Embed Size (px)

Citation preview

Selling Your Business For It’s Maximum Value

A Presentation by Paul McKay and Dave Wilson

Selling Your Business for Maximum Value

© Booth Ainsworth and SAS Daniels LLP

Minimise Your Tax Bill

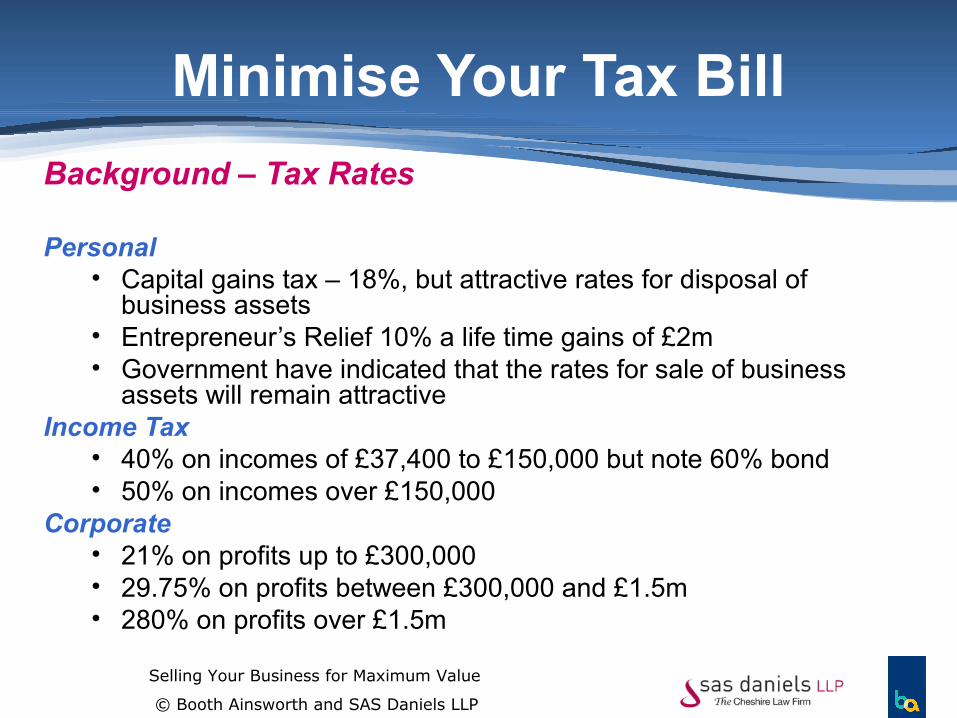

Background – Tax Rates

Personal• Capital gains tax – 18%, but attractive rates for disposal of

business assets• Entrepreneur’s Relief 10% a life time gains of £2m• Government have indicated that the rates for sale of business

assets will remain attractiveIncome Tax

• 40% on incomes of £37,400 to £150,000 but note 60% bond• 50% on incomes over £150,000

Corporate• 21% on profits up to £300,000• 29.75% on profits between £300,000 and £1.5m• 280% on profits over £1.5m

Selling Your Business for Maximum Value

© Booth Ainsworth and SAS Daniels LLP

Minimise Your Tax Bill…contd

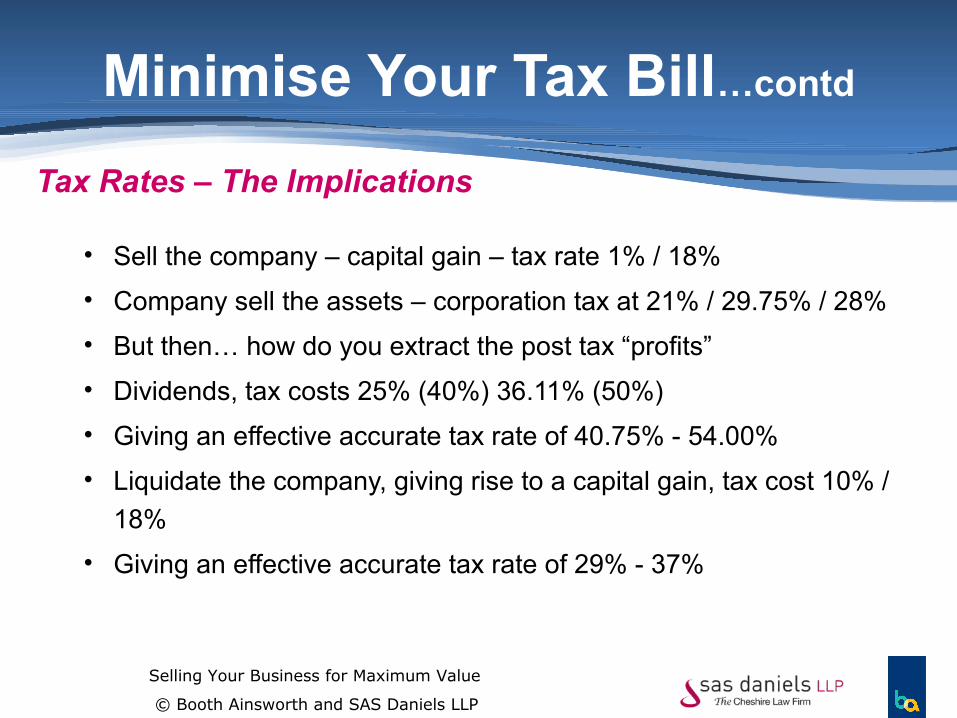

Tax Rates – The Implications

• Sell the company – capital gain – tax rate 1% / 18%

• Company sell the assets – corporation tax at 21% / 29.75% / 28%

• But then… how do you extract the post tax “profits”

• Dividends, tax costs 25% (40%) 36.11% (50%)

• Giving an effective accurate tax rate of 40.75% - 54.00%

• Liquidate the company, giving rise to a capital gain, tax cost 10% /

18%

• Giving an effective accurate tax rate of 29% - 37%

Selling Your Business for Maximum Value

© Booth Ainsworth and SAS Daniels LLP

Minimise Your Tax Bill…contd

Sell The Company / Sell The Trade And Assets

• Tension between the need of the purchaser /

vendor• Typically purchaser will want to buy the assets

- Enhanced capital allowances- Tax relief for acquired goodwill- No history

• Vendor will want to sell the company• Result; a “horse trade” but need to understand

the issues

Selling Your Business for Maximum Value

© Booth Ainsworth and SAS Daniels LLP

Minimise Your Tax Bill…contd

• If a fixed part of the consideration is deferred the final amount is taxed (capital gains) in the year the contract is finalised

• Same rule applies if the consideration is conditional upon a specific event

• Cash flow issues

• Computation only adjusted if part of the consideration becomes irrecoverable

Deferred Consideration (Share Sale)

Selling Your Business for Maximum Value

© Booth Ainsworth and SAS Daniels LLP

Minimise Your Tax Bill…contd

Earn Outs• Typical structure

- Fixed sum on completion- Further sum based on a formula e.g. share of profits for next three

years- Continues as an employee for next three years

• Tax treatment of the earn out element- Unquantifiable further sum regarded as a chore in action

- Value of the choice in action treated as part of the consideration for the share

- Gain qualifies for Entrepreneur's Relief

- Further gain when receive referred consideration

- But no Entrepreneur’s Relief

- Care needs to be taken to avoid characterising the referred element as some form of bonus, since HMRC may sell to tax as employment income

Selling Your Business for Maximum Value

© Booth Ainsworth and SAS Daniels LLP

Minimise Your Tax Bill…contd Consideration In Shares

• Share for share rules means that the capital gain on the disposal can usually be deferred

• New shares treated as being acquired at the same time, and same amount as the old shares

• Election can be made to opt out of the share exchange rates

• This means that the benefit of Entrepreneur's Relief can be ‘booked”

• When part case, part shares, consideration pro-rated

• But consider the cash flow issue

Selling Your Business for Maximum Value

© Booth Ainsworth and SAS Daniels LLP

Minimise Your Tax Bill…contd

Due Diligence

• Will look at the campaign tax affairs;- Corporation Tax

- VAT

- PAYE/NIC

for the last 6 years

• Benefit of “good housekeeping”

• Warranties of identities(?)

![SELLING WITH MAXIMUM VALUES: STRATEGIES THAT MAXIMIZE THE VALUE AND POWER OF YOUR SALES TO DRIVE FAST AND FAVORABLE PURCHASE DECISIONS [INBOUND 2014]](https://img.pdfslide.net/doc/110x75/559419f61a28abe92b8b4579/selling-with-maximum-values-strategies-that-maximize-the-value-and-power-of-your-sales-to-drive-fast-and-favorable-purchase-decisions-inbound-2014.jpg)