Embed Size (px)

Citation preview

FORE SCHOOL OF MANAGEMENT

Studying theRetail Strategy ofApparel IndustrySubmitted to Prof. Asif Zameer

SUBMITTED BY GROUP 6

INTRODUCTION

Broadly, the domestic apparel industry constitutes fivesegments - men's wear, women's wear, kids wear, unisex anduniforms. Men's wear is the largest segment whereas uniformsare the fastest-growing segment. In recent years, the women'swear category has witnessed healthy growth in organizedsegment, especially in the lingerie and western wear sub-segments. Apparel manufacturing being the least capital-intensive section of the textile value chain is characterizedby low entry barriers, hence is highly fragmented. It is alsohighly labour intensive and requires skilled, unskilled andsemiskilled laborers’.

The Indian apparel market has demonstrated resilience andgrowth in an environment characterized by slow economicgrowth. The domestic apparel market, which was worth INR207,400 crore (~USD 38 billion) as of 2012, is expected togrow at a compound average growth rate (CAGR) of 9% over thenext decade.

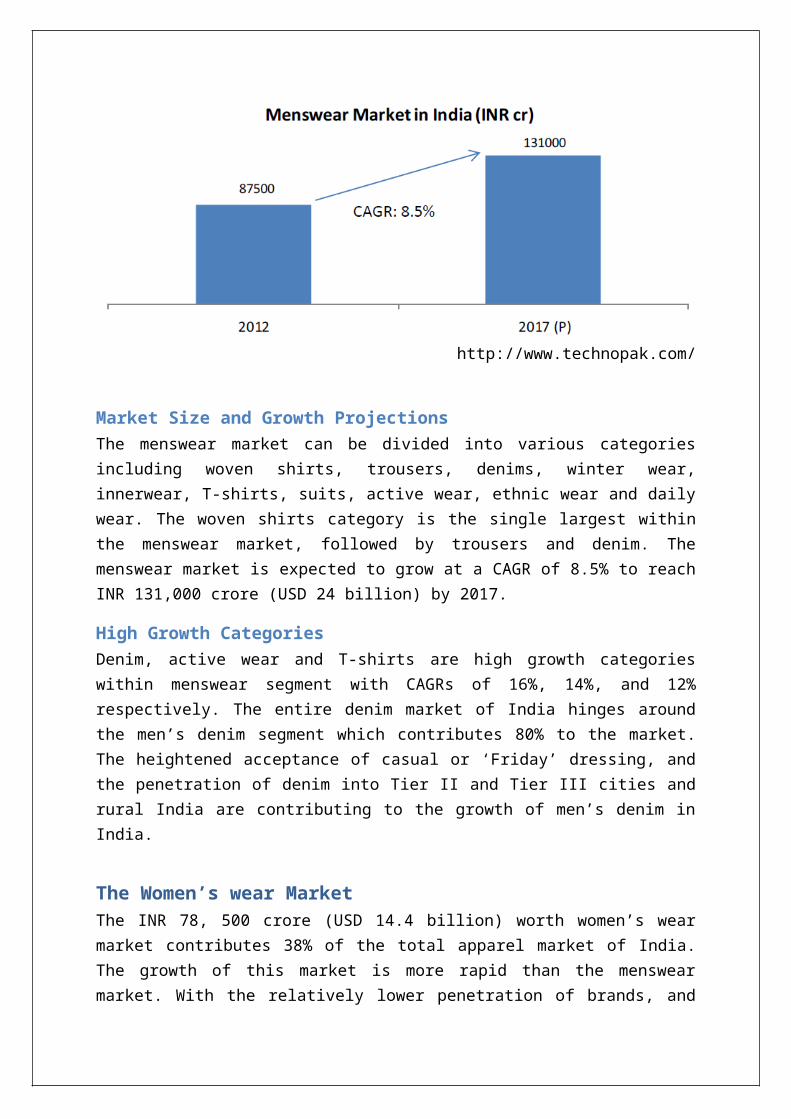

The Menswear MarketWith a market size of INR 87,500 crore (USD 16 billion) in2012, menswear is the largest segment in India’s apparelmarket, accounting for 42% of the overall market. Incomparison, womens wear makes up 38%, while kids wearcomprises 20%, of the market.

http://www.technopak.com/

Market Size and Growth ProjectionsThe menswear market can be divided into various categoriesincluding woven shirts, trousers, denims, winter wear,innerwear, T-shirts, suits, active wear, ethnic wear and dailywear. The woven shirts category is the single largest withinthe menswear market, followed by trousers and denim. Themenswear market is expected to grow at a CAGR of 8.5% to reachINR 131,000 crore (USD 24 billion) by 2017.

High Growth CategoriesDenim, active wear and T-shirts are high growth categorieswithin menswear segment with CAGRs of 16%, 14%, and 12%respectively. The entire denim market of India hinges aroundthe men’s denim segment which contributes 80% to the market.The heightened acceptance of casual or ‘Friday’ dressing, andthe penetration of denim into Tier II and Tier III cities andrural India are contributing to the growth of men’s denim inIndia.

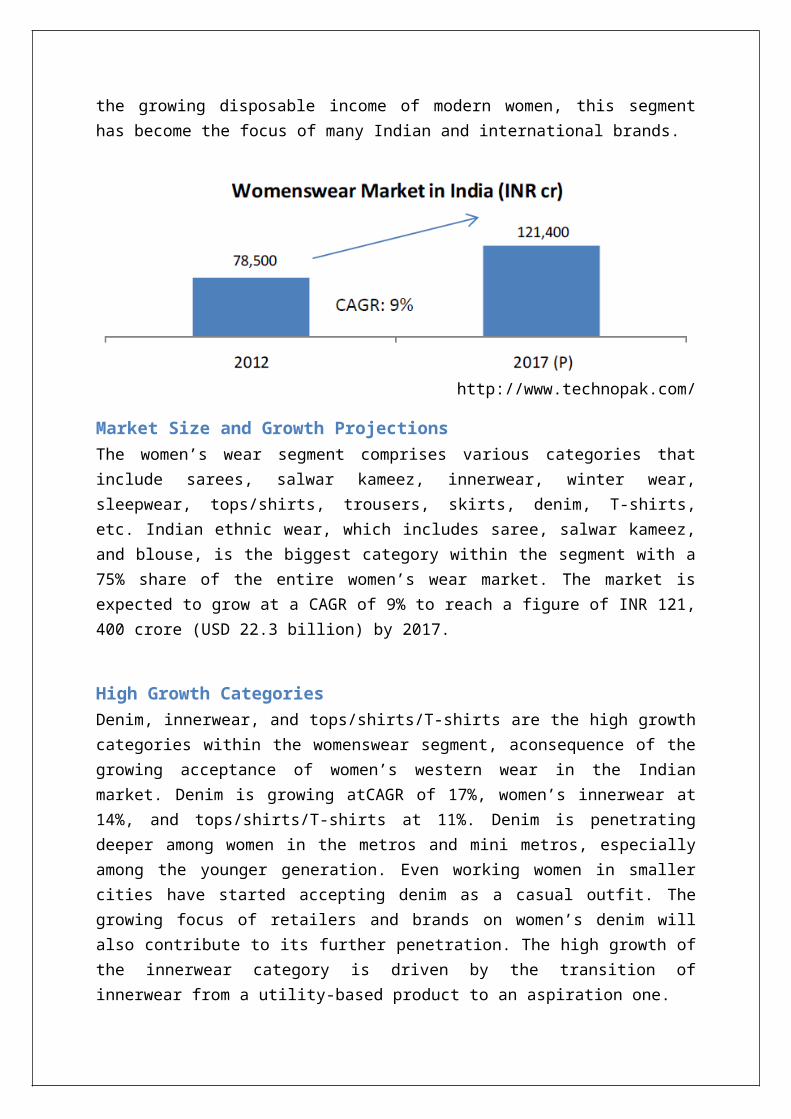

The Women’s wear MarketThe INR 78, 500 crore (USD 14.4 billion) worth women’s wearmarket contributes 38% of the total apparel market of India.The growth of this market is more rapid than the menswearmarket. With the relatively lower penetration of brands, and

the growing disposable income of modern women, this segmenthas become the focus of many Indian and international brands.

http://www.technopak.com/

Market Size and Growth ProjectionsThe women’s wear segment comprises various categories thatinclude sarees, salwar kameez, innerwear, winter wear,sleepwear, tops/shirts, trousers, skirts, denim, T-shirts,etc. Indian ethnic wear, which includes saree, salwar kameez,and blouse, is the biggest category within the segment with a75% share of the entire women’s wear market. The market isexpected to grow at a CAGR of 9% to reach a figure of INR 121,400 crore (USD 22.3 billion) by 2017.

High Growth CategoriesDenim, innerwear, and tops/shirts/T-shirts are the high growthcategories within the womenswear segment, aconsequence of thegrowing acceptance of women’s western wear in the Indianmarket. Denim is growing atCAGR of 17%, women’s innerwear at14%, and tops/shirts/T-shirts at 11%. Denim is penetratingdeeper among women in the metros and mini metros, especiallyamong the younger generation. Even working women in smallercities have started accepting denim as a casual outfit. Thegrowing focus of retailers and brands on women’s denim willalso contribute to its further penetration. The high growth ofthe innerwear category is driven by the transition ofinnerwear from a utility-based product to an aspiration one.

The Innerwear CategoryInnerwear is one of the high growth categories in the apparelmarket and promises growth and innovation. The increase inincome levels, along with higher discretionary spending,growing fashion orientation of consumers, and productinnovations by the innerwear market have turned innerwear froma traditionally utilitarian item to an essential fashionrequirement. The size of the Indian Innerwear market is INR15,870 crore (USD 2.9 billion); the category is also growingat an impressive CAGR of 12% and is expected to reach INR27,900 crore (USD 5.1 billion) by 2017. The women’s innerwearmarket, which is driven by value-added innerwear products,contributes around 60% to the market. The growth of theinnerwear category is primarily centered in urban India. Thetrend towards western outfits, combined with the demand foroccasion- and outfit-based innerwear, is acting as a boost forthe market. The demand for innerwear with higher functionalityand greater comfort is rising fast. The market for inner wearproduct variations like seamless intimates, plus size innerwear, body shape enhancers, etc. is burgeoning in the metrosand mini metros.

Future OutlookSimply put, the future of the apparel market, and theinnerwear category, looks promising. At the same time,fashionretailers have to face some daunting challenges prior totapping the extant opportunities. Rising realestate costs,increasing power tariffs, and supply chain inefficiencies aresome of the issues that have to betackled with utmostprudence. The growth story of Indian consumption is expectedto revive in the medium to long term, but it will requireimprovements in the overall business performance andmanagerial prudence of the highest degree to benefit from thisgrowth. To emerge a winner in a market marked by the presenceof multiple players, brands and retailers have to optimizetheir business operations by addressing the challenges and

harnessing market opportunities. Understanding the psyche ofthe Indian consumer, amalgamating the Indian style offunctioning with western management techniques, and tailoringfashion offerings to defined consumer segments, are some ofthe key areas upon which fashion and innerwear players have tofocus.

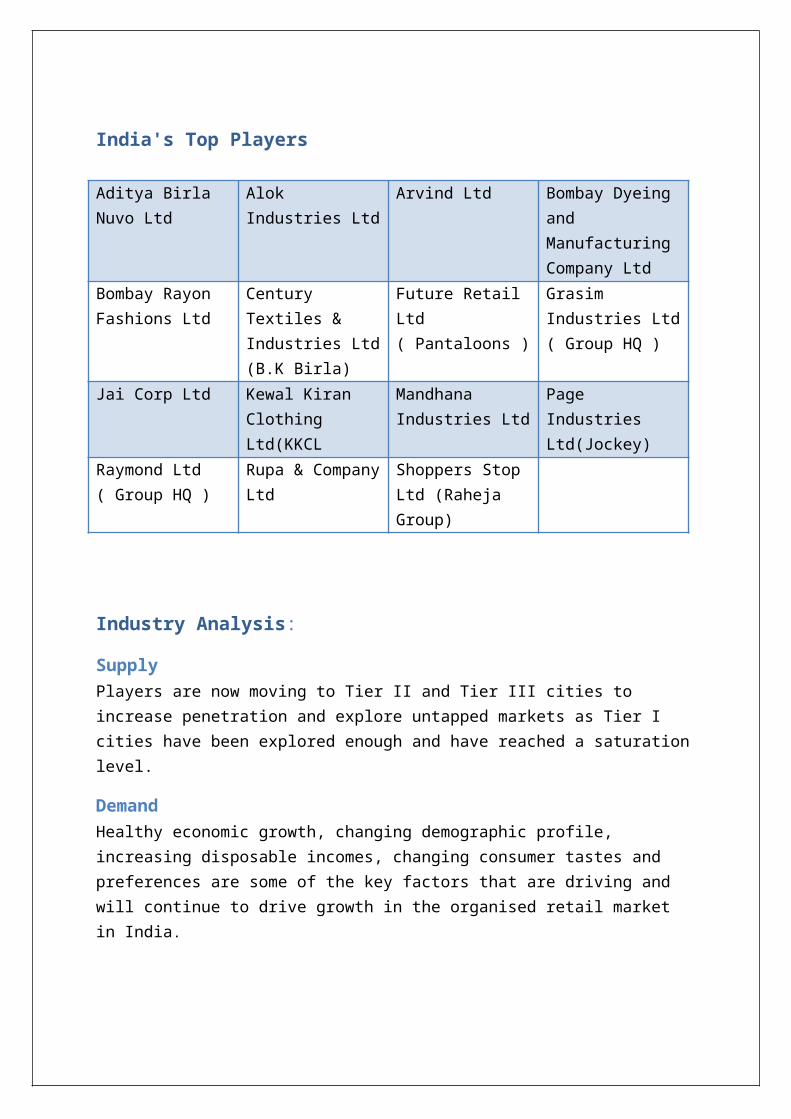

India's Top Players

Aditya Birla Nuvo Ltd

Alok Industries Ltd

Arvind Ltd Bombay Dyeing and Manufacturing Company Ltd

Bombay Rayon Fashions Ltd

Century Textiles & Industries Ltd(B.K Birla)

Future Retail Ltd ( Pantaloons )

Grasim Industries Ltd( Group HQ )

Jai Corp Ltd Kewal Kiran Clothing Ltd(KKCL

Mandhana Industries Ltd

Page Industries Ltd(Jockey)

Raymond Ltd ( Group HQ )

Rupa & CompanyLtd

Shoppers Stop Ltd (Raheja Group)

Industry Analysis:

SupplyPlayers are now moving to Tier II and Tier III cities to increase penetration and explore untapped markets as Tier I cities have been explored enough and have reached a saturationlevel.

DemandHealthy economic growth, changing demographic profile, increasing disposable incomes, changing consumer tastes and preferences are some of the key factors that are driving and will continue to drive growth in the organised retail market in India.

Pestle: Apparel Industry in India is dominated by unorganized sector and with the increasing spending power of the consumers, the industry is witnessing a surge in the advent of foreign players, High-end Boutique stores are coming up in the market to tap the rising demand. The factors under Pestle analysis will be rated in a scale of 1-10, with 10 being most favourable for the industry. The Pestle analysis for Apparel industry is as follows:

Political Factor: Rating 5/10.1. The country is due for general election in coming months,

the results of the elections will be curial for the industry because if Congress (Ruling party), does not come to power than the chances of FDI in retail industry will be in jeopardy which will have direct impact on the growth aspect of the Apparel industry.

2. The country’s political strategy is also not very clear in supporting or opposing the retail industry, at point government propose a tax hike and at other propose to boost the sector with grants, which make the players think about expanding the business or not.

3. Although no party supports this industry but as the industry gives good export revenue and provide huge employment opportunity, this sector is bound to see some legislation in its favour in the coming years.

Economic Factor: Rating 6/101. The country is expected to grow at a rate of 5-6 % in the

coming years, which although is not great but when compared to developed countries it is good.

2. The middle class which currently forms up to be around 40% of the population is growing both in its income and also size which is good for organized apparel retail, as these are the major target market of the industry.

3. The Chinese economy is also going through trouble as the labour cost is rising major companies are shifting their

bases to other countries, which may prove to be favourable for the country because if some major players move their bases to India this will further improve the synergies of the industry making it more competitive.

Social Factors: Rating 6/101. The Indian society is very famous for its assimilation of

new trends and this essentially makes the country a good place for international players to leverage their global offerings, hence this will also improve the chances of FDI in retail.

2. The country is seeing a trend in single family with double earning giving it more spending power to thrust the sector’s growth.

3. Although organized retail is growing, malls are facing grave problems with many of the project delayed and many other running in loss, this is a hindrance for organized apparel.

4. The country is also observing a major shift towards online retailing which basically is organized retailing and this giving a major thrust for the growth of major retail players, but this is also bringing in major international players like Amazon, EBay etc.

Technological Factors: Rating 8/101. Technology is seeing great leaps in the current days and

with innovation coming in every day, this is helping apparel retailing in the most important ways like improving supply chain efficiency, Improving customer engagement programmes, etc.

2. We all know that major players like Wal-Mart, Zara, and IKEA etc use extensive technology; this will make the market more competitive and will shift the consumers towards organized sector which has both volumes and more variety in its offerings.

Legal Factors: Rating 3/101. The country ranks 134th out of 189 countries in Doing

Business Ranking, which tell the problems a company, should face setting up a business in India.

2. India performs exceptionally poor in enforcing contracts which shows the problem with legal procedures.

3. Country is still not sure to allow FDI in retail in big way (51% in Multi Brand) with many political parties opposing it; this makes the legal framework of the country poor.

Environment Factors: Rating 8/101. The Organized Retail of Apparel industry is not much

impacted by environmental factors in a big way.2. Although in India it is a very tedious process to get

environmental clearance from the ministry, but this is majorly required by manufacturing sector. Hence it will not impact the retail side of the business.

Porters Five Forces Model: The ratings represent the acuteness for example 10 in Barriersto entry means very difficult to enter the market, and vice versa.

Barriers to entry: Rating 6/101. The Industry has moderate expense in fixed cost and also

the cost of exit is high.2. Reforms by India in opening up its economy have greatly

improved trade prospects, but major barriers still exist such as regulatory issues, supply chain complexities, inefficient infrastructure, and automatic approval not being allowed for foreign investment in retail.

3. With the central government clearance of FDI in multi brand retail the prospects are brighter now.

4. The high rental in the limited locations is also a major challenge for any entrant into the market.

5. The supply of labour is good and also the cost is less ascompared to developed countries which makes entry into the market easy.

Bargaining power of suppliers: Rating 4/101. The country is a big manufacturer and exporter of textile

and hence there is good supply of raw material at reasonable price.

2. The competition is high among supplier which gives good amount of bargaining power in the hands of retailers.

Bargaining power of customers: Rating 6/101. The consumer currently holds the highest variety of

formats, stores and brands to choose from which is increasing the power of customers.

2. Although apparel are basic necessity for customers but due to high competition which is reflected in the different types of discount provided by almost all of organized retailers.

3. With the advent of foreign players like Zara, Foreever21,etc consumers are becoming even more demanding, at least in the design and variety aspect of offerings.

Competition: Rating 7/101. Currently there is a stiff competition in the market at

least in the metros and tier 1 cities, but in the tier 2 & 3 cities and towns the market is largely untapped.

2. Brands like Life Style, Reliance trends, Bharti, Future Group are present in the Multi brand formats, whereas in company owned stores brands like United Colours of Benetton, Levis, Kewal Kiran Clothing, Aditya Birla group etc have good presence.

3. With the opening up of FDI, many more foreign brands likeH&M, Wal-Mart, Tesco etc will try to take control over the market in the near future.

Substitutes: Rating 8/101. Organized Apparel retail industry covers only about 5% of

the total market and the rest of industry.2. Un-organized sector basically is the main challenge in

front of organized sector because the consumers in India still prefer to shop in these markets and this behaviour is the main challenge the industry is currently facing.

LEVIS

Levi Strauss & Co. (LS&CO.) is one of the world's largestbrand-name apparel marketers with sales in more than 110countries. There is no other company with a comparable globalpresence in the jeans and casual pants markets. Today, theLevi's® trademark is one of the most recognized in the worldand is registered in more than 160 countries. The company isprivately held by descendants of the family of Levi Strauss.Shares of company stock are not publicly traded.

The company employs a staff of approximately 8,850 peopleworldwide, including approximately 1,000 people at its SanFrancisco, California headquarters. Levi Strauss & Cocurrently makes jeans in approximately 108 sizes and 20 finishfabrics. With 2007 net sales of $4.1 billion, the company iscommitted to building upon strong heritage and brand equity asthey position the company for future growth.

LEVIS STRAUSS INDIA LIMITED [LSIL]

LSIL was established in 1994 under the parent American apparelcompany, Levis Strauss & Co. LSIL is the most prominentjeanswear company in India with about 270 flagship stores, 500other points of sale, across more than 200 towns across thecountry.

LSIL provides the parent company with about 8.8% of the totalsales.

Levi’s was considered as the “most admired jeanswear brand ofthe year” for 6 years in a row.

SWOT AnalysisStrengths

1. Levi’s enjoys high brand equity. People all around theworld recognize the brand name.

2. Levi’s products are unique and innovative in the style.3. A lot of variety is offered by Levi’s ranging from

sunglasses to skirts and shirts.4. The products are renowned and are considered as the most

durable i.e. the long lasting products.5. Levi’s follows a high standard of quality.6. Expertise in Jeans Industry7. Distribution Channels and Global Outsourcing8. Finance and Access to International Capital9. Has over 470 self operated stored globally managed by

16000+ employees10. Levi’s marketing includes retro popular songs in its

TVC ad campaigns11. Over 60 and 25 manufacturing plants in US and abroad

respectively

Weakness

1. Levi’s products are considered as very expensive.Therefore a large percentage of people are reluctant tobuy the products.

2. As no discounts are present and products are sold atfixed prices many customers are lost.

3. Levi’s does not provide any services like free deliveryetc.

4. Too narrow a product line5. High Pressures of Brand Protection6. Increasing competition means limited scope for growth

Opportunities

1. Levi’s can do more well in the women section. Thissection is give less importance as compared to the mensection.

2. The kid’s section, which has been started from few years,should also be given proper attention to gain customers.

3. Growing casual wear market4. Low manufacturing and production costs in various

international markets5. Increasing acceptability of western wear across the

world

Threats

1. Increasing number of competitors2. Fast changing consumer tastes3. Lack of protection of property rights in some countries

like China4. Increasing Competition and Product Substitution

Strategy of LevisLevis is often associated with the origin of the jeans, whichis reflected in most of its ads too.Products are usually considered to be the No.1 factor

contributing towards building goodwill of a firm. A productshould be unique, durable, reliable, comfortable andeconomical. Following are some of the basic attributes ofLS&CO.’S products

Variety

Features

Design

Color

Size

VARIETY

Levi’s products today are perceived by many as a symbol ofyouth, freedom, confidence, individualism, independence &comfort.

Levi’s jeans have been present at nearly every pivotal momentin history and culture for the past 150 years.

Comfort

Levi’s jeans and other products are comfortable enough to beworn even at the times of protest, war, Cultural Revolution,relative peace and pure fun.

Durability

The two figures on the patch of Levi’s jeans with whips inhand pulling in opposite directions, yet the jeans remainintact; symbolize the strength and durability of the ‘Patentriveted clothing’.

Style

Clothing means more than just fabric, thread and rivets. Toclothe oneself means to put on something that symbolizes whoyou are. Levi’s jeans are available in different styles formen and women.

Consumer Profile

LEVI’s specifically targets customers falling under:

a) Upper Class

b) Upper Middle Class

1. It emphasizes more on the age group of 13-24(youngsters), although it has its product range forpeople with above 30 yrs age.

2. Its strategy is basically on having long-term relationswith their customers by designing jeans, shape, color,and cloth so that fun mix and match clothes withaccessories in style of fashion

3. In 1930’s Jeans were positioned as being worn by“cowboys”.

4. Consumer demand shifts from durability of jeans tofashion of jeans.

Culturally, jeans became symbol of youth and rebellion

Trading Area and location strategyLevi Strauss & Co. is a worldwide corporation organized intothree geographic divisions:

Levi Strauss, North America (LSNA)

Based in the San Francisco headquarters

Levi Strauss Europe (LSE)

Based in Brussels

Asia Pacific Division (APD)

Based in Singapore

Levi Strauss & Co.'s Asia Pacific Division is comprised ofsubsidiary businesses, licensees and distributors throughoutAsia Pacific, Middle East, Africa and Latin America. TheDivision sources, manufactures and markets Levi's®, Dockers®,and Levi Strauss Signature™ products through 14 affiliates.The company employs approximately 2,500 talented peopleworking together to ensure that the apparel brands are leadersin this part of the world. The division is comprised of whollyowned-and-operated businesses, licensees and distributorsthroughout Asia and the Pacific including Pakistan.

Levi's® brand of products are sold in 49 countries, Dockers®brand in 31 countries and Levi Strauss Signature™ brand in 4countries:

Store location is one of the prime considerations in acustomer store choice. Location decisions have long termstrategic importance. Location decisions are hard to change asthey involve a huge involvement. LSIL has truly understoodthese issues and strategically located its stores at the bestplaces.

The factors that LSIL has considered for deciding the locationare given below:

1) Demographics – Lifestyle, income potential, occupationmix, nearby offices.

2) Traffic & Access – Number & types of vehicles, access tostore, street congestion, mass transit presence.

3) Competition – Number & types of stores in the area, keyplayer analysis, location of competitor.

4) Site factors – Size of site, Parking space, visibility ofstore, entry & exit, building condition, retailersassociation.

5) Cost factors – Terms of lease or rent, rent rates,operation cost, local taxes, membership cost ofassociation of retailers.

LEVI’S stores in DELHI/NCR:

1. Noida, Sector – 18: Vintage retail and merchandising,G61-62, Opposite McDonalds (Franchise/MBO)

2. Noida, Sector -18: Millenium (Flagship Store)3. Noida, Sector – 18: TGIP (Flagship Store)4. New Delhi, Connaught Place – F-19, Inner circle.

(Flagship Store)5. New Delhi, Katwaria Sarai (Franchise) and others

LSIL fashion merchandise stores can be categorized into thefollowing formats according to the location:

Exclusive brand outlets / Flagship stores (EBOs) – EBO is adistribution strategy where the retailer sells its products inone retail outlet in a specific geographical area. An EBO issuitable in a shopping centre/central business district whichis the main centre of commerce and trade in the city. Usuallyevery Metro city has more than one central business district.It is better to have EBOs in each of these places as it givesa significant brand presence due to high customer trafficmovement and also footfalls will increase and convert suspectcustomers into prospective clients.

Multi brand outlets (MBOs) – MBOs are retail stores not ownedby the retailer but a channel partner of the retailer who hasmade agreements with various retailers to sell their brands intheir outlets. This type of brand outlets is suitable in asecondary business district which has shopping area that issmaller than the central business district and revolves aroundat least one variety store at a major street location. TheseMBOs are available in plenty in Metro cities and Tier 2 & 3cities. Customers in these areas are not specifically brandconscious but more of value buyers and they prefer to shop instores which house a variety of brands.

Franchise – Franchising is an innovative method ofdistributing goods and services where the franchisor(retailer) provides products and assigns to franchisees the

right to market and distribute the franchisor’s goods andservices. The business format franchisee model is the mostpopular method in apparel franchising. The franchise model ofstore operations is best suited when the retailer wants toenter new geographical area where limited knowledge isavailable to conditions of business and market potential isnot very clear. Also having own stores in new locationsattracts lot of investment and riskier. It is better to enternew geographical areas through franchise model and with itssuccess the retailer can plan to expand his own market throughopening of EBOs and Flagship stores.

Store Mapping of LEVI’S Fashion Merchandise Retail Outlets:

Thus LSIL has taken care in devising a well framed locationstrategy for its retail outlets so as to enhance itsvisibility and attract prospective and also persuade them tobecome brand owners.

Primary Trading Area - 50-80% customers; Central Business Districts - metros - EBOsSecondary Trading Area - 15-25% customers; Secondary Business Districts - Metro, Tier 2 & 3 cities - MBOsFringe Trading Area - 10% customers; Stores in new area- Expansion mode - Franchise

Operations and Merchandize management:Levi Strauss & Co., the iconic American brand founded in 1873,found itself coping with steeply declining revenues and marketshare loss just years after sales hit record highs in the mid-1990s. The company’s financial performance has since stabilized; it reported net revenue of $4.8 billion in 2011, an 8% increase over the previous year.

In the early 2000s, Levi’s responded to its financial challenges, in part, by partnering with Walmart to sell a lower-priced line of jeans at the retail giant’s thousands of stores. Walmart’s corporate website lists a detailed series ofrequirements that suppliers must meet in order to do business with the world’s biggest retailer, among them:

● Lead-Time Requirements: The ability of suppliers to adapt toWalmart’s Club lead-time requirements is highly standardized. Building lines of merchandise for each season is a long-range process that involves much more than simply getting items on store shelves.

● Timely Shipping: Late shipments can translate into great losses – both monetarily and in customer respect. So, suppliers need to combine excellent products with on-time deliveries – at the right cost.

As part of its overhaul to meet Walmart’s stringent supply chain rules, Levi’s made an extensive slate of changes to button up gaps in its logistical operations, according to the CIO.com article. Among the upgrades: adding freight distribution facilities in three states; pre-packing products;and implementing technology to better forecast demand. Levi’s had to integrate its information technology system in order totrack products and provide “real-time data” on manufacturing, distribution and inventory levels.

Watching the trends, managers at apparel-maker Levi Strauss & Co. saw the need to upgrade supply-chain systems and processesfeeding their outlet retailers. Their solution: Isolate these activities in a new distribution centre with a singular focus and outsource the operation to an experienced third party. Nowoverstocks, irregular merchandise and returns no longer clog the arteries of the company's primary distribution centres, Instead, these items - as well as new product samples destinedfor Levi Strauss sales and marketing teams - flow smoothly through the company's dedicated facility, a new 246,000-square-foot distribution centre.

Another internal driver for change stemmed from the practice of using all four first-quality customer-service centres (CSCs) to handle products for the value-channel stores - a costly, complex process that tended to gum up the CSC's primary function. No investment had been made in improving their handling of off-price products for more than 10 years, and their new CSCs intentionally were not designed to handle the merchandise. With two of its four CSCs having recently been constructed and one completely redesigned, the company's attention was focused on perfecting process flows and maximizing efficiencies. New distribution channels were introduced to meet all those requirements.

Moreover, the new centres complicated the task of feeding merchandise into the value channel, a task that interrupted first-quality product and process flows and constituted an unwanted distraction for distribution centre managers.

Layout analysis and comparison:

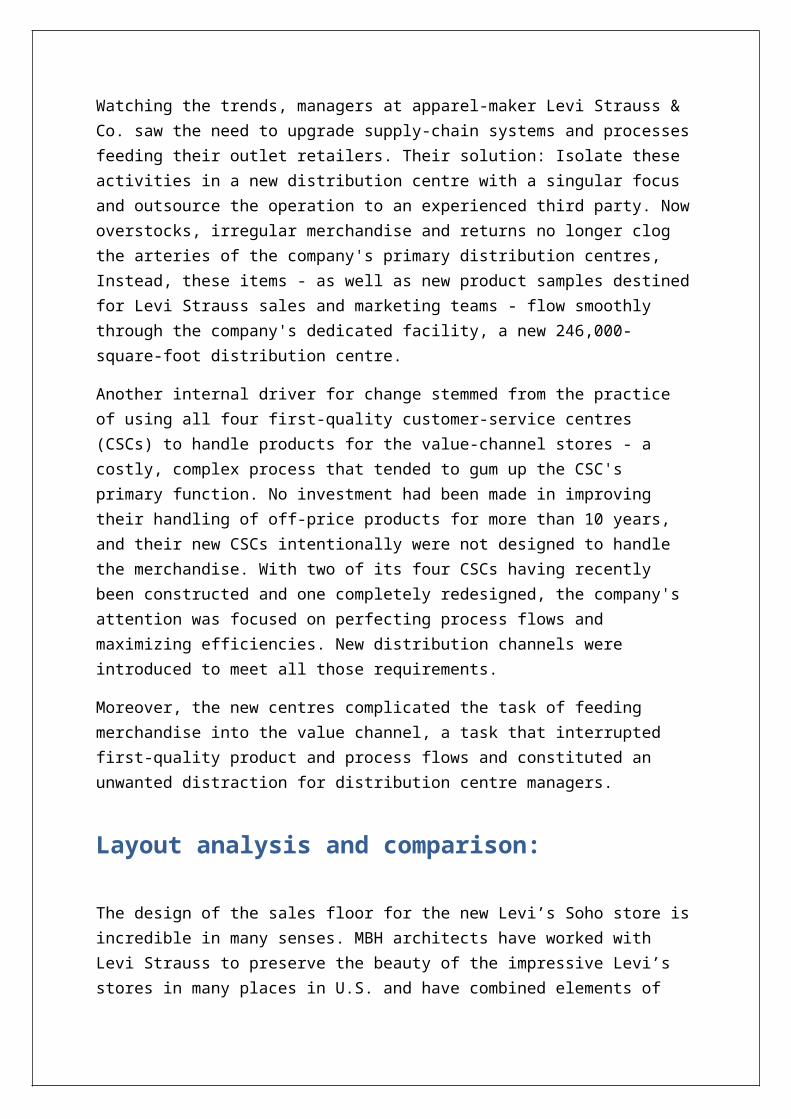

The design of the sales floor for the new Levi’s Soho store isincredible in many senses. MBH architects have worked with Levi Strauss to preserve the beauty of the impressive Levi’s stores in many places in U.S. and have combined elements of

the original structure with the iconic Levi’s brand. Minimising additional elements they were able to retain the ornate steel columns as an original feature of the building and incorporate them into the layout.

Innovative bundles of twisting rope are suspended as light fixtures over denim displays featuring rough-sawn logs. The new dressing rooms have been inspired by Yosemite National Park and are packed with ‘Tents’ rather than the traditional stalls.

Colour is introduced using red and yellow neon signage in the shape of Levi’s instantly recognisable logo as a focal point above the cash draws, this instantly creates a warm glow that bounces off the darkly painted ceilings to the merchandise below.

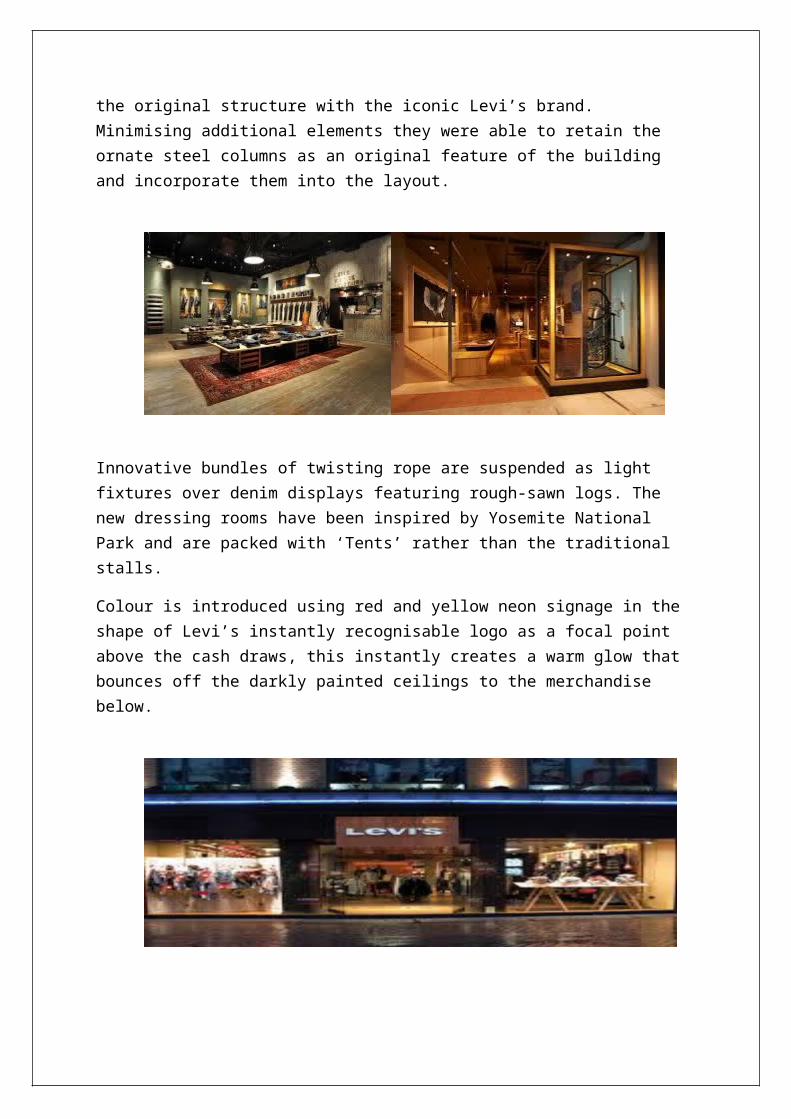

Levi Strauss & Co have demonstrated how to really showcase their established brand by enveloping the sales floor in neutral colours and through using the natural resource of woodfixtures and displays in varying textures and neutral tones. The combination of ornate steel columns, neutral backdrop and natural wood textures allow their industrial and outdoorsy brand character to shine through and take centre stage.

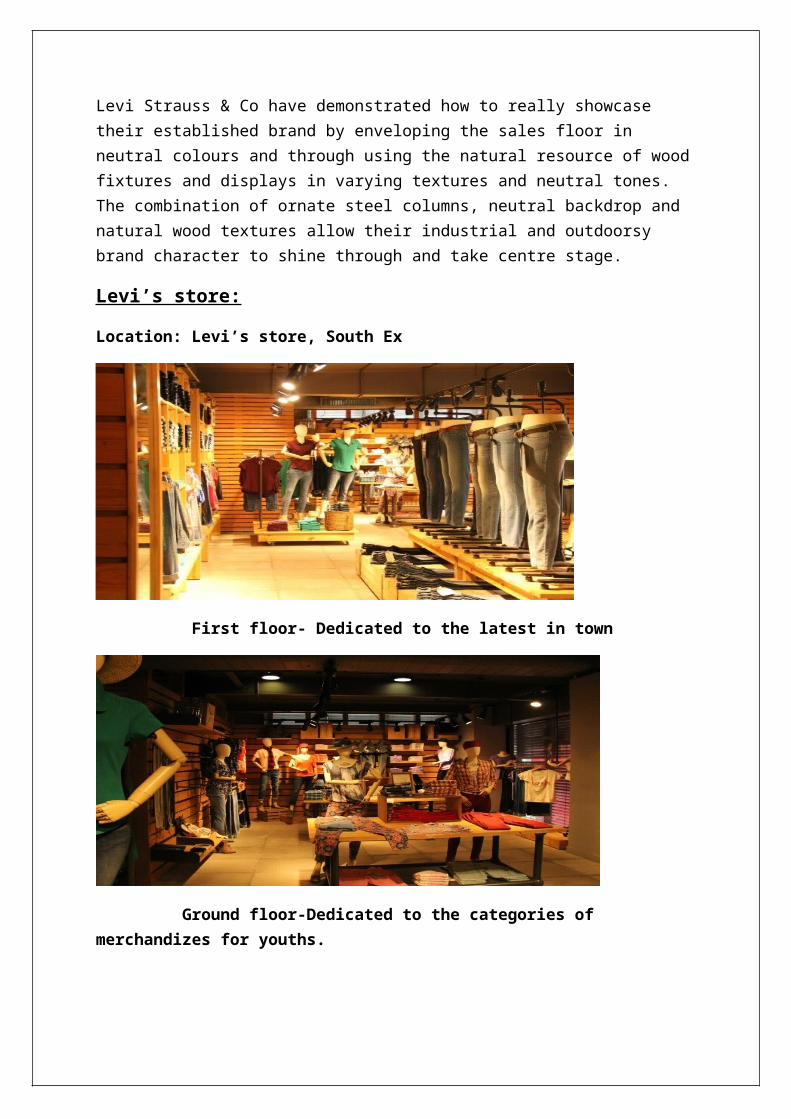

Levi’s store:

Location: Levi’s store, South Ex

First floor- Dedicated to the latest in town

Ground floor-Dedicated to the categories of merchandizes for youths.

Red Format - Dlf Select City Walk, Saket

Levis Black Format store, Dwarka

Merchandize displays:

Nesting Table Grill

D BART-STAND

Communications and promotion strategy:

The problem facing Levi Strauss was that jeans were increasingly regarded as ‘uncool’. In 1996 the company reported record one-year sales of $7.1 billion and a profit ofmore than $1 billion.

By the end of 1999, sales had fallen to $5.1 billion and it had barely broke even on profits despite closing 30 of its 51 factories and laying off about 15,000 people, or 40 per cent of its workers.

The root causes go back as far as 1992 when rap music emerged as a cultural phenomenon and baggy trousers were its generational signature. Unfortunately, Levi’s failed to connect with young customers. While competitors such as Gap, Diesel, Wrangler and Pepe stole market share Levi’s market share shrank from 31 to 14 per cent. The problem was complacency; for years Levi’s had been cool—the kind of cool that seems as if it will never end.But nothing lasts forever. One survey reported that the proportion of US teenage males who considered Levi’s to be a ‘cool’ brand plummeted from 21 per cent to 7 per cent between 1994 and 1998.

New strategies:

The continued segmentation and fragmentation of the UK jeans market led Levi’s to organize its marketing around three customer groups: urban opinion-formers, extreme sports, and regular girls and guys. Each handles its own new product development, has its own brand managers and marketing team. The core market remains the 15–25 age groups. Levi Strauss developed new marketing strategies. A new range of non-denim jeans, branded Sta-Prest, was launched in 1999, backed up by amajor TV advertising campaign starring a toy furry animal called Flat Eric. This campaign was well received by its youthaudience. n 2000, Levi’s launched Engineered Jeans, an aggressive modern range billed as a ‘reinvention’ of the five-pocket style to replace the old 501 brand. Described as the ‘twisted original’ the new jeans featured side seams that follow the line of the leg and a curved bottom hem that is slightly shorter at the back to keep it from dragging on the ground. The jeans also had a larger watch pocket to hold itemslike a pager. Under its youth-orientated Silver Tab brand, Levi’s introduced the Mobile Zip-Off Pant, with legs that unzipped to create shorts and the loose Ripcord Pant, which rolled up.

Levi Strauss also altered its approach to massified promotion. It believed that a ‘massified’ image was a

hindrance to being accepted among young consumers. It studied how rave promoters publicized their parties using flyers, ‘wild posting’ on construction sites and lamp- posts, pavement markings and e-mail. It explored how such ‘viral communications’ could be used to infiltrate youth culture. The idea was to introduce the Levi’s brand name into the target consumers’ clubs, concert venues, websites and fanzinesin order for the kids to discover the company’s tag for themselves. Levi’s spent massive sums sponsoring and supporting musicians, bands and concerts in order to communicate with savvy youths who are so smart about media campaigns that the best strategy—as with the Flat Eric campaign—was to try to prod them gently towards the idea that Levi’s is again the ‘cool’ brand. As the president of their advertising agency said, ‘If you go into their environment where they are hanging out, and you speak to them in a way that’s appropriate, then the buzz created from that is spread,and that’s an incredibly powerful way to impact the marketplace.

Type One Jeans, made of dark denim with bright stitching, oversized rivets and large pockets, were launched in 2003. Like Worn Jeans, the brand targeted both young men and women. The accompanying campaign more than matched the company’s reputation for avant-garde advertising. It featured a group of hybrid mouse-humans, conceived to personify the ad’s creative theme of a ‘bold new breed’ of denim. Before the advertising agency, Bartle Bogle Hegarty, shot the ad, focus groups discussed the plot where mouse-humans kidnap a cat and blackmail its owner. The research concluded that Levi’s should tone down the aggression and superiority, and balance the female and male roles more equally from a script that was skewed towards the females. To create even more interest in the brand, Levi’s used a guerrilla marketing technique known as ‘self-discovery’. It left documents purporting to be leaked top- secret memos about the launch in

bus shelters, bars and pubs. A website was also established in support of the brand.

In 2004 Levi’s embarked on an ambitious attempt to relaunch its famous 501 jeans. The brand had been built using music incommercials, a tactic that had often seen tracks shoot to the upper reaches of the pop charts. Levi’s iconic advertising campaigns stopped in 1998 after 13 years. The new campaign, in a first for the brand, was entirely built around dialogue with groups of hip-looking people in their late teens and early twenties, flirting and arguing about their jeans. The jeans themselves were very different to the tight-fitting 501sof yesteryear, being low cut and loose fitting. To emphasizetheir design, the advertisements proclaimed ‘501 jeans with Anti-fit’ and were extensively pre-tested among 15–25 year olds for acceptance. In one, a man dressed in baggy Levi’s argued furiously in Spanish with another dressed in tight trousers about which looked better—the clear implication beingthat the baggy look was far more stylish.

CRM at Levi’s:

The Loop program:

The Levi's® Loop is the Customer Relationship Management program of Levi's® India. It is a program designed to reward people who wear and love the Levi's® brand. Through this program we seek to thank and reward such individuals with rewards and benefits such as points being earned against the purchases, invitations to promotions, special events, product previews and a whole lot more.

Levi's® Loop Points - Get up to 3 Levi's® Loop Points with every Rs.100 on all purchases at participating Exclusive Levi's® Stores. You can then redeem these Loop Points for Levi’s merchandise and a whole lot of other goodies.

Special Privileges - You can look forward to sneak previews, special offers, exclusive invites and Levi's® merchandise – besides the wildest experiences money could never buy!

Loop Exclusives - Every Levi's® Loop limited edition item is strictly reserved for Levi's® Loop members. Outsiders can't get their hands on them!

Celebrations Unbuttoned - We appreciate that you make Levi's® a part of your life which is why we'll be celebrating your special occasions with gifts, discounts and offers, just for you – to make those special moments even more memorable.

Shopping Scoops - Take advantage of exclusive pre-sale premieres. Be the first to know about new product launches andother promotions.

Gigs - Get your name on the hottest Levi's® events in town.

SHOPPERS STOP

The foundation of Shoppers' Stop was laid on October 27, 1991by the K. Raheja group of companies, one of India's biggesthospitality and real estate players. The Group crossed yetanother milestone with its lifestyle venture-Shoppers' Stop.With its immense expertise in the service industry andcreditability, Shoppers' Stop today boasts of 65 retailoutlets across the country i.e. 28 cities and is planning tospread its wings with futuristic expansion plans to meet thechallenges of the retail industry.

A benchmark for the Indian retail industry to follow,Shoppers' Stop has progressed from a single brand shop to aFashion & Lifestyle store for the families. Shoppers' Stop isa household name, known for its superior quality products,services and above all, a complete shopping experience.Shoppers' Stop was the first to redefine shopping experienceand creating a niche for itself in the service industry. AsIndia's first specialty chain with outlets in Mumbai,Bangalore, Delhi, Hyderabad, Jaipur and Chennai, Shoppers'Stop offers a complete range of garments and accessories forthe entire family. More than 25,000 customers walk intoShoppers Stop everyday to feel the experience of shopping.

Andheri was the first store to be opened in India. Theinitiative of this store was taken by B.S.Nagesh at a timewhen the concept of retail industry was just coming into themarket. As on today, the current investors in Shoppers‘Stopare ICICI, IL&FS Investments and Zodiac clothing. Theircombined shareholding inShoppers Stop is 19% while 79% is heldby Raheja Group & balance 2% is held by its employees.

Shopper's Stop is largest chain of department stores atpresent in India. The company has a 19% stake in HypercityRetail (India). The company’s subsidiary Gateway MultichannelRetail (India) has introduced the concept of catalogue stores,call and collects store, internet retail website and telephoneorders

Shopper's Stop store located at Rajouri in New Delhi is thelargest department store in the country. The company ownssubsidiaries namely Crossword Bookstores, Upasna Trading,Shopper's Stop.Com (India), Shopper's Stop Services (India)and Gateway Multichannel Retail (India).

FORMATS UNDER THE BRAND SHOPPERS STOPShoppers stop is anchored across multiple category formats.

1. Shoppers stop: This is the company’s flagship business ofdepartment stores. It offers customers an international

shopping experience through 55 stores 2 airport storesacross 24 cities. It offers a wide assortment of nationaland international brand across categories such as fashionapparel, accessories, cosmetics, perfumes, home andkitchen ware.

2. Home stop: it is first of its kind premium home conceptstore. It has 13 stores across 10 cities. It is a onestop solution for home ranging needs.

3. Crossword: Crossword is the leader in the lifestylebookstore category with a unique product mix of books,magazines, movies etc.

4. Hyper city: it has redefined the experience of the Indianconsumer in the big box mix retail format. The businessoperates a big store big saving by-line and deliversquality products at a great value all under one roof.

5. Mother care and early learning centre6. Estee lauder group of companies: SSL has entered into a

non-exclusive retail agreement with world renownedcosmetics major estee lauder to open stores forinternational brands

7. Site: shopperstop.com has reached out to customers acrossIndia. It delivers more than 1000 cities and acrosstowns.

8. Nuance group (India) Pvt. Ltd.: The Company and theNuance group AG has inked a 50:50 joint venture foroperating duty free stores at airports.

CUSTOMER PROFILESegmentation of customer is done on the basis of demographicsand Psychographics

Demographic segmentation

Age Group: 16-35 Years, families and young couples

Income: Monthly household income above 20,000 per month andspending more than Rs. 15,000.

Psychographic Segmentation:

People who have lifestyle which is out door oriented and theybelong to upper class or upper middle class of the society.

COMMUNICATION AND PROMOTION STRATEGYShoppers stop started its journey of exciting marketingpromotion and in store excitement. In 1997 launchedparikrama. In 2005 Brand positioning was changed from feel theexperience to shopping and beyond. In 2008 repositioned andreinvented as a ‘bridge to luxury’ brand unveiling of the newlogo and tagline START something new

Shoppers stop has over the years introduced clutter breakingcampaigns, innovative activations and attractive promotionsthat kept customers engaged.

1. Brand Campaign ‘Start something New’Through this campaign shoppers stop has voiced varioussocial concerns. The various causes are like waterconservation, use of greener modes of transport ND othercivic issues. The campaign features stylish people insimple day 2 day situations actually doing something new.

2. Start something new todayThis is a series of campaign of small ads that appearevery Thursday on page 3. These ads provide fashiontrends and tips on shopping

3. End of season sale: Shoppers stop launched its delightfully low prices up to51% off sale campaign with innovative and clutterbreaking imagery.In order to promote the end of season sale shoppers stopcrafted distinctive elements across media platform suchas press, outdoor, radio along with dedicated focus onsocial media.

4. Choose your own gift:This is an annual promotion for customers speciallycrafted for them. Instead of offering a pre-selected gift

shopper’s stop offered its loyalty programme member bonusreward points on their purchase which could be redeemedlater.

5. Makeover marathon: this was done in select cities whereincomplimentary makeovers were done by make u artists sothat customers are exposed to international brands.

6. Suits and jacket fest: Shoppers stop made India highest jacket i.e. 22 ft. highto promote suits and jacket fest.

7. Gift cards: The gist card ensures the shoppers stopcustomers have the freedom and felicity to indulge inpersonal choices and preferences

8. World’s largest stocking: To celebrate Christmas shoppersstop made the 223 ft. high stocking when measured fromtoe to cuff.

Digital promotions

1. Facebook and twitter: shoppers stop constantly churns outinteresting and engaging content on the Fb page. Shoppersstop has 4.4 million fans, making it the largest big boxretailer on Facebook in India. It engages its fan on realtime basis through constructive dialogues, uniquepromotions and contests such as New Year gifts etc.

2. YouTube: This gives an opportunity to customers to seeaudio visual content crafted by the brand. Some of thevideos that got maximum views are Gift card, firstcitizen sale preview etc.

3. Innovative use of QR and AR: This is done for the firsttime by any retailer and thus special apps have beendesigned for the same which can be downloaded from theandroid or iTunes market.

4. Exclusive Apps: shoppers stop continues to offers itsloyal customers an exclusive mobile application. Usingthis tailor made app shopper stop first citizen membercan swipe their card without having it. They can alsoview promotions and offers in store.

Shoppers stop has also started with GiftBot app. using thisapplication customers can get gifting idea based on variouscriteria, budget.

Apart From these campaigns the Communication strategy isreaching out to the consumers in their own style and languagefor Eg. The first shoppers stop store in luck now was namedtehzeeb

Shopper stop also did Festive promotion campaign PRIKRAMA inwhich customers get an opportunity to interact with localartisan. Shopper stop also does various promotional campaignslike salwar duppatta exchange. It also organises localfestival like drug puja in Kolkata, onam in south anddhanteras in north.

For PR Shoppers stop entered into agreement with CRY to retaileco-friendly paper bags designed by underprovided children.The part proceeds from the sale of the bags were donated toproject support by CRY and the wardrobe exchange sawtremendous response with 80000 old garments collected fromcustomers who were donated to project concern IndiaFoundation.

Shoppers stop does direct marketing in the form of the cardcalled First citizen that reflects their commitment tooffering their customers the ultimate shopping experience.

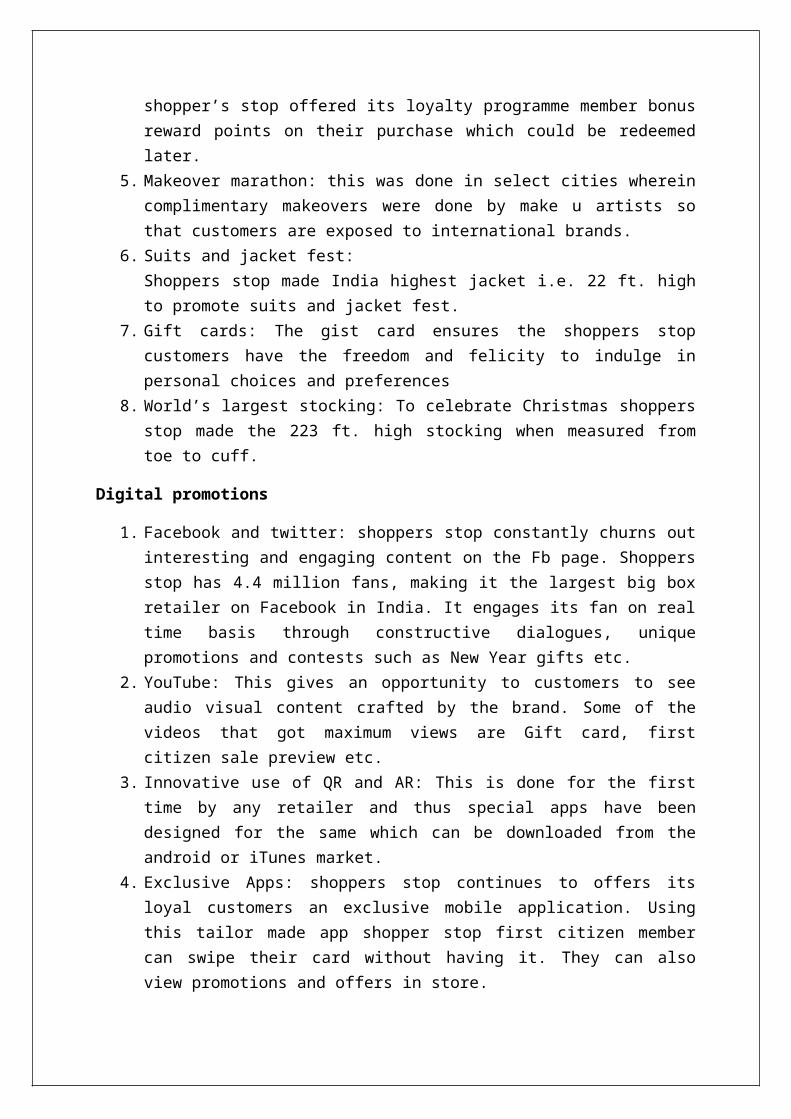

Shoppers stop offers promotion for individual brands as well.These promotions are mentioned on the site of the company. Foreg.

Fig 1: Promotions of individual brands

An eg. Of an advertising campaign done by shopper stop is

Fig2: advertisments

Shoppers stop does advertisement via print ads, social mediaand outdoor advertising

Shoppers stop also organises event like Promotion Campaignslike that of OM SHANTI OM

Fig3: OM shanti OM

Shoppers stop was a partner in promoting OM Shanti Om and hada preview of OM SHANTI OM Merchandise.

CRM

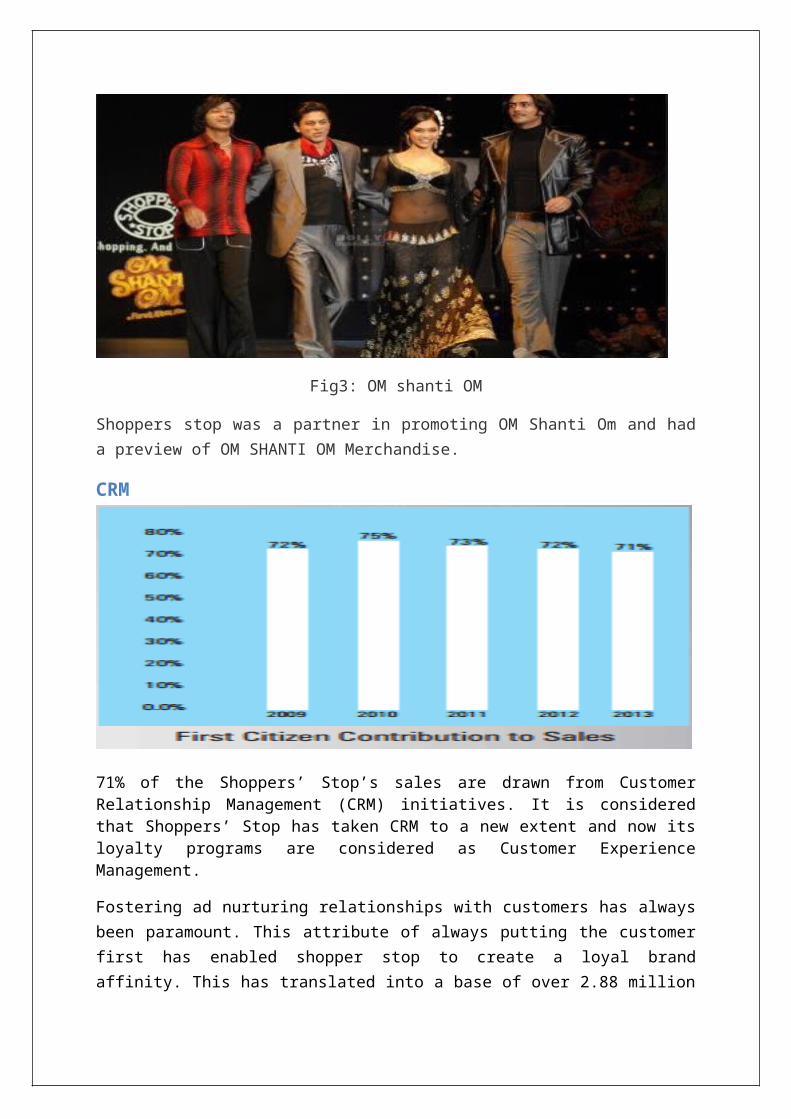

71% of the Shoppers’ Stop’s sales are drawn from CustomerRelationship Management (CRM) initiatives. It is consideredthat Shoppers’ Stop has taken CRM to a new extent and now itsloyalty programs are considered as Customer ExperienceManagement.

Fostering ad nurturing relationships with customers has alwaysbeen paramount. This attribute of always putting the customerfirst has enabled shopper stop to create a loyal brandaffinity. This has translated into a base of over 2.88 million

loyal customers who are a part of the first Citizen Loyaltyprogramme.

It believes that the customer is the whole and soul of thecompany, thus this contributes 71%to the sales. This programmeis one of its kinds in the industry. This programme attractsmore and more members each day. With an addition of upward of0.38 million members during the year 2012, the programcontinues to grow.

The objective is to provide customer delight and enhancecustomer satisfaction. Shoppers stop values the feedback itreceives from its customer. To truly know and understand thecustomer, shoppers stop continuously analyses the proprietaryinformation of the first citizen data. The insight thusgleaned termed ‘First Insight’, helps to plan targeted offersbrands and communication

Benefits come hand in hand with First Citizen program:

Customers gain reward points each time they shop atShoppers’ Stop stores or shoppersstop.com

Exclusive benefits & privileges Exclusive offers on purchase Updates on various products at Shoppers’ Stop Exclusive cash counters which help customers to spend

more time shopping than waiting in a queue

Apart from this the other loyalty initiatives by shoppers stopis

Crossword Book Rewards programme

Customer satisfaction and customer loyalty being the number 1priority, crossword book rewards programme rewards its loyalmembers with points, discounts previews during sales, eventupdates, news on upcoming titles and offers.

Discovery Club Programme

The Hyper CITY discovery club brings every customer greatsaving, exclusive promotion special previews and a whole lotmore. This programme reflects Heredity’s commitment to offerits customers the ultimate shopping experience

Shoppers stop strives to provide customers with the bestoverall experience of shopping. To measure the customerexperience they conduct customer satisfaction surveys toevaluate a range of parameters including merchandise range andquality, store enviornment, staff, schemes, promotions etc.

CRM Activates by the company:

The loyal customers and the CRM initiatives were planned basedupon the business intelligence software used by Shoppers stopto analyse the transaction across the stores. The transactionsdone by the customer base of over 230000 are entered into thesystem and after tracking the favourites of the variouscustomers, shoppers stop tries to keep them informed on thenew product launches and send them updated information on theproducts of their importance. The approaching events atshoppers stop are also informed to the customer so that thetrips can be planned accordingly

The aim of the IT initiative was to create tailors made orunique promotion and scheme that suited the requirements ofthe customers. According to Unnikrishnan Tm (customer careassociate and CTO, solutions and Technology, Shoppers stop),“for this, we needed to understand how, when, where and inwhat combination, the customer buys merchandize.” ShoppersStop had to choose software tools for facilitating theanalysis of the customer data. Unnikrishnan remarks, “We use acombination of business objective and the SAS solution fortrend analysis, promotion management and customer behaviour,segmentation, buying basket analysis, profitability andlifecycle analysis. We also use it to understand theeffectiveness of marketing efforts.”

Under the first Citizen Club, there were 3 categories whichhelped to segment the loyal customers on the basis ofprofitability. The categories were:

Classic moments Silver edge Golden glow

The benefits offered include various VAS like valet parking,home delivery of alteration. But the loyalty programme was ameans to give loyal customers rewards based on the total valueof transactions undergone by them.

To further enhance the benefits, shoppers stop entered into astrategic alliance with Citibank to offer a co-branded creditcard called the First citizen credit card which offered thecombined power of the benefits of a Citibank credit card alongwith the benefits of the loyalty programme. Using this card,customers could enjoy double the reward points, a 0% EMIScheme for purchases, and the card could be used as anATM/debit card as well.

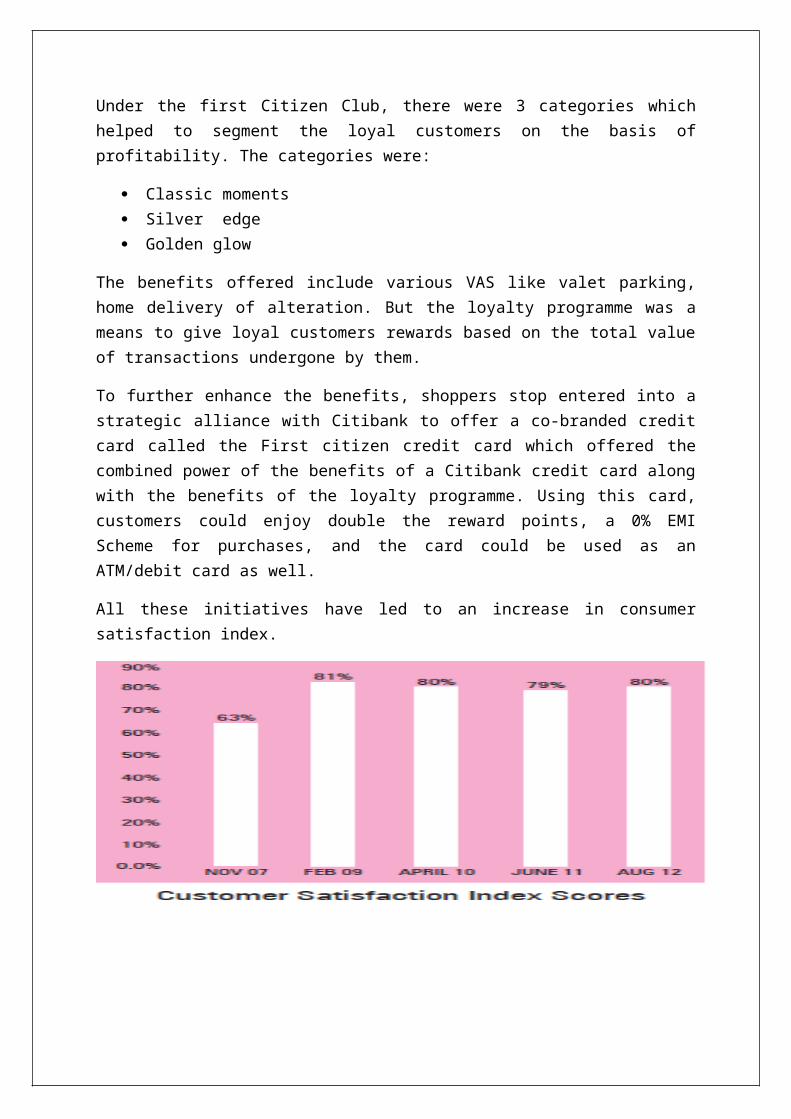

All these initiatives have led to an increase in consumersatisfaction index.