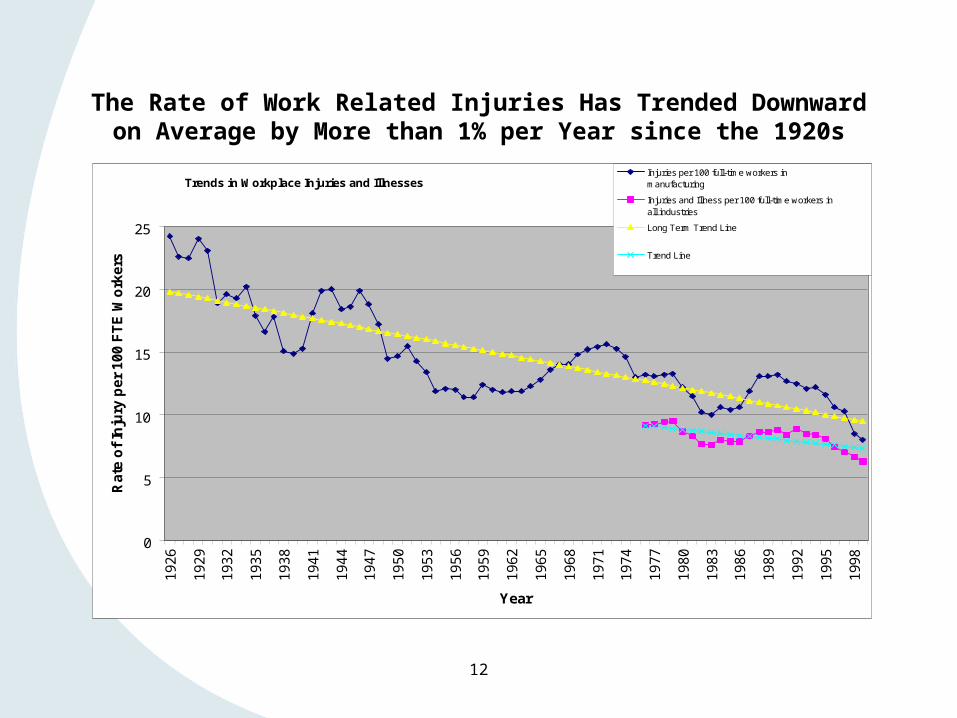

The Rate of Work Related Injuries Has Trended Downwardon Average by More than 1% per Year since the 1920s

Trends in Workplace Injuries and Illnesses

0

5

10

15

20

25

19

26

19

29

19

32

19

35

19

38

19

41

19

44

19

47

19

50

19

53

19

56

19

59

19

62

19

65

19

68

19

71

19

74

19

77

19

80

19

83

19

86

19

89

19

92

19

95

199

8

Year

Ra

te o

f In

jury

per

100 F

TE

Wo

rkers

Injuries per 100 full-time workers in manufacturing Injuries and Illness per 100 full-time workers in all industries Long Term Trend Line

Trend Line

12

13 2002 NCCI Holdings, Inc.

What can explain this tendency for frequency to decline over extended periods of time?

According to the Federal Reserve Bank of Dallas

Competitive labor markets require continuing improvement in working conditions and productivity

Source: “Have a Nice Day”, Annual Report 2000, Federal Reserve Bank of Dallas

14 2002 NCCI Holdings, Inc.

OK – the Long Term Decline Makes Sense

How about Short Term Movements?

________________________________

Frequency Typically Tracks with the Business Cycle

2002 NCCI Holdings, Inc.

This Is Not a New Idea

• “There is a tendency for the frequency rate of industrial injuries to move up and down with the volume of employment, as shown by an analysis of injuries in manufacturing industries from 1936 to 1941….The data for 1936 to 1941 reinforce the findings of an earlier study by the Bureau, for the years 1929 to 1936.”

• Depression – falling employment War build up – growing employment• frequency down frequency up

• Most recently added laid off first New, inexperienced workers• Lay-offs lagging decline in production Lengthening of the workweek• In spite of decline in safety programs Failure of safety activities to keep pace• Least efficient, less safe equipment idled Crowding and congestion in plants

operating well above design capacity

• Under reporting of minor injuries• Trained workers lost to the armed forces• Monthly Labor Review, March 1938 Monthly Labor Review, May 1943

16 2002 NCCI Holdings, Inc.

Looking at A Quarter Century of Experience

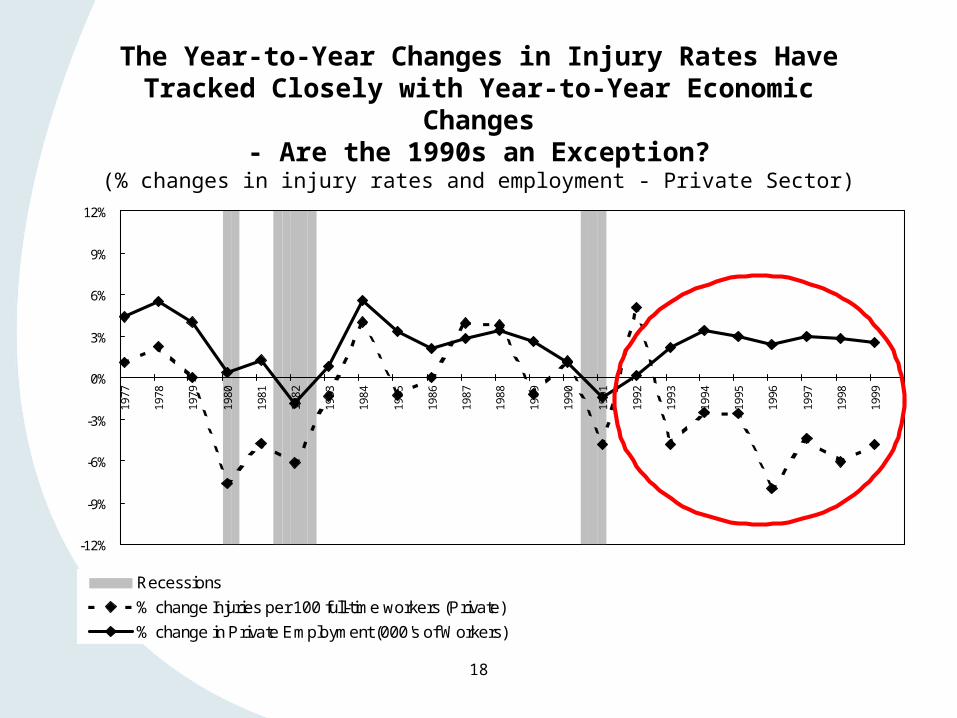

17 2002 NCCI Holdings, Inc.

Frequency Tracks with the Business Cycle

but

The Decline in the 1990s Seems to be Different

The Year-to-Year Changes in Injury Rates Have Tracked Closely with Year-to-Year Economic Changes

- Are the 1990s an Exception?(% changes in injury rates and employment - Private Sector)

-12%

-9%

-6%

-3%

0%

3%

6%

9%

12%

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

Recessions

% change Injuries per 100 full-time workers (Private)

% change in Private Employment (000's of Workers)

18

19 2002 NCCI Holdings, Inc.

Searching for the Factors Driving the Change in Frequencywith Special Interest in the Decline of the 1990s

The 1990s May Seem Different

but

Frequency Still Tracks with the Business Cycle

when

Combined with a Powerful (Linear) Downtrend

___________________________________________________

A Regression Analysis

20

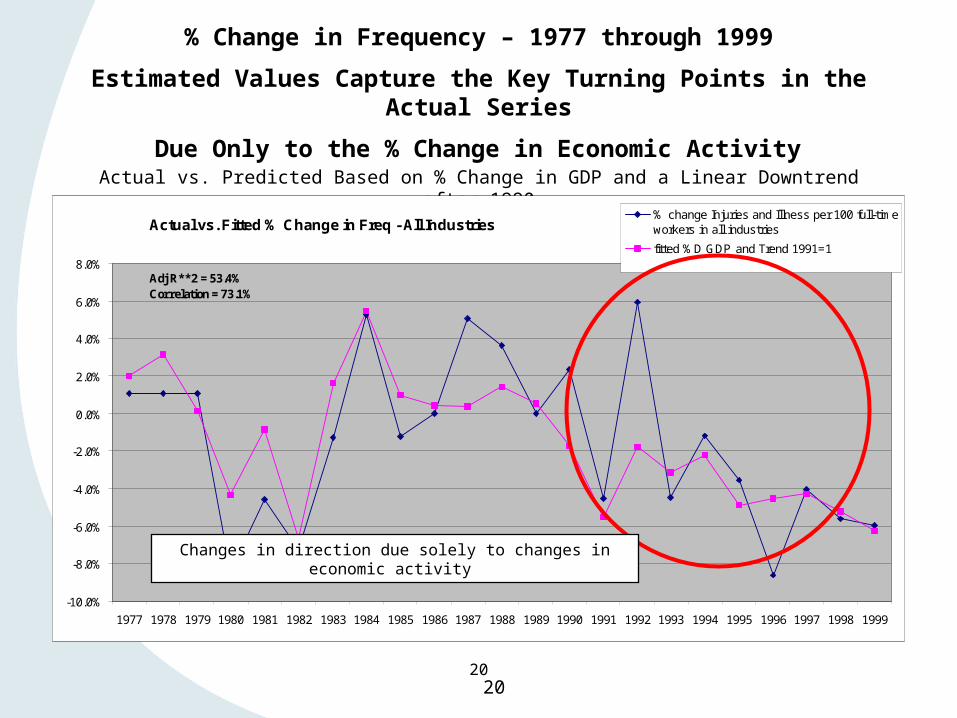

% Change in Frequency – 1977 through 1999

Estimated Values Capture the Key Turning Points in the Actual Series

Due Only to the % Change in Economic Activity

Actual vs. Predicted Based on % Change in GDP and a Linear Downtrend after 1990

Actual vs. Fitted % Change in Freq - All Industries

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

1977 1978 1979 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999

% change Injuries and Illness per 100 full-timeworkers in all industries

fitted %D GDP and Trend 1991=1

Adj R**2 = 53.4%Correlation = 73.1%

20

Changes in direction due solely to changes in economic activity

21 2002 NCCI Holdings, Inc.

Workers Comp Industry Concerns

• What Is the Source of this Downtrend?

• Will the Improvement Hold?

• Will the Decline Actually Reverse?

22 2002 NCCI Holdings, Inc.

Country Wide Experience in the 1990s

A Steady Decline

How Remarkable Is This?

23 2002 NCCI Holdings, Inc.

It’s Remarkable

and

It’s International

24 2002 NCCI Holdings, Inc.

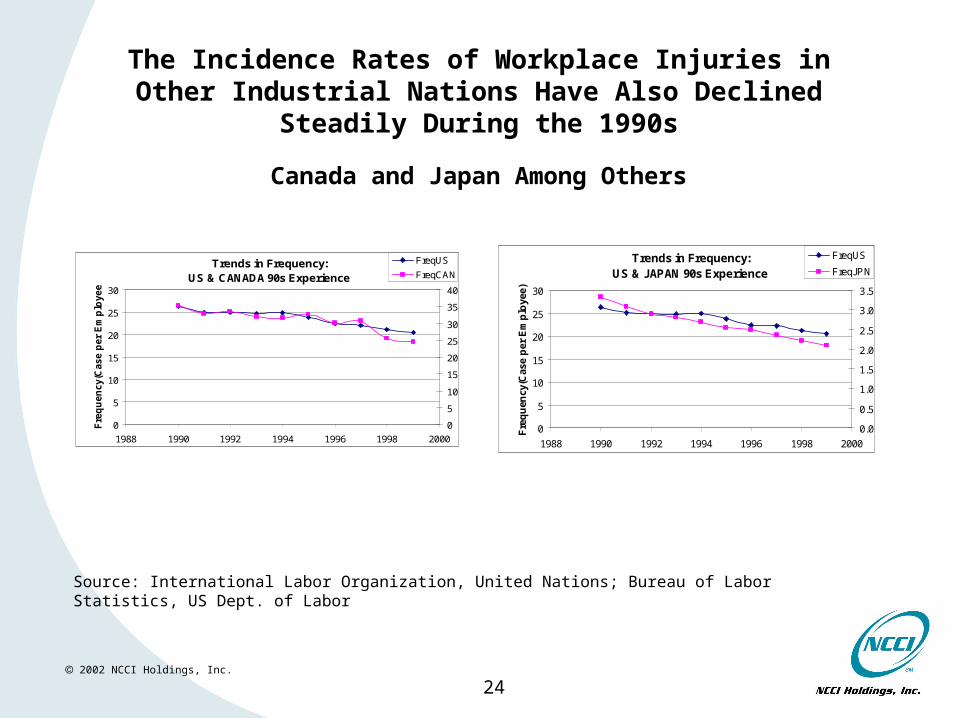

The Incidence Rates of Workplace Injuries in Other Industrial Nations Have Also Declined Steadily During the 1990s

Canada and Japan Among Others

Trends in Frequency: US & JAPAN 90s Experience

0

5

10

15

20

25

30

1988 1990 1992 1994 1996 1998 2000

Fre

qu

ency

(Cas

e p

er E

mp

loye

e)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

FreqUS

FreqJPNTrends in Frequency:

US & CANADA 90s Experience

0

5

10

15

20

25

30

1988 1990 1992 1994 1996 1998 2000

Fre

qu

en

cy(C

ase p

er

Em

plo

yee)

0

5

10

15

20

25

30

35

40

FreqUS

FreqCAN

Source: International Labor Organization, United Nations; Bureau of Labor Statistics, US Dept. of Labor

25 2002 NCCI Holdings, Inc.

Attention Shoppers

It’s Just Business

And

Wal-Mart Told Us Why

26 2002 NCCI Holdings, Inc.

Enhance Productivity to Compete

• McKinsey on Productivity Growth in the Last Half of the 1990s (NY Times 2/28/02)

• Competition and better management, not simply the spread of computers and the Internet, made the difference. Nowhere was that clearer than in retailing.

• Wal-Mart’s managerial innovations contributed mightily to the big increase in

America productivity in the late 1990s. • Most of the practices aren’t glamorous. • In some cases, not completely filling a pallet with goods can save so much time in

stocking the store that what seems “inefficient” at the warehouse is more productive overall.

• More in The McKinsey Quarterly (www.themckinseyquarterly.com)

27 2002 NCCI Holdings, Inc.

Wal-Mart’s Strategy

According to John Leyenberger, the divisional risk control director at Wal-Mart Stores:

• The decline in injuries is not due to just one thing.

• The Wal-Mart strategy is to minimize the number of times they handle the merchandise in order to increase both efficiency and safety.

28 2002 NCCI Holdings, Inc.

Why Wal-Mart Can Charge Low Prices

• Examples offered by Wal-Mart include:

• Inventory management - Analyzed peak sales days for tins of popcorn in the Christmas season. Then spoke with supplier to increase the number of deliveries from 2 to 4. They then didn't need to store and move tins of popcorn to make room for other merchandise. This saved over $1 million in labor costs, but also reduced their risk exposure.

• Inventory handling - Redesigned the back room and purchased new equipment called a walker stacker. This is a walk behind machine with a mast that allows employees to put merchandise up high out of the way without climbing a ladder. The redesign and new equipment also has allowed them to start unloading trucks at 4pm instead of 10pm, which reduces the rush. This was rolled out to 2600 stores over 18 months.

• Stocking shelves - Pulled out normal shelving for dog food and instead just drop in the pallet.

• Check out - Developed a new carousel/lazy Susan for bagging that reduces reaching and lifting. The bag to be loaded is on the carousel right next to the scanner. Once it is loaded, the cashier turns the lazy Susan toward the customer and starts filling a new bag that is then right next to the scanner. This reduces reaching since the bags are located next to the scanner, and it reduces lifting because 80% of the customers will pick up their own bags when they are turned toward them. It also improves cashier efficiency.

29 2002 NCCI Holdings, Inc.

Applying the Knowledge

Supporting Loss Cost Filings

30 2002 NCCI Holdings, Inc.

States Differ

One Size Doesn’t Fit All

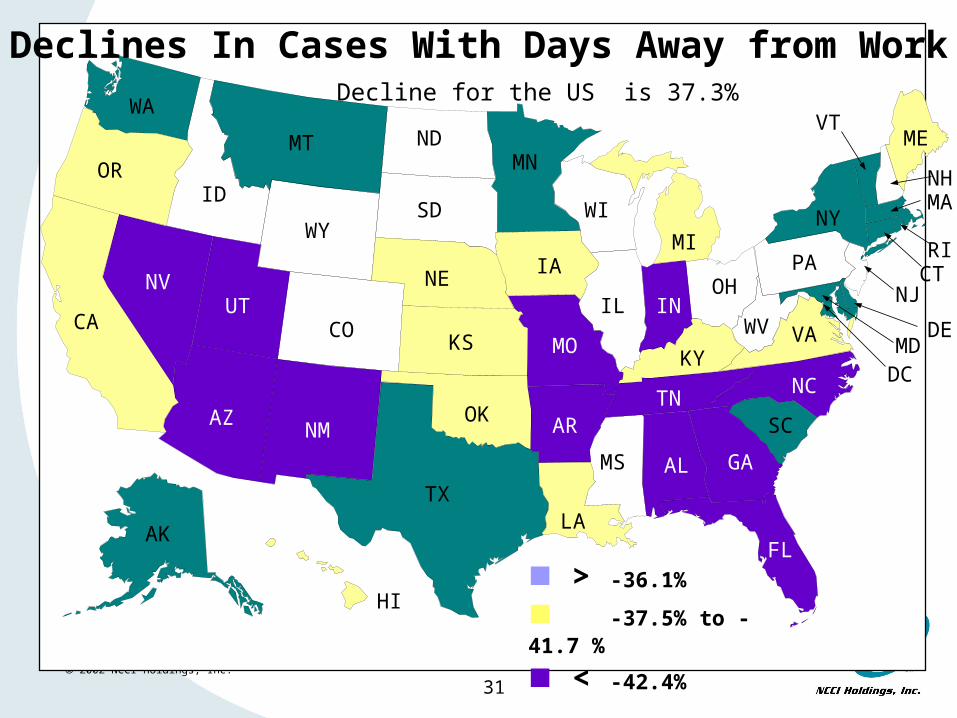

31 2002 NCCI Holdings, Inc.

Declines In Cases With Days Away from Work

> -36.1%

< -37.5% to -41.7 %

< -42.4%

Decline for the US is 37.3%

AK

OR

UT

WY

MT

SD

ND

KS

NE

OKNM

MO

AR

LA

MS

KY

TN

AL

FL

WI

INOH

PA

NY

ME

WV

NC

SC

GA

VAIL

MIIA

MN

TX

CO

AZ

ID

NV

CA

WA

NHMA

RICT

NJ

VT

HI

DE

DCMD

32 2002 NCCI Holdings, Inc.

Econometric Analysis of Loss Trends

Factors that Drive the Number of Claims

• Exposure - covered employment

• Long term changes in the nature of work

• Short term surges in employment - the business cycle

33 2002 NCCI Holdings, Inc.

How Well Does This Simple Model Do?

34 2002 NCCI Holdings, Inc.

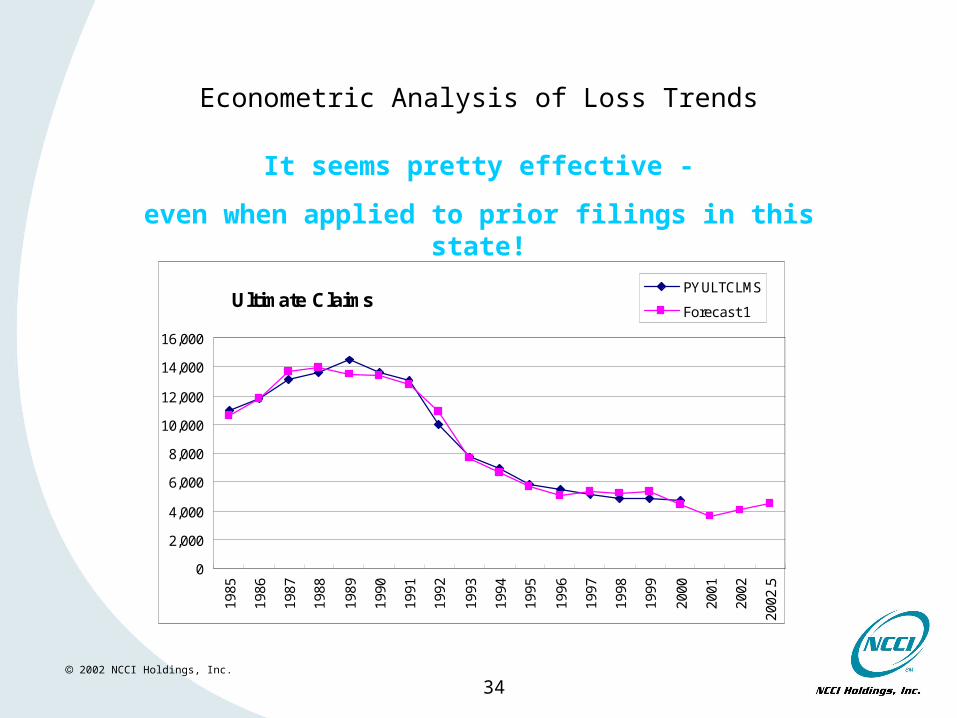

Econometric Analysis of Loss Trends

Ultimate Claims

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2002

.5

PYULTCLMS

Forecast 1

It seems pretty effective -

even when applied to prior filings in this state!

35 2002 NCCI Holdings, Inc.

Econometric Analysis of Loss Trends

Ultimate Claims

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

PYULTCLMS

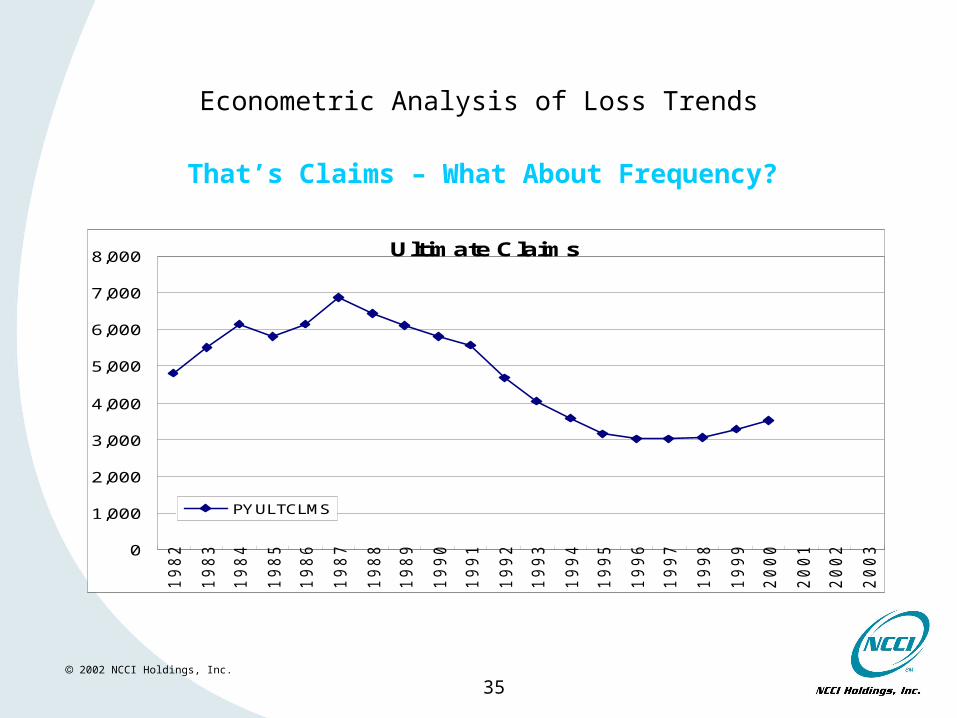

That’s Claims – What About Frequency?

36 2002 NCCI Holdings, Inc.

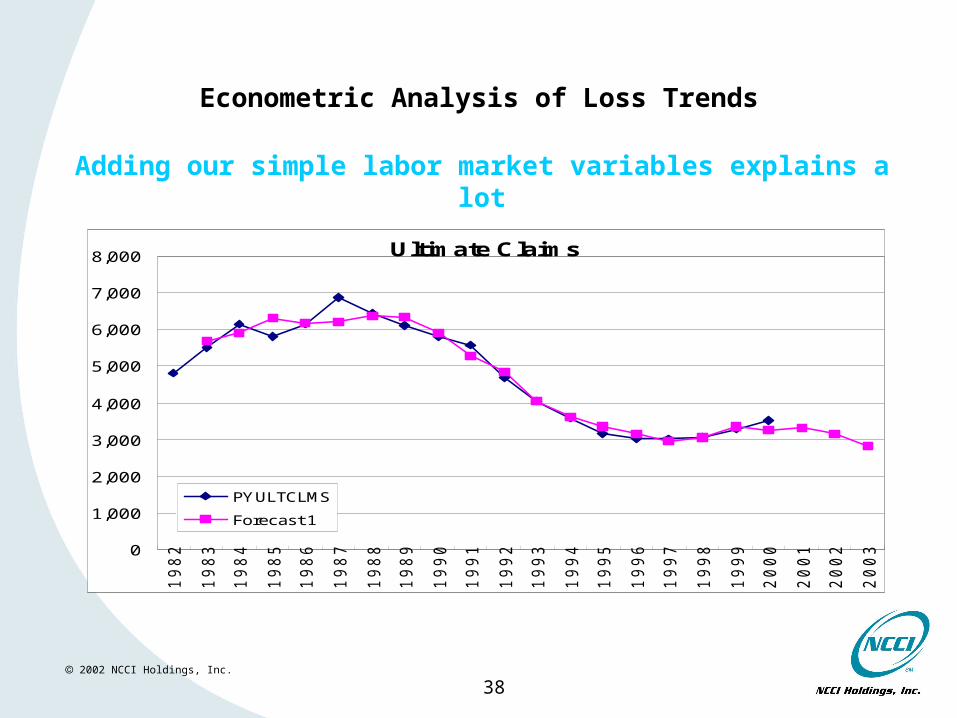

Econometric Analysis of Loss Trends

Ultimate Claims

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

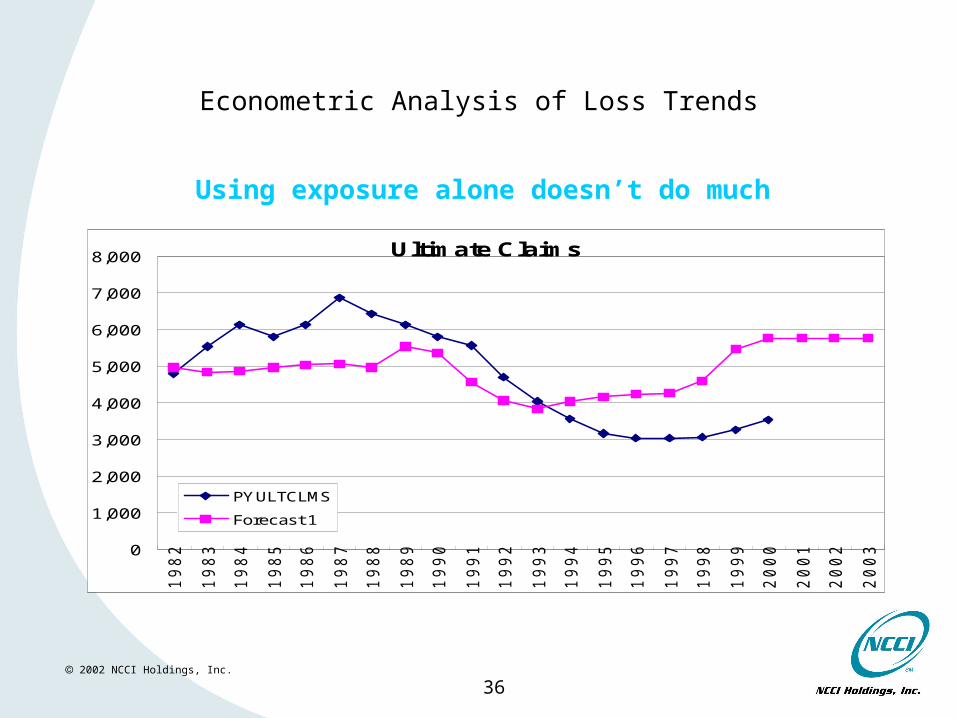

PYULTCLMS

Forecast 1

Using exposure alone doesn’t do much

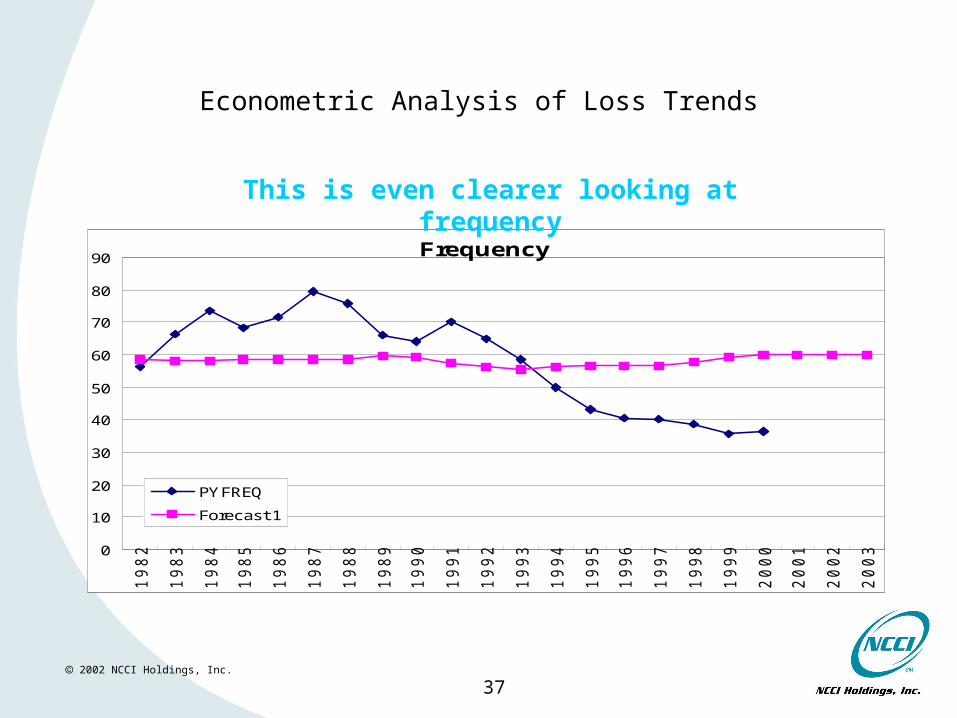

37 2002 NCCI Holdings, Inc.

Econometric Analysis of Loss Trends

Frequency

0

10

20

30

40

50

60

70

80

90

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

PYFREQ

Forecast 1

This is even clearer looking at frequency

38 2002 NCCI Holdings, Inc.

Econometric Analysis of Loss Trends

Ultimate Claims

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

PYULTCLMS

Forecast 1

Adding our simple labor market variables explains a lot

39 2002 NCCI Holdings, Inc.

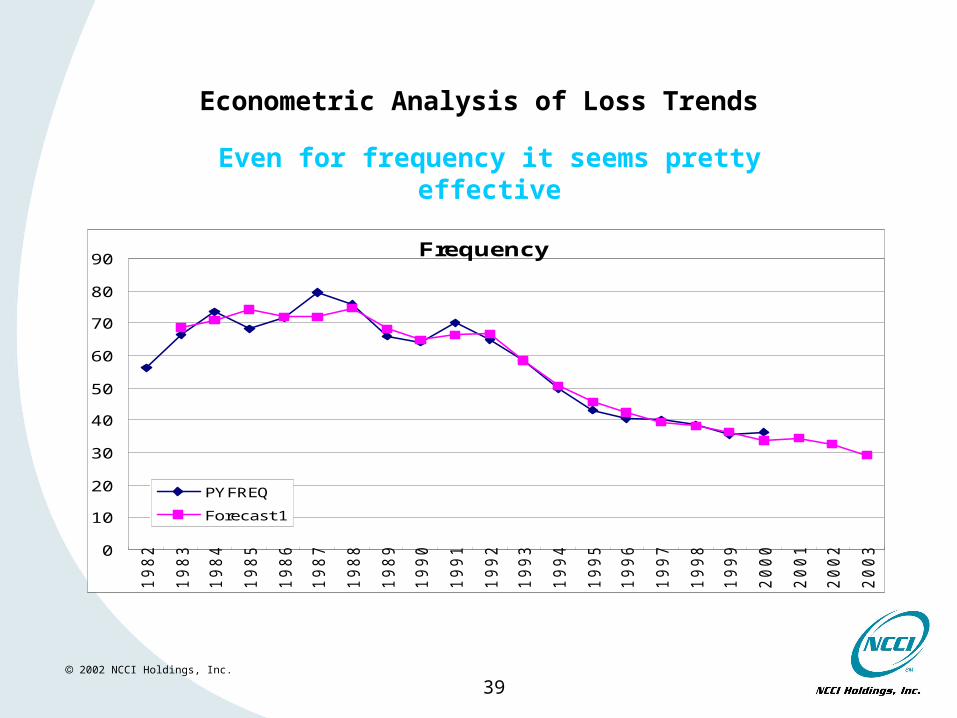

Econometric Analysis of Loss Trends

Frequency

0

10

20

30

40

50

60

70

80

90

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

PYFREQ

Forecast 1

Even for frequency it seems pretty effective

40 2002 NCCI Holdings, Inc.

Frequency Research at NCCI

• We believe that we have identified key drivers.

• This has helped in the analysis of loss cost trends.

• The research continues.

2002 NCCI Holdings, Inc.

Thank You for the Opportunity to Share This Information

Questions or Comments?