Embed Size (px)

Citation preview

Global Value Chain Reshoring: Overview and Impact on Trade

Jong Woo KangPrincipal Economist for Regional Cooperation and IntegrationEconomic Research and Regional Cooperation Department

Asian Development Bank

RCI-Policy Open Dialogue Webinar #22| 14 July 2021

Drivers of Supply Chain Reshoring

• Trade conflict between the United States (US) and the People’s Republic of China

(PRC) have encouraged policy makers, especially in the US, to consider reshoring

policies.

• Recent events such as the lockdowns due to the COVID-19 pandemic may cause

companies to consider reshoring their supply chains as well, although we have yet

to see the data in 2020.

2

Motivations of Reshoring

• Even before the pandemic, policy makers and businesses alike had revisited the rationale behind the

off-shoring strategy, driven mainly by cost and operational efficiency.

• (Middle-income countries) Technological progress has enabled many middle-income economies to

move up the technological ladder, and consequently to produce key intermediate goods themselves

instead of relying on foreign imports.

• (Advanced countries) The development of robotics and artificial intelligence also motivates advanced

economies to bring their production facilities closer to customers, tailoring their products to consumer

preferences.

• Concerns about the quality of products and services outsourced had also been on businesses’ minds. In

this sense, COVID-19 and the trade war have accentuated motivation for reshoring rather than

triggering it.

• After all, the reshoring trend will likely persist, although its exact form and size is difficult to predict from

the reflections on vulnerabilities of global supply chains, just-in-time inventory management systems,

and vast spillover effects of the crunch in certain segments of supply chains (e.g., recent shortages in

microchips and semiconductors).

3

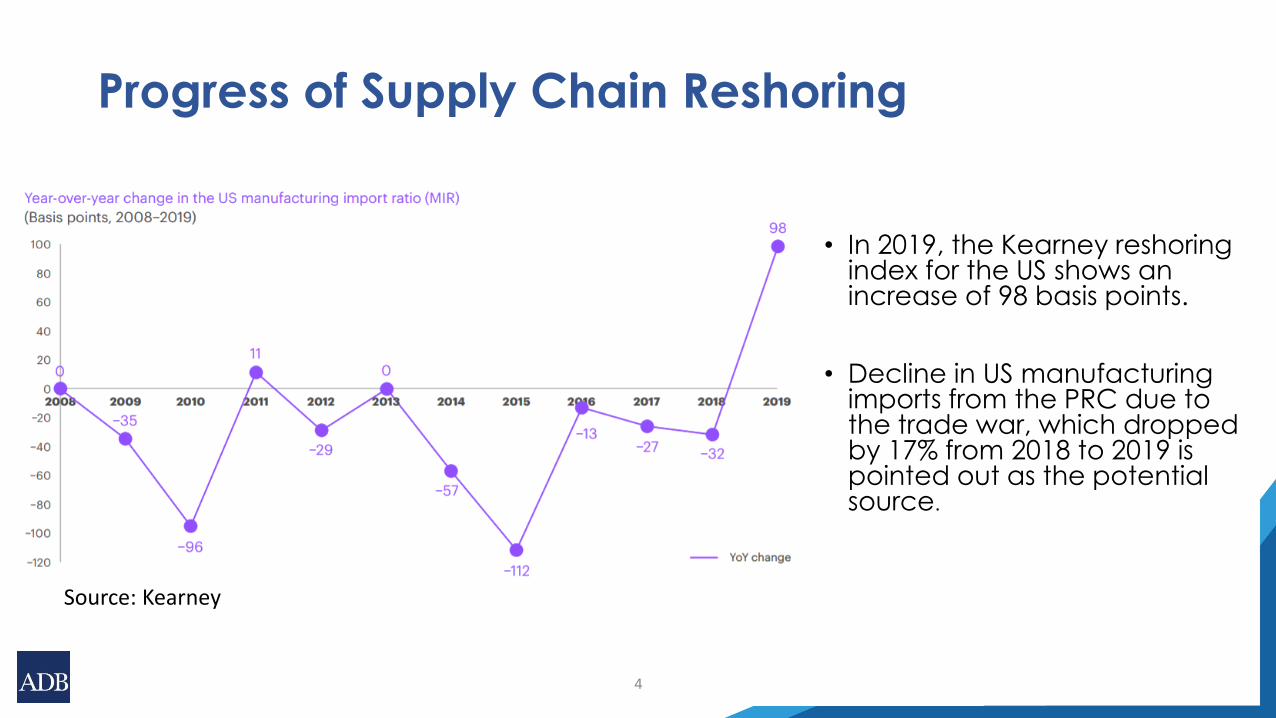

Progress of Supply Chain Reshoring

• In 2019, the Kearney reshoring index for the US shows an increase of 98 basis points.

• Decline in US manufacturing imports from the PRC due to the trade war, which dropped by 17% from 2018 to 2019 is pointed out as the potential source.

4

Source: Kearney

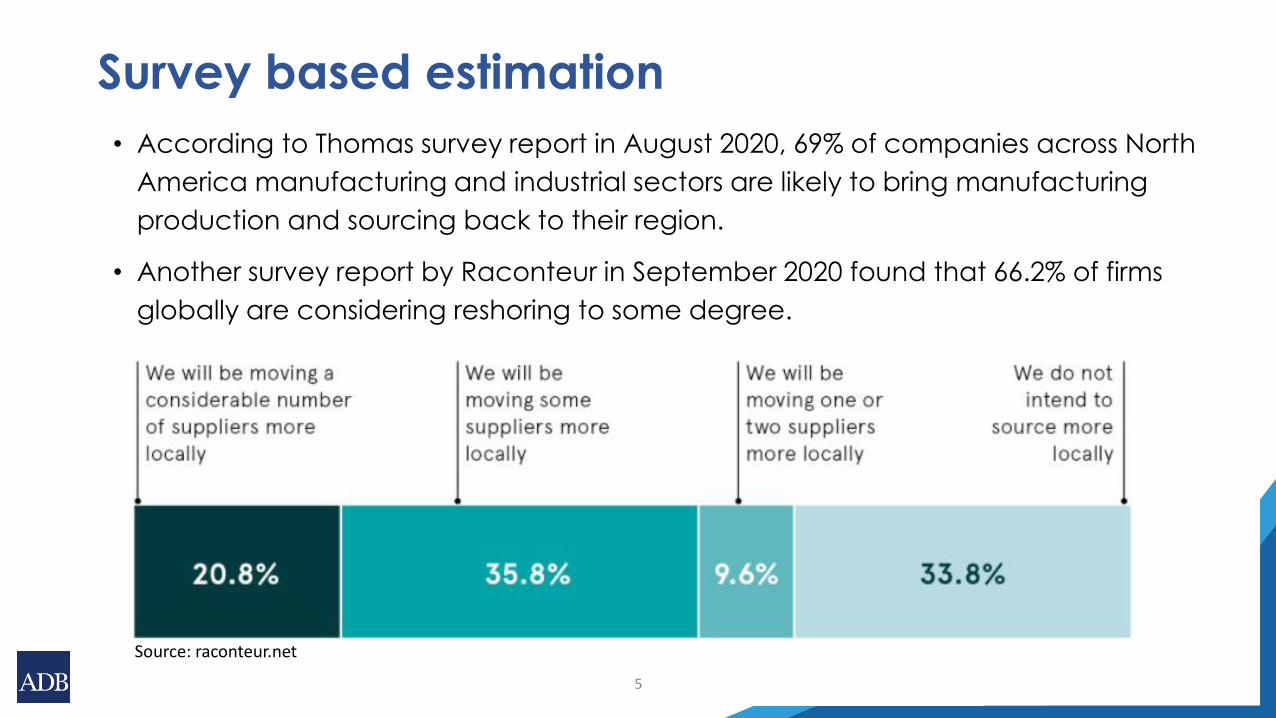

Survey based estimation

• According to Thomas survey report in August 2020, 69% of companies across North

America manufacturing and industrial sectors are likely to bring manufacturing

production and sourcing back to their region.

• Another survey report by Raconteur in September 2020 found that 66.2% of firms

globally are considering reshoring to some degree.

5

Source: raconteur.net

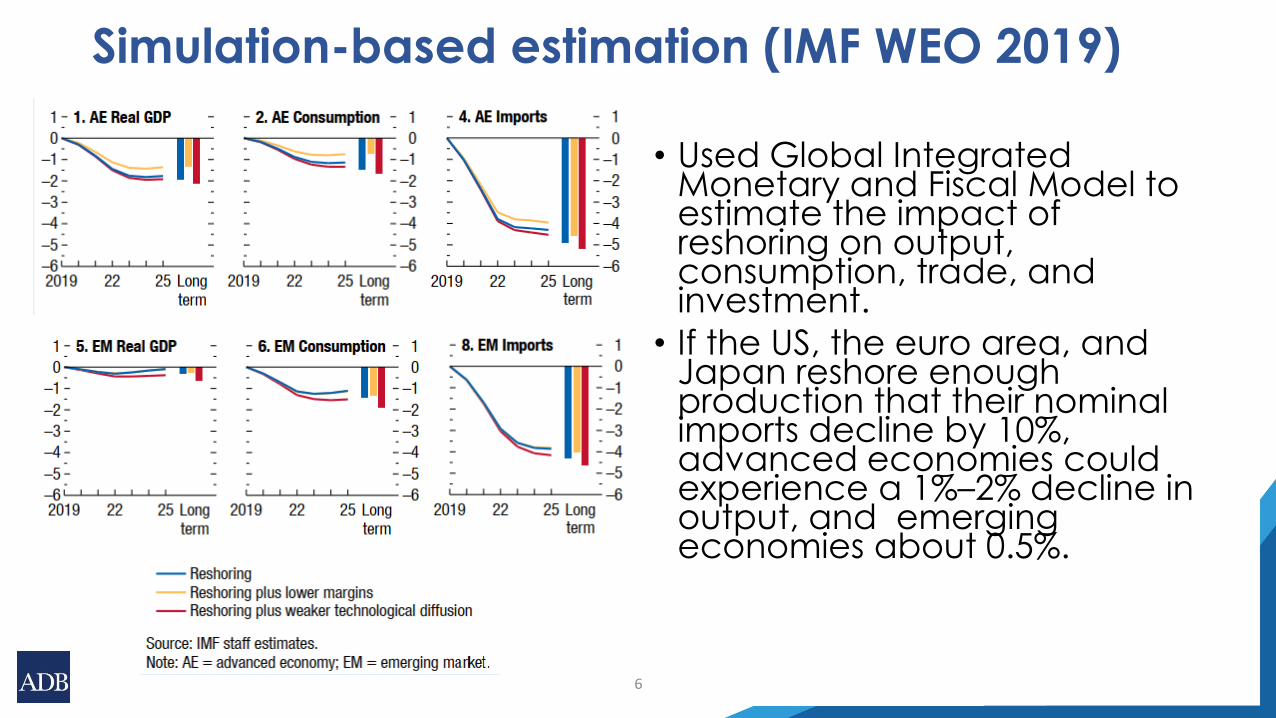

Simulation-based estimation (IMF WEO 2019)

• Used Global Integrated Monetary and Fiscal Model to estimate the impact of reshoring on output, consumption, trade, and investment.

• If the US, the euro area, and Japan reshore enough production that their nominal imports decline by 10%, advanced economies could experience a 1%–2% decline in output, and emerging economies about 0.5%.

6

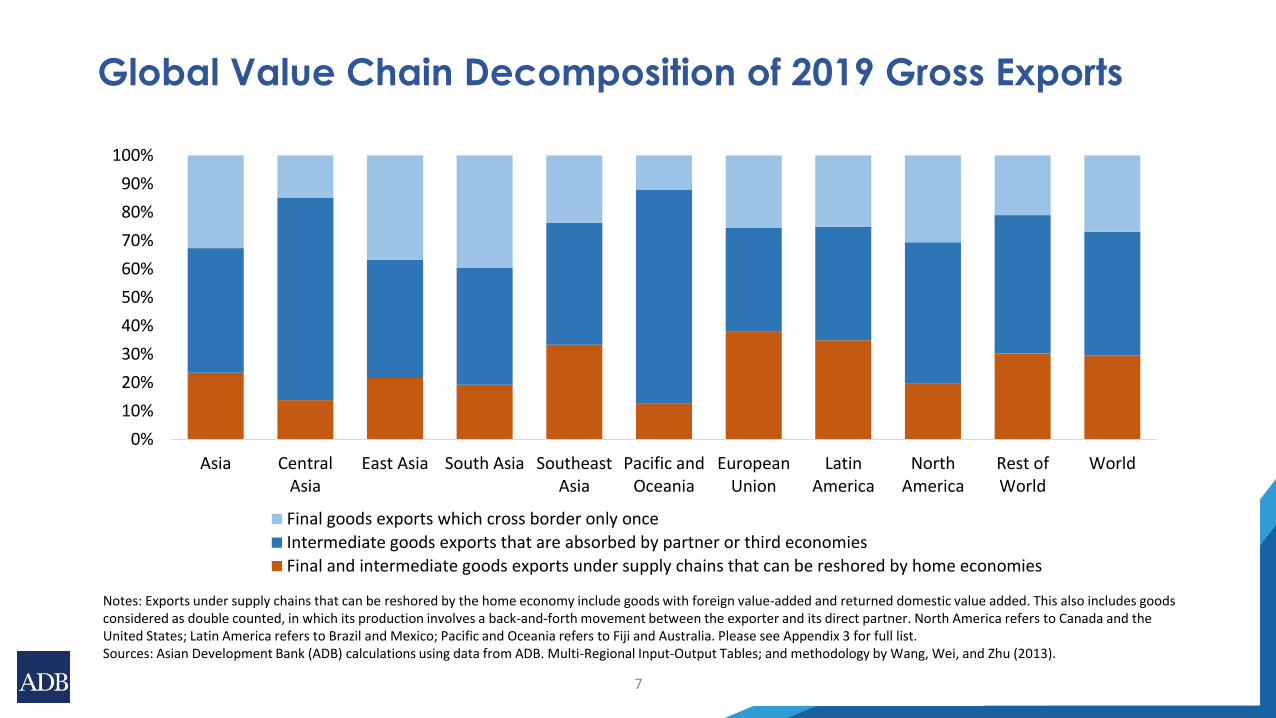

Global Value Chain Decomposition of 2019 Gross Exports

7

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Asia CentralAsia

East Asia South Asia SoutheastAsia

Pacific andOceania

EuropeanUnion

LatinAmerica

NorthAmerica

Rest ofWorld

World

Final goods exports which cross border only once

Intermediate goods exports that are absorbed by partner or third economies

Final and intermediate goods exports under supply chains that can be reshored by home economies

Notes: Exports under supply chains that can be reshored by the home economy include goods with foreign value-added and returned domestic value added. This also includes goods considered as double counted, in which its production involves a back-and-forth movement between the exporter and its direct partner. North America refers to Canada and the United States; Latin America refers to Brazil and Mexico; Pacific and Oceania refers to Fiji and Australia. Please see Appendix 3 for full list.Sources: Asian Development Bank (ADB) calculations using data from ADB. Multi-Regional Input-Output Tables; and methodology by Wang, Wei, and Zhu (2013).

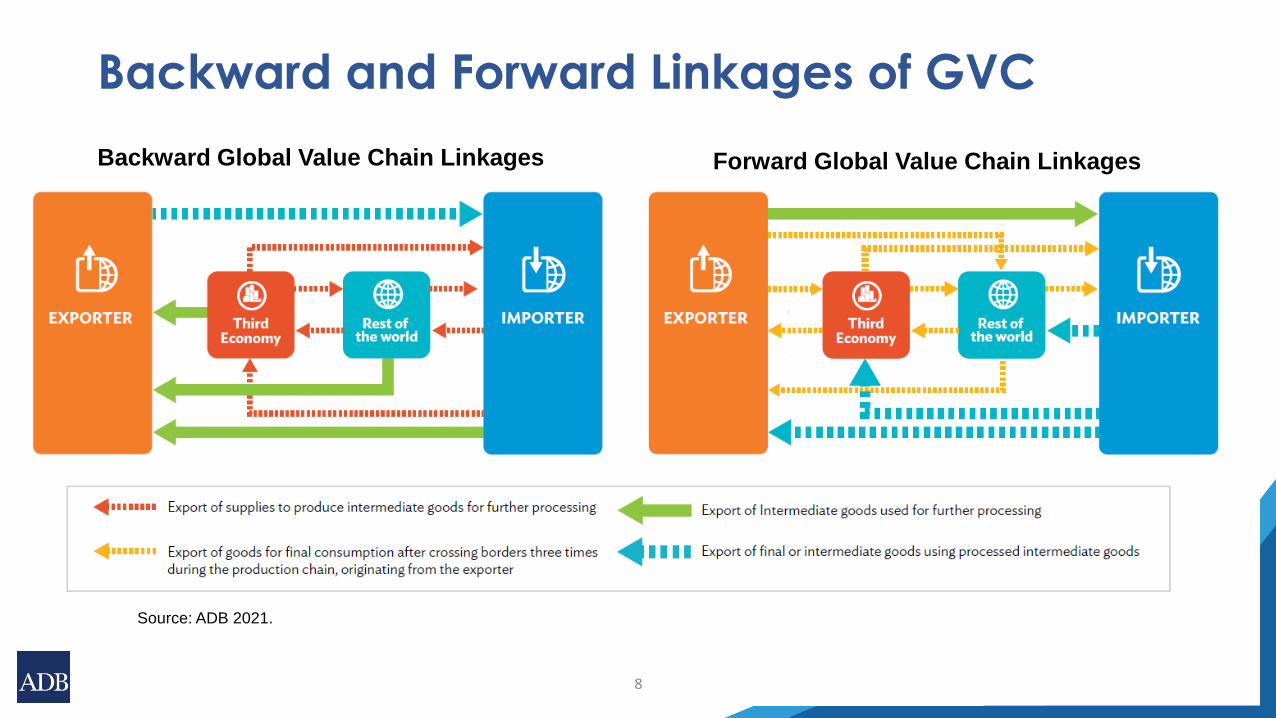

Backward and Forward Linkages of GVC

8

Backward Global Value Chain Linkages Forward Global Value Chain Linkages

Source: ADB 2021.

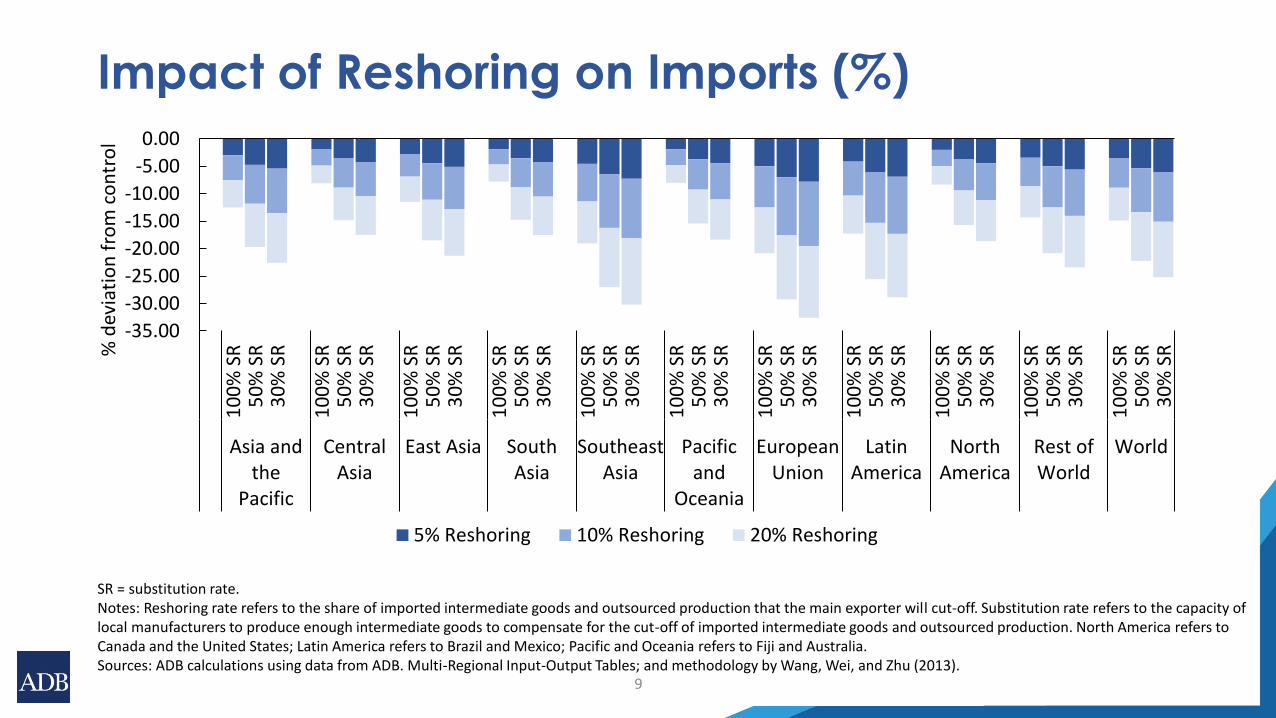

Impact of Reshoring on Imports (%)

9

-35.00

-30.00

-25.00

-20.00

-15.00

-10.00

-5.00

0.00

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

Asia andthe

Pacific

CentralAsia

East Asia SouthAsia

SoutheastAsia

Pacificand

Oceania

EuropeanUnion

LatinAmerica

NorthAmerica

Rest ofWorld

World

% d

evia

tio

n f

rom

co

ntr

ol

5% Reshoring 10% Reshoring 20% Reshoring

SR = substitution rate.Notes: Reshoring rate refers to the share of imported intermediate goods and outsourced production that the main exporter will cut-off. Substitution rate refers to the capacity of local manufacturers to produce enough intermediate goods to compensate for the cut-off of imported intermediate goods and outsourced production. North America refers to Canada and the United States; Latin America refers to Brazil and Mexico; Pacific and Oceania refers to Fiji and Australia.Sources: ADB calculations using data from ADB. Multi-Regional Input-Output Tables; and methodology by Wang, Wei, and Zhu (2013).

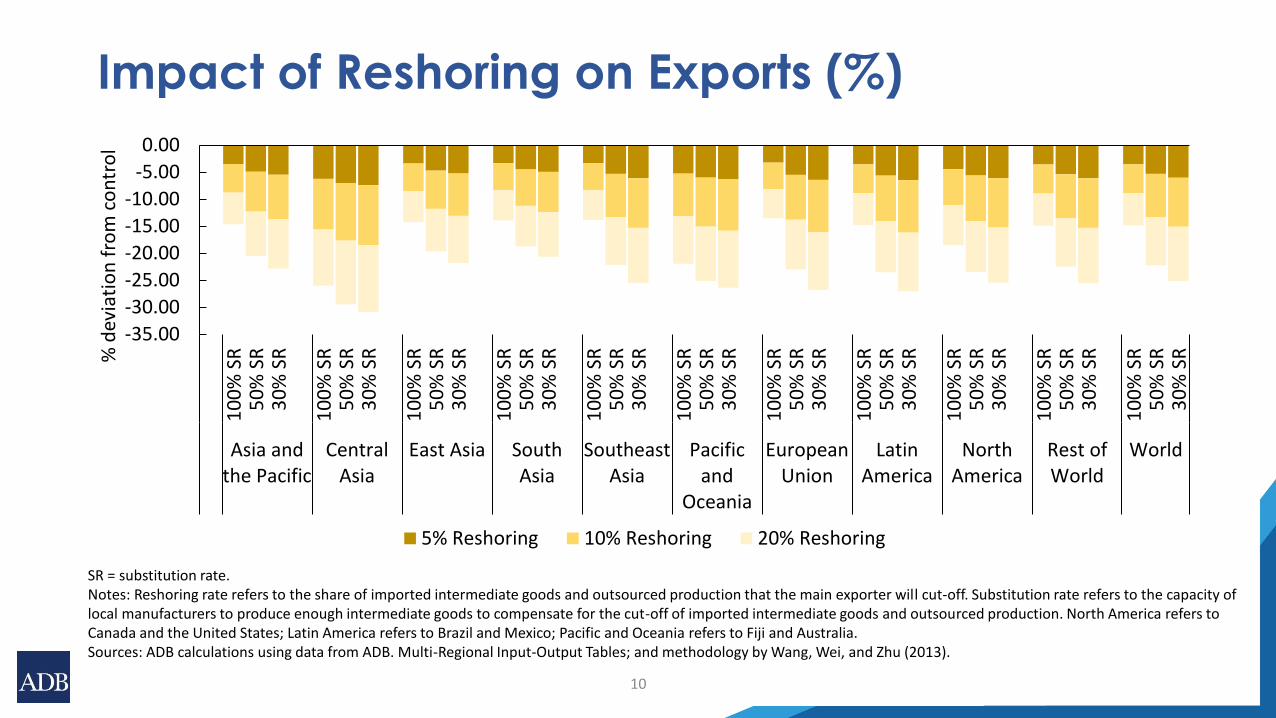

Impact of Reshoring on Exports (%)

10

-35.00

-30.00

-25.00

-20.00

-15.00

-10.00

-5.00

0.00

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

Asia andthe Pacific

CentralAsia

East Asia SouthAsia

SoutheastAsia

Pacificand

Oceania

EuropeanUnion

LatinAmerica

NorthAmerica

Rest ofWorld

World

% d

evia

tio

n f

rom

co

ntr

ol

5% Reshoring 10% Reshoring 20% Reshoring

SR = substitution rate.Notes: Reshoring rate refers to the share of imported intermediate goods and outsourced production that the main exporter will cut-off. Substitution rate refers to the capacity of local manufacturers to produce enough intermediate goods to compensate for the cut-off of imported intermediate goods and outsourced production. North America refers to Canada and the United States; Latin America refers to Brazil and Mexico; Pacific and Oceania refers to Fiji and Australia.Sources: ADB calculations using data from ADB. Multi-Regional Input-Output Tables; and methodology by Wang, Wei, and Zhu (2013).

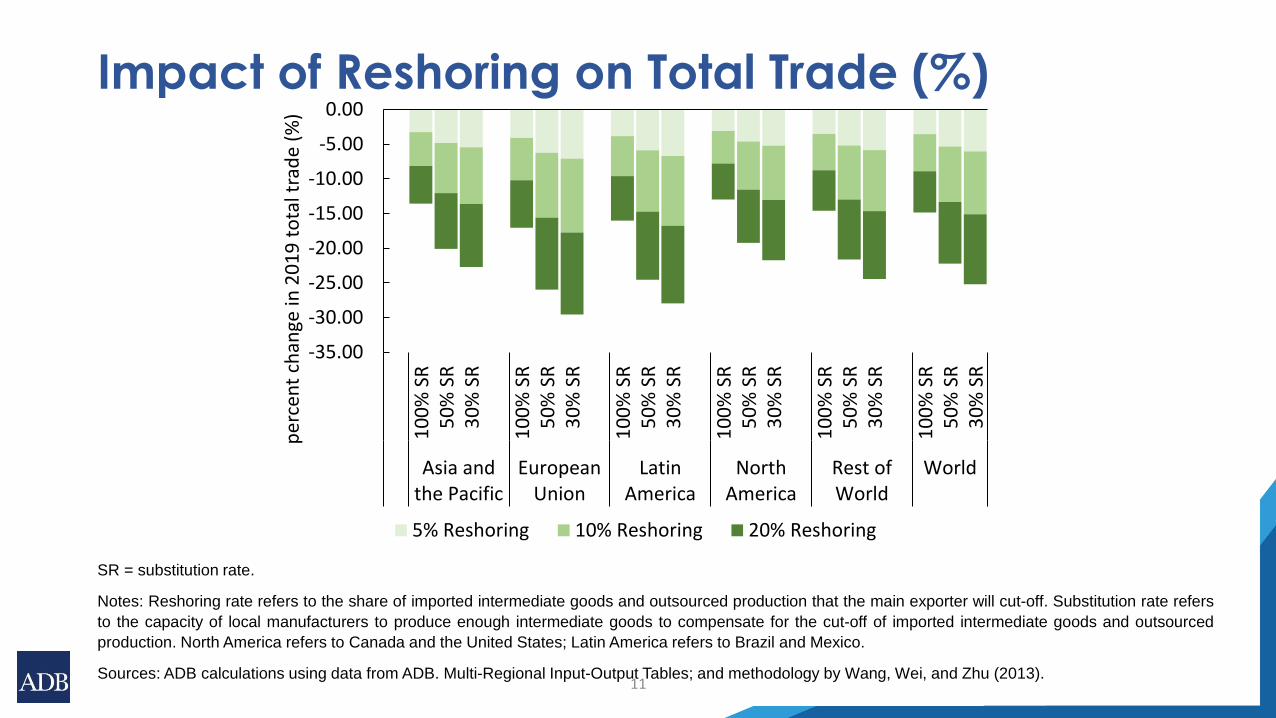

Impact of Reshoring on Total Trade (%)

11

SR = substitution rate.

Notes: Reshoring rate refers to the share of imported intermediate goods and outsourced production that the main exporter will cut-off. Substitution rate refers

to the capacity of local manufacturers to produce enough intermediate goods to compensate for the cut-off of imported intermediate goods and outsourced

production. North America refers to Canada and the United States; Latin America refers to Brazil and Mexico.

Sources: ADB calculations using data from ADB. Multi-Regional Input-Output Tables; and methodology by Wang, Wei, and Zhu (2013).

-35.00

-30.00

-25.00

-20.00

-15.00

-10.00

-5.00

0.00

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

Asia andthe Pacific

EuropeanUnion

LatinAmerica

NorthAmerica

Rest ofWorld

World

per

cen

t ch

ange

in 2

01

9 t

ota

l tra

de

(%)

5% Reshoring 10% Reshoring 20% Reshoring

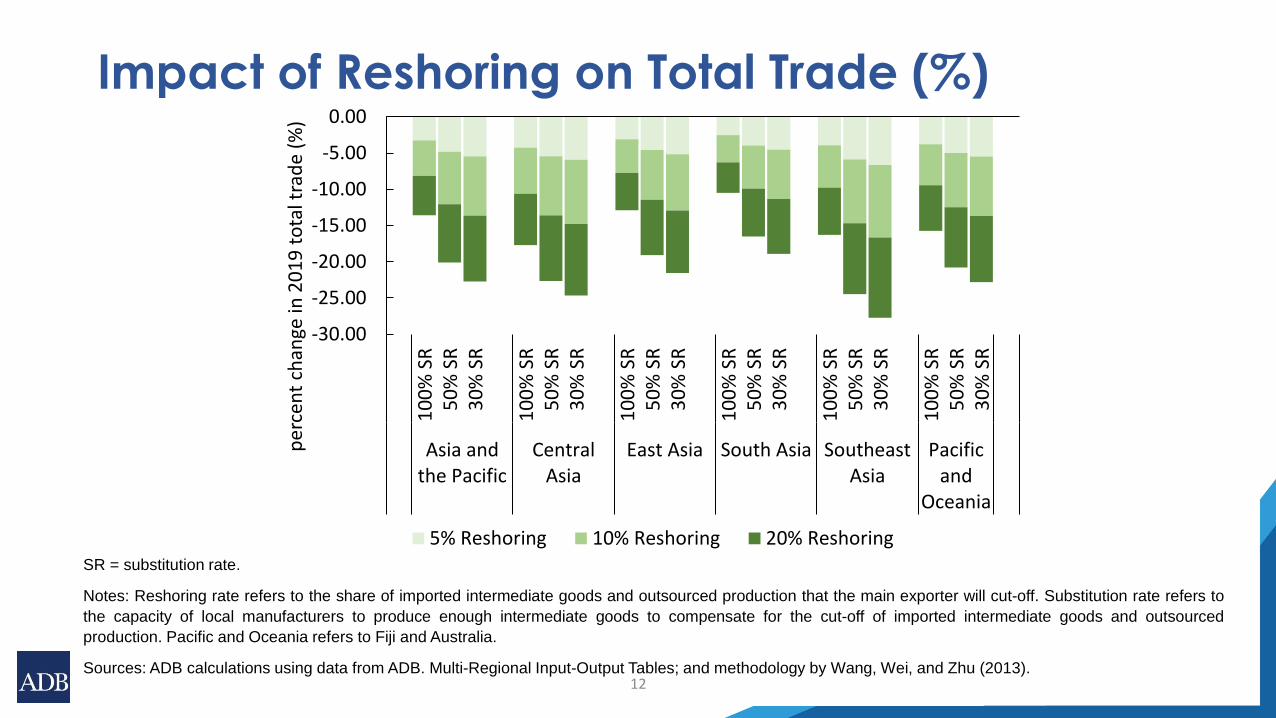

Impact of Reshoring on Total Trade (%)

12

SR = substitution rate.

Notes: Reshoring rate refers to the share of imported intermediate goods and outsourced production that the main exporter will cut-off. Substitution rate refers to

the capacity of local manufacturers to produce enough intermediate goods to compensate for the cut-off of imported intermediate goods and outsourced

production. Pacific and Oceania refers to Fiji and Australia.

Sources: ADB calculations using data from ADB. Multi-Regional Input-Output Tables; and methodology by Wang, Wei, and Zhu (2013).

-30.00

-25.00

-20.00

-15.00

-10.00

-5.00

0.00

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

10

0%

SR

50

% S

R3

0%

SR

Asia andthe Pacific

CentralAsia

East Asia South Asia SoutheastAsia

Pacificand

Oceania

per

cen

t ch

ange

in 2

01

9 t

ota

l tra

de

(%)

5% Reshoring 10% Reshoring 20% Reshoring

30

35

40

45

50

55

60

65

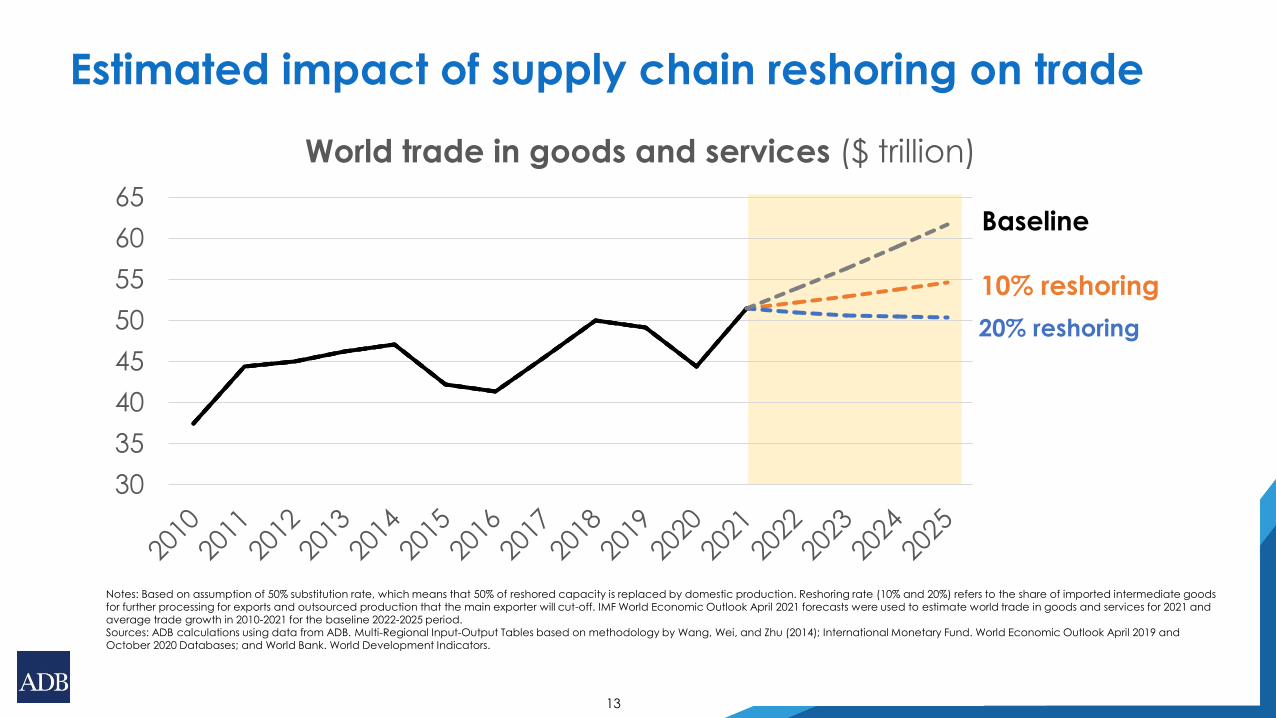

World trade in goods and services ($ trillion)

Baseline

10% reshoring

20% reshoring

Estimated impact of supply chain reshoring on trade

Notes: Based on assumption of 50% substitution rate, which means that 50% of reshored capacity is replaced by domestic production. Reshoring rate (10% and 20%) refers to the share of imported intermediate goods for further processing for exports and outsourced production that the main exporter will cut-off. IMF World Economic Outlook April 2021 forecasts were used to estimate world trade in goods and services for 2021 and average trade growth in 2010-2021 for the baseline 2022-2025 period.Sources: ADB calculations using data from ADB. Multi-Regional Input-Output Tables based on methodology by Wang, Wei, and Zhu (2014); International Monetary Fund. World Economic Outlook April 2019 and October 2020 Databases; and World Bank. World Development Indicators.

13

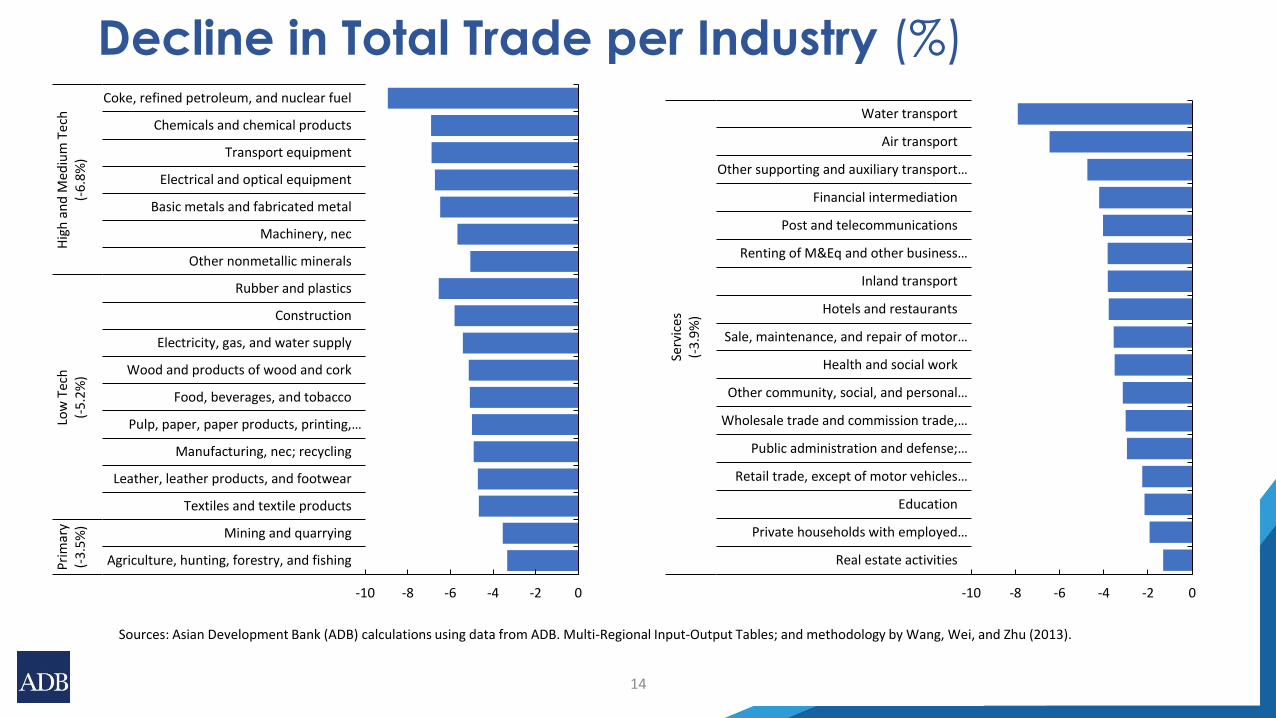

Decline in Total Trade per Industry (%)

14

Sources: Asian Development Bank (ADB) calculations using data from ADB. Multi-Regional Input-Output Tables; and methodology by Wang, Wei, and Zhu (2013).

-10 -8 -6 -4 -2 0

Agriculture, hunting, forestry, and fishing

Mining and quarrying

Textiles and textile products

Leather, leather products, and footwear

Manufacturing, nec; recycling

Pulp, paper, paper products, printing,…

Food, beverages, and tobacco

Wood and products of wood and cork

Electricity, gas, and water supply

Construction

Rubber and plastics

Other nonmetallic minerals

Machinery, nec

Basic metals and fabricated metal

Electrical and optical equipment

Transport equipment

Chemicals and chemical products

Coke, refined petroleum, and nuclear fuel

Pri

mar

y(-

3.5

%)

Low

Tec

h(-

5.2

%)

Hig

h a

nd

Med

ium

Te

ch(-

6.8

%)

-10 -8 -6 -4 -2 0

Real estate activities

Private households with employed…

Education

Retail trade, except of motor vehicles…

Public administration and defense;…

Wholesale trade and commission trade,…

Other community, social, and personal…

Health and social work

Sale, maintenance, and repair of motor…

Hotels and restaurants

Inland transport

Renting of M&Eq and other business…

Post and telecommunications

Financial intermediation

Other supporting and auxiliary transport…

Air transport

Water transport

Serv

ices

(-3

.9%

)

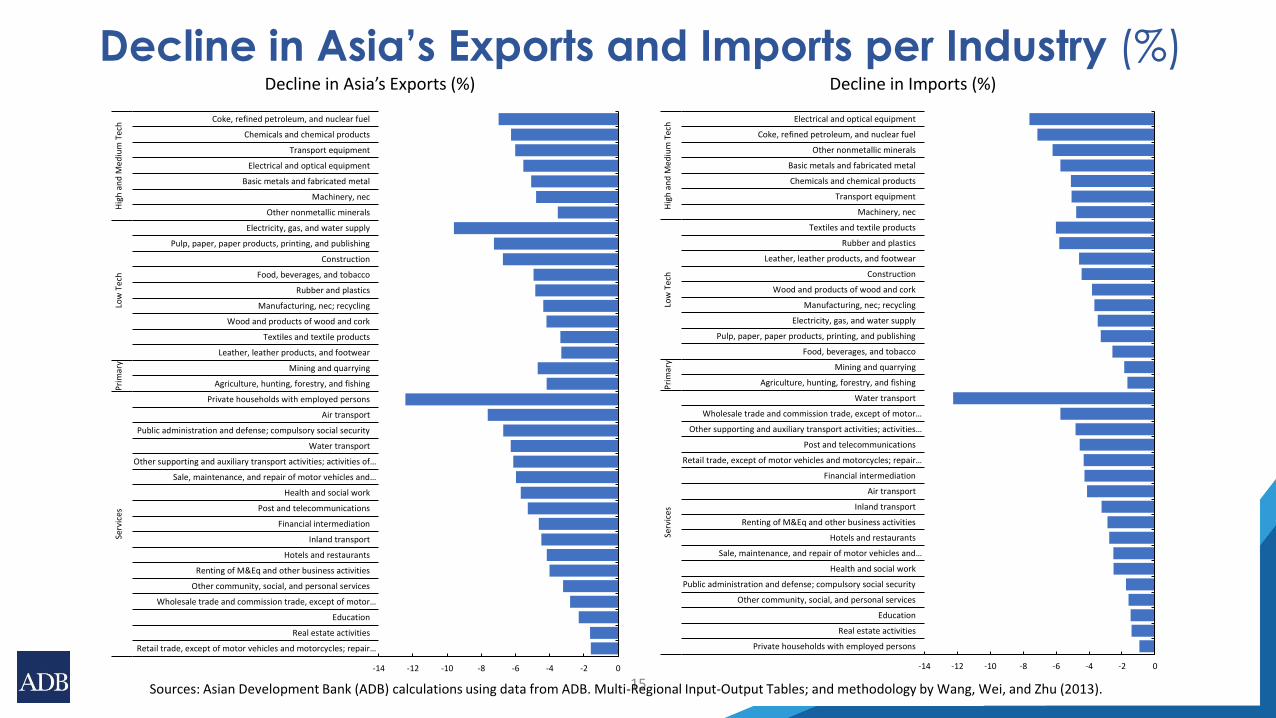

Decline in Asia’s Exports and Imports per Industry (%)

15Sources: Asian Development Bank (ADB) calculations using data from ADB. Multi-Regional Input-Output Tables; and methodology by Wang, Wei, and Zhu (2013).

-14 -12 -10 -8 -6 -4 -2 0

Private households with employed persons

Real estate activities

Education

Other community, social, and personal services

Public administration and defense; compulsory social security

Health and social work

Sale, maintenance, and repair of motor vehicles and…

Hotels and restaurants

Renting of M&Eq and other business activities

Inland transport

Air transport

Financial intermediation

Retail trade, except of motor vehicles and motorcycles; repair…

Post and telecommunications

Other supporting and auxiliary transport activities; activities…

Wholesale trade and commission trade, except of motor…

Water transport

Agriculture, hunting, forestry, and fishing

Mining and quarrying

Food, beverages, and tobacco

Pulp, paper, paper products, printing, and publishing

Electricity, gas, and water supply

Manufacturing, nec; recycling

Wood and products of wood and cork

Construction

Leather, leather products, and footwear

Rubber and plastics

Textiles and textile products

Machinery, nec

Transport equipment

Chemicals and chemical products

Basic metals and fabricated metal

Other nonmetallic minerals

Coke, refined petroleum, and nuclear fuel

Electrical and optical equipment

Serv

ices

Pri

mar

yLo

w T

ech

Hig

h a

nd

Med

ium

Tec

h

Decline in Imports (%)

-14 -12 -10 -8 -6 -4 -2 0

Retail trade, except of motor vehicles and motorcycles; repair…

Real estate activities

Education

Wholesale trade and commission trade, except of motor…

Other community, social, and personal services

Renting of M&Eq and other business activities

Hotels and restaurants

Inland transport

Financial intermediation

Post and telecommunications

Health and social work

Sale, maintenance, and repair of motor vehicles and…

Other supporting and auxiliary transport activities; activities of…

Water transport

Public administration and defense; compulsory social security

Air transport

Private households with employed persons

Agriculture, hunting, forestry, and fishing

Mining and quarrying

Leather, leather products, and footwear

Textiles and textile products

Wood and products of wood and cork

Manufacturing, nec; recycling

Rubber and plastics

Food, beverages, and tobacco

Construction

Pulp, paper, paper products, printing, and publishing

Electricity, gas, and water supply

Other nonmetallic minerals

Machinery, nec

Basic metals and fabricated metal

Electrical and optical equipment

Transport equipment

Chemicals and chemical products

Coke, refined petroleum, and nuclear fuelSe

rvic

esP

rim

ary

Low

Tec

hH

igh

an

d M

ediu

m T

ech

Decline in Asia’s Exports (%)

Conclusion

• Recent events, including trade conflicts and COVID-19 lockdowns, have prompted

policy makers and businesses to consider reshoring of supply chains to mitigate the

adverse effects of these trade shocks.

• Using the ADB’s MRIO Tables to simulate the direct and spillover effects of reshoring,

estimates suggest that reshoring by 5%–10% can lead to a 5.3% to 13.3% decrease in

global trade from its base value.

• Impact will be heterogeneous across sectors and regions depending upon the depth

of supply chain linkages.

16

Thank you!

ERCD/ERCI team

17