Embed Size (px)

Citation preview

1

The Balanced Scorecard approach for monitoring performance of the company by independent directors

Submitted to

Prepared by

V.Sridhar

V.Sridhar is the Director of Empowertrans Private Limited which is headquartered in Bhubaneswar, India . He has around 25 Years of Experience in various domains like Marketing, Estimation and Costing, Design and Engineering of Sub-Stations, Project Planning, Project Management, Procurement, Quality and safety of the projects, Project Finance and accounting and other functions in Electrical Project industry. He is Qualified Electrical engineer from Vinayaka Mission university, MBA in Finance from Sikkim Manipal university and partipated in the Global Energy seminar conducted by Harvard Business School, Boston

Email: [email protected] Handphone : +919937000046

2

TABLE OF CONTENTS

Sl.No. Title Page No. 1. Program Objective and Goal 3 2. Outcome of the Objective 4 3. Determinant 4 4. Synopsis 5 4.1 Balanced Score board 5 4.2 Financial Perspective 9 4.3 Customer perspective 11 4.4 Internal Process Perspective 12 4.5 Learning and Growth Perspective 13 4.6 Linking Balanced Scorecard Measures to Independent

Director Strategy 15

5. Impact of using BSC by Independent Directors on Organization

20

5.1 Achieving Strategic Alignment 27 6. Contributing Factors 30 6.1 Effective governance of the Board 36 7. Case Study 36 8 Findings 43 9. Conclusion 45 10. Glossary of Terms 45 11. References 49

3

1.0 Program objective and Goal As corporations grow in size and complexity and are increasingly doing business in the global arena, it has become essential for boards to uphold the highest standards of corporate governance and to perform their role effectively. With the advent of Clause 49, board structures have started to change; board committees are playing a more central role, and it is now a requirement for a majority of board directors to be independent. However, the reality is that most listed company boards have little experience of what it means to hear independent voices around the table and little appreciation of the value that a truly diverse group of directors can bring to board performance and debate. The Companies Act, 2013, which replaces more than half a century old law, is a reform oriented, governance focussed and forward looking legislation. While on one hand it confers greater say in governance to the independent directors, one the other hand, it places greater demand on them – in terms of involvement, commitment levels and technical and industry knowledge. In order to make their presence felt and “make it matter”, Independent Directors would need to be agile, proactive, and equipped with industry insights. Stricter criteria for Independence Independent Directors are supposed to bring in an independent judgment on the affairs of the company, safeguard the interests of minority shareholders and give priority to company’s interest as a whole. Under the new law, there is an elaborate code of conduct which independent directors are expected to abide by. The code lays down certain broad guidelines like upholding ethical standards of integrity, acting objectively and most importantly devoting sufficient time and attention for informed and Balanced decision making. There are certain critical functions entrusted to them – to scrutinise the performance of management and to satisfy themselves on the integrity of financial information and robustness of financial controls and risk management. The role of audit committee has been enhanced thereby placing greater responsibilities on independent directors. By defining responsibilities and duties in a mandatory code of conduct, onus has been placed on independent directors thereby reducing their chance of getting the ‘benefit of doubt’ in case of non compliances. This casts an important fiduciary responsibility on Independent Directors towards investor community and other stakeholders. An attempt has been made to strike a fine Balanced by putting in place checks and Balanceds to ensure that empowerment does not lead to unbridled power and authority is exercised with accountability. Greater empowerment coupled with accountability of Independent Director requires them to closely monitor the performance of the company and in terms of delivering best

4

to their minority stakeholders and also adhering to Compliances part. Balanced Scorecard plays a greater role in effective monitoring of the performance of the Organization, Strategic decision making process in the boards, and by making compliances part also as one of the key performance indicators the corporate governance policies of the company can be measured. The objectives of the scorecard are to: • Assist the board, particularly the independent non-executive directors, in the oversight of a company’s strategic process; • Assist the board in dealing with strategic choice and transformational change; • Give assurance to the board in relation to the company’s strategic position and progress; • Track actions in, and outputs from, the strategic process – not the detailed content; and • Assist the board in identifying key points at which it needs to take decisions.

2.0 Outcome of the objective The outcome of this dissertation is to provide Independent directors to align with the organization in their vision , Goals and governance by using Balanced score card. The Objective of using Balanced score card include:

1. Use of performance data to monitor 2. Improve the effectiveness of organizations 3. Aligning the strategic goals with the vision and mission of the company 4. Making Compliances as measurement and monitoring tool 5. Interests of Minority stake holders 6. To involve other management with the Board and Indepent directors in achieving

long term goals of the organization

3.0 Determinants

The Balanced score card even though it is a continuous process of measurement the usage depends on the Independent directors decision making process and will be tool to determine the following decision making of the organizations:

1. Organization strategic goals in long terms 2. New Investments requiring boards resolution 3. Threats from the competitor and from the substitute products 4. Process cost reduction 5. Recruiting key employees of the company 6. Customers dissatisfaction of the company products 7. Not getting the perceived Profits consistently 8. Ability to respond to abrupt changes in market condition 9. Ability to undertake successful merger and acquisitions

5

10. To understand the customer needs

4.0 Synopsis 4.1 The Balanced Scorecard The collision between the irresistible force to build long range competitive capabilities and the immovable object of the historical –cost financial accounting model has created a new synthesis: the Balanced Scorecard. The Balanced Scorecard retains the traditional financial measures. But financial measures tells the story of the past events, an adequate story for industrial age companies for which investment in long term capabilities and customer relationships were not critical for success. These financial measures are inadequate, However for guiding and evaluating the journey that the information age companies must make to create future values through investments in customers, suppliers, employees, processes, technology and innovation. The Balanced Scorecard complements financial performance of past with the measures of the drivers of the future performance. The objectives and measures of the scorecard are derived from organization vision and strategy. The objectives and measures view organization performance from four perspective: Financial, customer, internal Business process and learning and growth. The Balanced Scorecard expands the set of Business unit objectives beyond summary financial measures. Corporate executives can measure how their business units create value for current and future customers and how they must enhance internal capabilities and the investment in people, systems and procedure necessary to improve future performance. The Balanced Scorecard captures critical value creation activities created by skilled motivated organizational participants. While retaining via the financial perspective , an interest short term performance , the Balanced scorecard clearly reveals the value drivers for superior long terms financial and competitive performance. The key to the popularity of the scorecard may lie in its flexibility and adaptability. Whether for commercial organisations, governed by profits, public sector operations governed by service delivery, or not-for-profit organisations driven by commitment to a particular cause, a scorecard that improves performance (either through Performance measurement, or via strategy refinement), can be developed. When first developed, the scorecard was positioned as a holistic performance-measurement framework, which could provide management with useful information relating to financial performance, internal processes, and customer perceptions and internal learning and growth.

6

Translating vision and Strategy: Four Perspectives Fig 1-1 The opportunity to use such information to satisfy the concerns of not only internal management but also external stakeholders was soon acknowledged, and companies such as Sears, Citicorp, and AT&T, as well as numerous public sector organisations developed such ‘stakeholder scorecards’. By first identifying the interested parties whose objectives they sought to satisfy, (shareholders, customers, employees, suppliers etc), the organisations then defined goals for each and developed stakeholder cards of appropriately Balanced stakeholder-related measures and targets, in an attempt to meet the needs of all. As organisations developed their own scorecards to measure performance, each generated valuable information, relating to many aspects of organisational activity. Close analysis of this information, added to organisational knowledge of operations and their impacts, made people aware of the potential of the framework from a performance management perspective rather than one of performance measurement.

7

Through the use of ‘strategic objectives’, many organisations, both private and public, have used the scorecard to place strategy, rather than financial metrics (simple budgets, economic value added, shareholder return etc.) at the heart of their management processes. Strategic objectives, first represented as short sentences attached to each of the four perspectives, can be used to highlight the essence of the organisation’s strategy relevant to each. Measures that reflect progress towards the achievement of these Objectives are then selected. Strategy maps provides employees a clear line of sight into how their jobs are linked to the overall objectives of the organization, enabling them to work in a coordinated, collaborative fashion toward the company’s desired goals. The maps provide a visual representation of a company’s critical objectives and the crucial relationships among them that drive organizational performance. Strategy maps can depict objectives for revenue growth; targeted customer markets in which profitable growth will occur; value propositions that will lead to customers doing more business and at higher margins; the key role of innovation and excellence in products, services, and processes; and the investments required in people and systems to generate and sustain the projected growth. Strategy maps show the cause-and-effect links by which specific improvements create desired outcomes—for example, how faster process-cycle times and enhanced employee capabilities will increase retention of customers and thus increase a company’s revenues. From a larger perspective, strategy maps show how an organization will convert its initiatives and resources—including intangible assets such as corporate culture and employee knowledge—into tangible outcomes. The template provides a common framework and language that can be used to describe any strategy, much like financial statements provide a generally accepted structure for describing financial performance. A strategy map enables an organization to describe and illustrate, in clear and general language, its objectives, initiatives, and targets; the measures used to assess its performance (such as market share and customer surveys); and the linkages that are the foundation for strategic direction.

From the Top Down

The best way to build strategy maps is from the top down, starting with the destination and then charting the routes that will lead there. Corporate executives should first review their mission statement and their core values—why their company exists and what it believes in. With that information, managers can develop a strategic vision, or what the company wants to become. This vision should create a clear picture of the company’s overall goal—for example, to become the profit leader in an industry. A strategy must then define the logic of how to arrive at that destination.

8

Customer Intimacy

Product leadership

Strategy Map Example Shareholder value

ROCE

Financial Perspective New Revenue Sources Customer Profitability Cost per unit Customer Perspective Customer value Proposition Internal Perspective Learning And Growth perspective

Improve Shareholder value

Revenue Growth Strategy Productivity Strategy

Value from new products and

Increase Customer value

Improve Cost strucutre

Improve Asset utilization

Asset Utilization

Operational Excellence

‘Innovate’ (Processes that

create new products and

services)

‘Increase customer value’ ( Customer Management process)

‘ Achieve Operational Excellence’ (Operations and logisitics ProcessseS)

‘ Be a Good Neighbour’ (Regulatory and environmental processes)

Employee Competencies

Technology Corporate Culture

9

Fig 1-2

4.2 Financial Perspective.

Building a strategy map typically starts with a financial strategy for increasing shareholder value. (Nonprofit and government units often place their customers or constituents—not the financials—at the top of their strategy maps.) Companies have two basic levers for their financial strategy: revenue growth and productivity. The former generally has two components: build the franchise with revenue from new markets, new products, and new customers; and increase value to existing customers by deepening relationships with them through expanded sales—for example, cross-selling products or offering bundled products instead of single products. The productivity strategy also usually has two parts: improve the company’s cost structure by reducing direct and indirect expenses, and use assets more efficiently by reducing the working and fixed capital needed to support a given level of business.

In general, the productivity strategy yields results sooner than the growth strategy. But one of the principal contributions of a strategy map is to highlight the opportunities for enhancing financial performance through revenue growth, not just by cost reduction and improved asset utilization. Also, balancing the two strategies helps to ensure that cost and asset reductions do not compromise a company’s growth opportunities with customers.

Mobil’s stated strategic vision was “to be the best integrated refiner-marketer in the United States by efficiently delivering unprecedented value to customers.” The company’s high-level financial goal was to increase its return on capital employed by more than six percentage points within three years. To achieve that, executives used all four of the drivers of a financial strategy that we break out in the strategy map—two for revenue growth and two for productivity. (See the financial portion of the exhibit “Mobil’s Strategy Map.”)

Mobil’s Strategy Map

Shown here is a map for the strategy that Mobil North American Marketing and Refining used to transform itself from a centrally controlled manufacturer of commodity products to a decentralized customer-driven organization. A major part of the strategy was to target consumers who were willing to pay price premiums for gasoline if they could buy at fast, friendly stations that were outfitted with excellent convenience stores. Their purchases enabled Mobil to increase its profit margins and its revenue from nongasoline products. Using the strategy map shown here, Mobil increased its operating cash flow by more than $1 billion per year.

10

**To account for Mobil’s independent-dealer customers—not just consumers—the company adapted the strategy map template to factor in dealer relationships.

11

The revenue growth strategy called for Mobil to expand sales outside of gasoline by offering convenience store products and services, ancillary automotive services (car washes, oil changes, and minor repairs), automotive products (oil, antifreeze, and wiper fluid), and common replacement parts (tires and wiper blades). Also, the company would sell more premium brands to customers, and it would increase sales faster than the industry average. In terms of productivity, Mobil wanted to slash operating expenses per gallon sold to the lowest level in the industry and extract more from existing assets—for example, by reducing the downtime at its oil refineries and increasing their yields.

4.3 Customer Perspective.

The core of any business strategy is the customer value proposition, which describes the unique mix of product and service attributes, customer relations, and corporate image that a company offers. It defines how the organization will differentiate itself from competitors to attract, retain, and deepen relationships with targeted customers. The value proposition is crucial because it helps an organization connect its internal processes to improved outcomes with its customers.

Typically, the value proposition is chosen from among three differentiators: operational excellence (for example, McDonald’s and Dell Computer), customer intimacy (for example, Home Depot and IBM in the 1960s and 1970s), and product leadership (for example, Intel and Sony).2 Companies strive to excel in one of the three areas while maintaining threshold standards in the other two. By identifying its customer value proposition, a company will then know which classes and types of customers to target. In our research, we have found that although a clear definition of the value proposition is the single most important step in developing a strategy, approximately three-quarters of executive teams do not have consensus about this basic information.

The inset of the exhibit “The Balanced Scorecard Strategy Map” highlights the different objectives for the three generic strategy concepts of operational excellence, customer intimacy, and product leadership. Specifically, companies that pursue a strategy of operational excellence need to excel at competitive pricing, product quality and selection, speedy order fulfillment, and on-time delivery. For customer intimacy, an organization must stress the quality of its relationships with customers, including exceptional service and the completeness of the solutions it offers. And companies that pursue a product leadership strategy must concentrate on the functionality, features, and overall performance of its products or services.

Mobil, in the past, had attempted to sell a full range of products and services to all consumers, while still matching the low prices of nearby discount stations. But this unfocused strategy had failed, leading to poor financial performance in the early ’90s. Through market research, Mobil discovered that price-sensitive consumers represented only about 20% of gasoline purchasers, while consumer segments representing nearly 60% of the market might be willing to pay significant price premiums for gasoline if they could buy at stations that were fast, friendly, and outfitted with excellent convenience stores. With this information, Mobil made the crucial decision to adopt a “differentiated value proposition.” The company would target the premium customer segments by offering them immediate access to gasoline pumps, each equipped with a self-payment mechanism; safe, well-lit stations; clean restrooms; convenience stores stocked with fresh, high-quality merchandise; and friendly employees.

12

Mobil decided that the consumer’s buying experience was so central to its strategy that it invested in a new system for measuring its progress in this area. Each month, the company sent “mystery shoppers” to purchase fuel and a snack at every Mobil station nationwide and then asked the shoppers to evaluate their buying experience based on 23 specific criteria. Thus, Mobil could use a fairly simple set of metrics (share of targeted customer segments and a summary score from the mystery shoppers) for its consumer objectives.

But Mobil does not sell directly to consumers. The company’s immediate customers are the independent owners of gasoline stations. These franchised retailers purchase gasoline and other products from Mobil and sell them to consumers in Mobil-branded stations. Because dealers were such a critical part of the new strategy, Mobil included two additional metrics to its customer perspective: dealer profitability and dealer satisfaction.

Thus, Mobil’s complete customer strategy motivated independent dealers to deliver a great buying experience that would attract an increasing share of targeted consumers. These consumers would buy products and services at premium prices, increasing profits for both Mobil and its dealers, who would then continue to be motivated to offer the great buying experience. And this virtuous cycle would generate the revenue growth for Mobil’s financial strategy. Note that the objectives in the customer perspective portion of Mobil’s strategy map were not generic, undifferentiated items like “customer satisfaction.” Instead, they were specific and focused on the company’s strategy.

4.4 Internal Process Perspective.

Once an organization has a clear picture of its customer and financial perspectives, it can then determine the means by which it will achieve the differentiated value proposition for customers and the productivity improvements to reach its financial objectives. The internal process perspective captures these critical organizational activities, which fall into four high-level processes: build the franchise by innovating with new products and services and by penetrating new markets and customer segments; increase customer value by deepening relationships with existing customers; achieve operational excellence by improving supply chain management, the cost, quality, and cycle time of internal processes, asset utilization, and capacity management; and become a good corporate citizen by establishing effective relationships with external stakeholders.

An important caveat to remember here is that while many companies espouse a strategy that calls for innovation or for developing value-adding customer relationships, they mistakenly choose to measure only the cost and quality of their operations—and not their innovations or their customer management processes. These companies have a complete disconnect between their strategy and how they measure it. Not surprisingly, these organizations typically have great difficulty implementing their growth strategies.

The financial benefits from improved business processes typically reveal themselves in stages. Cost savings from increased operational efficiencies and process improvements create short-term benefits. Revenue growth from enhanced customer relationships accrues in the intermediate term. And increased innovation can produce long-term revenue and margin improvements.

13

Thus, a complete strategy should involve generating returns from all three of these internal processes. (See the internal process portion of the exhibit “Mobil’s Strategy Map.”)

Mobil’s internal process objectives included building the franchise by developing new products and services, such as sales from convenience stores; and enhancing customer value by training dealers to become better managers and by helping them generate profits from nongasoline products and services. The plan was that if dealers could capture increased revenues and profits from products other than gasoline, they could then rely less on gasoline sales, allowing Mobil to capture a larger profit share of its sales of gasoline to dealers.

For its customer intimacy strategy, Mobil had to excel at understanding its consumer segments. And because Mobil doesn’t sell directly to consumers, the company also had to concentrate on building best-in-class franchise teams.

Interestingly, Mobil placed a heavy emphasis on objectives to improve its basic refining and distribution operations, such as lowering operating costs, reducing the downtime of equipment, and improving product quality and the number of on-time deliveries.

When a company such as Mobil adopts a customer intimacy strategy, it usually focuses on its customer management processes. But Mobil’s differentiation occurred at the dealer locations, not at its own facilities, which basically produced commodity products (gasoline, heating oil, and jet fuel). So Mobil could not charge its dealers higher prices to make up for any higher costs incurred in its basic manufacturing and distribution operations. Consequently, the company had to focus heavily on achieving operational excellence throughout its value chain of operations.

Finally, as part of both its operational-excellence and corporate-citizen themes, Mobil wanted to eliminate environmental and safety accidents. Executives believed that if there were injuries and other problems at work, then employees were probably not paying sufficient attention to their jobs.

4.5 Learning and Growth Perspective.

The foundation of any strategy map is the learning and growth perspective, which defines the core competencies and skills, the technologies, and the corporate culture needed to support an organization’s strategy. These objectives enable a company to align its human resources and information technology with its strategy. Specifically, the organization must determine how it will satisfy the requirements from critical internal processes, the differentiated value proposition, and customer relationships. Although executive teams readily acknowledge the importance of the learning and growth perspective, they generally have trouble defining the corresponding objectives.

Mobil identified that its employees needed to gain a broader understanding of the marketing and refining business from end to end. Additionally, the company knew it had to nurture the leadership skills that were necessary for its managers to articulate the company’s vision and develop employees. Mobil identified key technologies that it had to develop, including automated equipment for monitoring the refining processes and extensive databases and tools to analyze consumers’ buying experiences.

14

Upon completing its learning and growth perspective, Mobil now had a complete strategy map linked across the four major perspectives, from which Mobil’s different business units and service departments could develop their own detailed maps for their respective operations. This process helped the company detect and fill major gaps in the strategies being implemented at lower levels of the organization. For example, senior management noticed that one business unit had no objectives or metrics for dealers (see the exhibit “What’s Missing?”). Had this unit discovered how to bypass dealers and sell gasoline directly to consumers? Were dealer relationships no longer strategic for this unit? Another business unit had no measure for quality. Had the unit achieved perfection? Strategy maps can help uncover and remedy such omissions.

Strategy Matrix The strategy matrix is another useful visualization and summarization tool. It displays objectives, measures, targets, and initiatives in one table. The strategy matrix can point to areas where scorecard elements might be out of Balanced. For example, there may be a cluster of initiatives around one objective, while other objectives have no supporting initiatives. This can be useful when prioritizing spending for projects. Typically, the strategy matrix will reflect a strategic theme, so one matrix is prepared for each theme.

Strategic Theme: Smart, Profitable Expansion Objective Measure Target Initiative

Fina

ncia

l

Increase % of revenue from new stores

% Revenue from stores opened in last 3 years

> 30% year 1

> 50% year 3

Marketing to new target markets

Avg. # of days to breakeven

< 180 days year 1

< 130 days year 3

Operations review

Site selection

Increase sales efficiency

Revenue per FTE

> $ X year 1

> $ Y year 3 Self-service checkout pilot

Cus

tom

er

Acquire new locations

Avg. # daily customers

> X in first 6 mos.,

> Y in first year,

> Z by year 3

Local marketing/PR campaigns

# of repeat customers

> X in first 6 mos., > Y in first year,

> Z by year 3

Customer loyalty program

Avg. $ customer purchase

> $ X year 1

> $ Y year 3

Coupon program

In-store promotions & classes

Proc

ess

Fact-based site selection

Days lag between market selection and site acquisition

< 90 days year 1

< 70 days year 3

GIS mapping

National brokerage contract

15

Streamline development process

Project duration, site acquisition to opening

< 365 days year 1

< 300 days year 3

Standardize design/build processes

% stores open on schedule

> 93% year 1

> 95% year 2

Web-based project management

Lear

ning

& G

row

th

Use business intelligence systems

% eligible employees trained

>90% year 1

>99% year 2

In-house system training

Integrated knowledge management # paper forms used

< 200 year 1

< 100 year 2

< 5 year 3

Corporate digital nervous system

Figure 1: Example Strategy Matrix (for the Strategy Map shown in Figure 1-2)

4.6 Linking Balanced Scorecard Measures to Independent Director Strategy Most Balanced Scorecard implementations focus on aligning the organization and creating synergies, both inside and among business units. However, companies also turn to the Balanced Scorecard to improve their governance processes and their communication with shareholders. And, as is well known, the main component of the entire intermediation and governance system is the company’s Board of Directors. A proactive and engaged Board and Independent director is essential for designing and executing a strategy successfully. 1. Ensure integrity and compliance Board members should guarantee that the reports and information disclosed accurately represent the company’s key performance factors, as well as its most pressing risks. They should also control the level of risk engaged in by the company and verify that executives implement adequate risk management processes to mitigate the consequences of adverse events. The Board must guarantee that the company has the necessary internal controls to prevent the loss of assets, information and prestige. It must also ensure that the managers adopt an ethical behavior that falls in line with the company’s Code of Conduct in its interactions with suppliers, clients and employees. Lastly, it must verify that the employees adhere to the compulsory regulations, so as to not jeopardize the company’s assets or operations. 2. Approve and verify the organization’s strategy The Board should ensure that the CEO and the executive team fulfill their responsibility of formulating and implementing the strategy. Likewise, it should fully understand and approve the corporate strategy, approve the main decisions related to its implementation, and continuously control its execution and results. It is therefore crucial that the members of the Board know the key value drivers and the organization’s risks.

16

3. Approve the principal financial decisions The Board of Directors guarantees the effective and efficient use of the financial resources to achieve the company’s strategic objectives. This includes the approval of annual operative and capital expenditure budgets and the authorization for large investments, new loans or reimbursements as well as acquisitions and fusions. 4. Select and evaluate the top-tier executive The members of the Board select the CEO and determine his or her salary. They also approve the recruitment of other executive team members, such as the CFO and the COO. Once a year the Board evaluates the CEO and executive team’s performance and revises their salary as seen fit. 5. Provide advice and support to the CEO Board members share their expertise, knowledge and recommendations when the executive team describes the strategic opportunities and important decisions at hand. Limited time, limited information To fulfill their multiple responsibilities, Board members must have a vast knowledge of the company; they must understand its financial outcomes and the competitive position it holds, as well as its clients, new product launches and its workforce’s skills and capabilities. Therefore, companies must find a way to optimize the information that the Board receives and must evaluate previous to the meetings, as well as the information presented during these. A corporate governance system developed around the Balanced Scorecard helps the Board face two of its most pressing challenges: limited time and limited information. The Balanced Scorecard and the Corporate Governance Process Nowadays many companies use three levels of scorecards as the basis for their corporate governance system. 1. The Organizational Scoreboard The process commences with the organizational scoreboard. The Board approves the firm’s strategy map, strategic objectives and indicators, as well as the targets and incentives linked to their performance. The main objective of the organizational scoreboard is to help the CEO communicate and implement the corporate strategy throughout the organization. This scoreboard plays a central role in the governance process as it provides board members with the financial and non-financial information they need to supervise the organization’s performance. Through it, the Board can access updated information about important trend indicators, such as consumer feedback on value attributes and changes in market share. 2. The Executive Team’s Personal Scoreboards The second components of the corporate governance system are the executive team members’ individual scoreboards. These scoreboards describe the strategic contributions of key employees. They help the CEO and the Board separates their expectations of executive performance from their expectations of the company’s performance as a whole. Also, the Board of Directors and the Compensation Committee may use these to select, evaluate and remunerate top-tier executives.

17

To develop them, the CEO and the executive team reach an agreement about the organizational objectives that will become each team member’s main responsibility, and then use these objectives to shape the individual scoreboards. By aligning these scoreboards to the strategy, the Board has access to an explicit mechanism by which to evaluate their performance, and therefore, calculate their compensations based on objective indicators. 3. The Board of Directors’ Scoreboard Implementing this scoreboard has the next benefits: - It defines the Board’s strategic contributions - It provides a tool to manage the Board’s structure and performance - It clarifies the strategic information and inputs required by the Board This scoreboard uses a stakeholder perspective which reflects the Board’s responsibilities with regards to investors, regulatory bodies and the community. These responsibilities include: - Approving the plan, verifying the organization’s performance and defining high-level performance objectives for the organization. - Evaluate and strengthen executive performance. - Guarantee the organization’s compliance to regulations, laws and community standards, as well as the adequate use of internal control mechanisms. The Board ensures that managers are providing shareholders with valuable information and that executives are using shareholder capital to pursue the long-term interests of the latter. Therefore, the Internal Process perspective contains the objectives that will allow board members to fulfill shareholder and stakeholder expectations. They should be divided into three main strategic themes: Performance Supervision, Executive Performance, and Compliance, Communication and Corporate Responsibility. Better Understanding, More Responsibility This approach provides the information and necessary structures to enable the Board to fulfill its responsibilities more effectively. At the same time, the transparency conveyed by these scorecards endorses the Board’s responsibilities. The organizational Balanced Scorecard informs the Board of the strategies the organization intends to implement. The executive’s individual scoreboards provide a clear base to monitor the management team’s performance, compensate them based on compliance to strategic targets and evaluate the executives’ career and succession plans. Lastly, the Board’s scoreboard informs all its members of their responsibilities and facilitates the periodic evaluation of their performance, based on clearly defined and comprehended criteria. Linking Balanced Scorecard Measures to Strategy: Three principles that enable an organization’s Balanced Scorecard to be linked to it’s strategy.

1. Cause and effect relationships 2. Performance drivers 3. Linkage to financials

18

Cause and effect relationships: A strategy is set of hypothesis about cause and effect. Cause and effect relationships can be expressed by sequence of if-then statements. For example, a link between improved sales training of employees and higher profits can be established through the following sequence of Hypothesis: If we increase employee training about products, then they will become more knowledgeable about full range of products they can sell. If employees are more knowledgeable about products, then their sales effectiveness will improve. If their sales effectiveness improves, then the average margins of the products they sell will increase. A properly constructed scorecard should tell the story of the business unit’s strategy through such a sequence of cause and effect relationships. The measurement system should make the relation ship (hypotheses) among objectives in the various perspectives explicit so that they can be managed and validated. Is should identify and make explicit the sequence of hypotheses about the cause and effect relationship between outcome measures and performance drivers of these outcomes. Every measure selected for Balanced scorecard shall be an element of chain of cause and effect analysis that communicates the meaning of business unit’s strategy to the Organization. Outcomes and Performance Drivers The Balanced Scorecard use certain generic measures. Theses Generic measures tend to be core outcome measures, which reflect the common goal of many strategies, as well as similar structure across industries and companies. These Generic outcome measures tend to be lag indicators, such as profitability, market share, customer satisfaction, customer retention and employee skills. The performance drivers, the lead indicators are the ones that tend to be unique for a particular business unit. The performance drivers reflect the uniqueness of the business unit’s strategy, for example the financial drivers of profitability, the market segments in which unit chose to compete and particular internal process and learning and growth objectives that will deliver the value propositions to the targeted customers and market segments. A good Balanced Scorecard should have mix of outcome measures and performance drivers. Outcome measures without performance drivers do not communicate how the outcomes are to be achieved. They also do not provide about the early indication about the strategy being implemented successfully. Conversely Performance drivers such as Cycle times and parts per million defect rates without outcome measures may enable business unit to achieve the short term operational improvements but will fail to reveal whether the operational improvements have been translated in to expand business with existing and new customers, and to eventually enhance financial performance. A good Balanced Scorecard should have an appropriate mix of outcomes ( lagging indicators) and performance drivers( leading indicators) that have been customized to the business unit’s strategy.

19

Linkage to Financials A Balanced Scorecard must retain a strong emphasis on outcomes, especially on financial one like return on capital employed or economic value added. Many managers fail to link programs such as Total Quality Management, cycle time reduction, reengineering and employment empowerment to outcomes that directly influence customers an directly deliver performance. In such organizations, the improvement programs have incorrectly taken as the ultimate objective. They have not been linked to specific targets for improving customer and eventually financial performance. The inevitable result is that such organizations eventually become disillusioned about the lack of tangible payoffs from their change programs. Ultimately, causal paths from all the measures on a scorecard should be linked to financial objectives.

20

5.0 Impact of using BSC by Independent Directors on Organization

Implications of Independent directors a) The role of the director is more than advisory. b) The position of the director comes with certain risks that did not exist until recently. c) Being a friend of the chairperson of co-directors is an insufficient reason for being on the board. d) It is not possible to be a member of too many boards. In fact it would be rather against one’s reputation to be in too many boards. There are human limitations on what one person can possibly do. e) It is important to jell with other members of the board and create a professional yet collegial group working together for clarifying, understanding and achieving the vision of the company. What these mean is that the board has to team up with the executive and create better results for stakeholders. It will also require that the board manages itself in more thorough ways using appropriate tools. Impact of Balanced Scorecard Creating a Balanced Scorecard for the Boards of Directors The recent catastrophic corporate governance failures at Enron, Tyco, WorldCom, Parmalat and other entities triggered an equally cataclysmic collapse in the confidence that shareholders, and wider stakeholders, held in our organizations. People simply stopped believing what companies told them. A major analysis of poor performing firms for a report in 2004 found that in just 13% of cases shareholder value destruction was a result of compliance failure. Fully 60% was attributed to strategic mistakes such as misjudging customer demand or competitive pressure. The remaining failures were the result of operational blunders (2). The message is clear. Although oversight of the compliance with accounting and other financial rules and regulation is a key responsibility of the stewards of our corporations (the Board of Directors), to properly dispatch their duties they must pay even more attention to assessing the likelihood of strategic failure. Align the Board of Directors The third of Kaplan and Norton’s five principles of the Strategy-Focused Organization (align the organization to the strategy) has as a sub-component: align board of directors. Doing this effectively requires the creation of a Balanced Scorecard for the Board of Directors that complements that of the Enterprise.

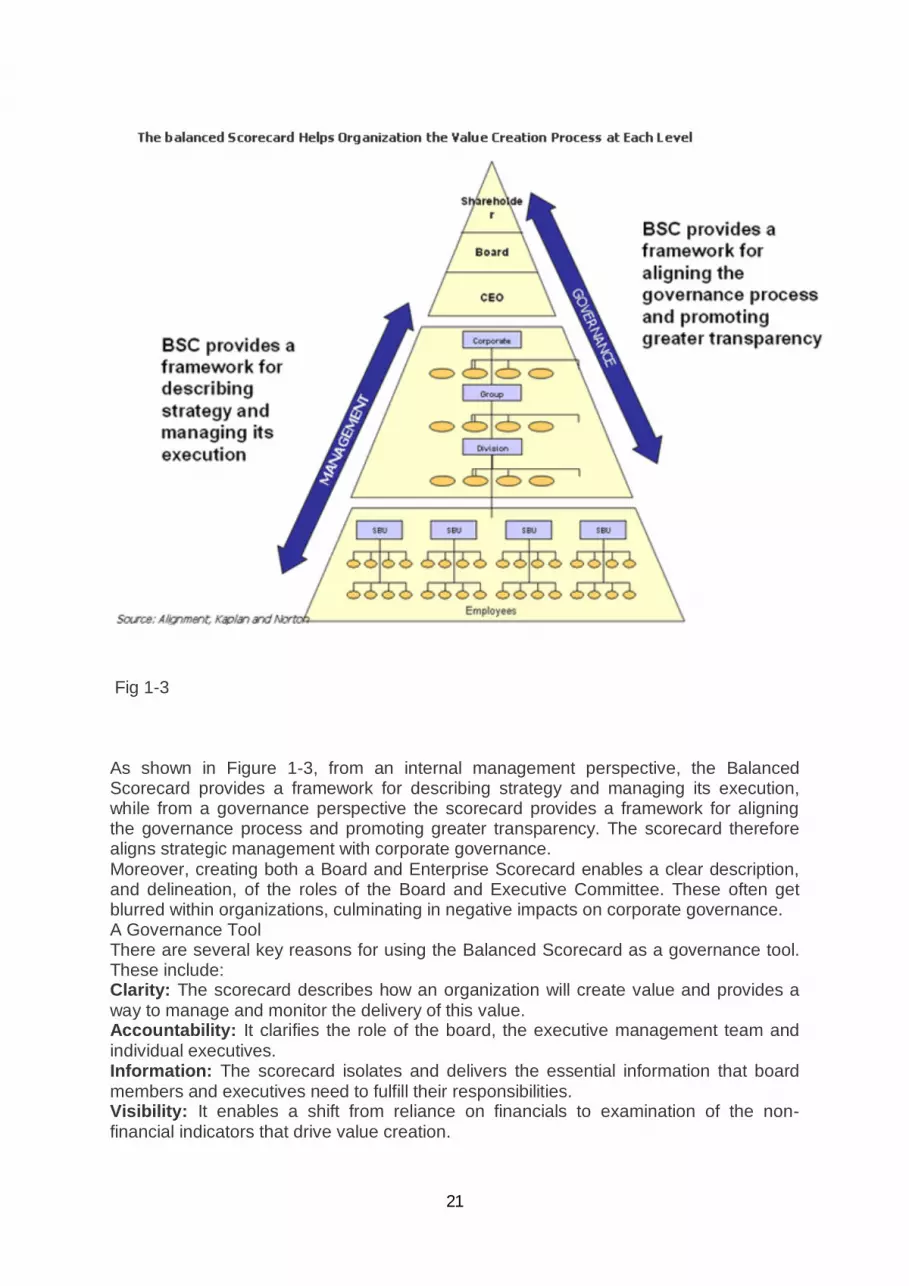

21

Fig 1-3 As shown in Figure 1-3, from an internal management perspective, the Balanced Scorecard provides a framework for describing strategy and managing its execution, while from a governance perspective the scorecard provides a framework for aligning the governance process and promoting greater transparency. The scorecard therefore aligns strategic management with corporate governance. Moreover, creating both a Board and Enterprise Scorecard enables a clear description, and delineation, of the roles of the Board and Executive Committee. These often get blurred within organizations, culminating in negative impacts on corporate governance. A Governance Tool There are several key reasons for using the Balanced Scorecard as a governance tool. These include: Clarity: The scorecard describes how an organization will create value and provides a way to manage and monitor the delivery of this value. Accountability: It clarifies the role of the board, the executive management team and individual executives. Information: The scorecard isolates and delivers the essential information that board members and executives need to fulfill their responsibilities. Visibility: It enables a shift from reliance on financials to examination of the non-financial indicators that drive value creation.

22

Composition: The scorecard provides a way to clarify the strategic skills required by the board. Compensation: It provides a way to clarify and assess the strategic contributions of an executive. A Board Scorecard System Note that when we speak of a Board Balanced Scorecard it has to be understood within the context of the Board Scorecard System, which has three mutually reinforcing components. 1. The Enterprise Scorecard. 2. The Board Scorecard. 3. The Executive Scorecard. The Enterprise Scorecard The Enterprise Scorecard is the corporate scorecard, which describes how value will be created for shareholders. Indeed if executive management teams just use the Enterprise Strategy Map and Balanced Scorecard to communicate with their Boards (without building a Board scorecard) it will still signal a dramatic step-forward from communicating via the impenetrable board packs that are too often typically distributed - and which provide boards with a poor guide for assessing performance. The Board Scorecard The Board Strategy Map clarifies how the Board contributes to the success of the corporation. The financial perspectives on the Board and Enterprise scorecards will be identical, as both share the same vision of creating value for shareholders. However, rather than use a traditional customer perspective, a Board scorecard introduced a stakeholder perspective, reflecting the board’s responsibilities to investors, regulators and communities. As a generic example, these can be translated into the stakeholder objectives of ‘approve, plan and monitor corporate performance’, ‘strengthen and motivate executive performance’ and ‘ensure corporate compliance’. Each of these three objectives then becomes discrete themes within the Board’s internal perspective. For instance the performance oversight theme will include an objective such as ‘approve strategy and oversee its execution’. Within the learning and growth perspective, the board will be ensuring that it has the skills, knowledge and information systems in place for it to judiciously dispatch its duties. A typical objective might be ‘ensure board skills and knowledge match the strategic direction.’ The corporate Balanced Scorecard significantly enhances the board’s oversight capacity by providing a revealing glimpse into the strategy execution efforts of the company, but today’s directors, facing unprecedented pressure to adhere to leading-edge governance standards, require a tool to assess their own performance as well. Enter the board Balanced Scorecard, a tool in the arsenal of pioneering boards that wish to maximize their contribution to corporate performance and sustain the ability to add value in the years to come through the identification and evaluation of key performance measures utilizing the proven Scorecard framework. As a first step in the board Scorecard process, a Strategy Map of objectives, such as the generic example in Exhibit 1-4, should be constructed. Let’s work through the four perspectives of this map, outlining the considerations that must be made when selecting objectives.

23

There is an assumption that, if the board capably performs its required tasks, those efforts will contribute to the corporation’s ability to achieve financial success. Therefore, the Financial objectives comprising the board Strategy Map should be drawn directly from the organization’s corporate Strategy Map. These objectives normally include an overarching objective relating to shareholder value as well as ones that outline how the organization will achieve the dual objectives of increasing productivity (through cost reductions and improved asset utilization) and growing revenue (from selling new products or deepening relationships with existing customers). For this map, the Customer perspective has been renamed Stakeholder, in recognition of the many groups that have a stake in the performance of the board. Thus, the initial task in crafting objectives for this perspective is determining the stakeholder groups that must be satisfied as the board works to fulfill its obligations. From the objectives appearing in Exhibit 1-4, we might infer that this board has chosen shareholders and employees as the critical stakeholder groups. “Ensure compliance and accountability” will allow stockholders to sleep a little easier, secure in the knowledge that the board has their best interests at heart. While not explicitly stated, society at large will also benefit from this objective, avoiding the high costs of litigation, productivity declines, and unemployment that frequently result from corporate shenanigans. Shareholders will also be pleased to see that the board will “[a]pprove strategy and monitor corporate performance.” Finally, all employees will benefit from the board[s] that “[c]ounsel[s] CEO and monitor[s] executive performance.”The Internal Processes objectives articulate how the outcomes in the Stakeholder perspective will be achieved through efficient and effective board processes. In order to achieve compliance and accountability as shown in the Stakeholder perspective, this board must ensure compliance with all laws and regulations, make certain the company has effective internal controls, and diligently work to improve disclosure practices, improving transparency and visibility into the firm’s operations. Stakeholders also demand that the board approve strategy and monitor corporate performance; thus internal processes must be developed to achieve this significant undertaking. In this example, the board will monitor performance using the company’s corporate Balanced Scorecard, approve funding for and monitor strategic initiatives to ensure that spending is aligned withstrategy, and, finally, optimize its own functions, such as board structure and procedures in an effort to ensure they function as efficiently as possible. A major endeavor of any board is counseling the CEO and monitoring executive performance. This board will attempt to achieve that objective by first ensuring it has a firm grasp on the company’s industry and underlying economic and political environment. Evaluating and rewarding executive performance and monitoring succession planning ensure that successful executives are rewarded for a job well done and a pipeline of future leaders is waiting in the wings.

24

Fig 1-4

25

A well-constructed Learning and Growth perspective must contain objectives focused on three separate but integrated dimensions of capital: human, information, and organizational. Under the mantle of human capital, the board represented in Exhibit 1-4 will work to ensure skills align with the firm’s strategic direction. Board members must possess the requisite financial literacy and business acumen to contribute meaningfully in their capacity. Regarding information capital, the board must press the company to provide access to strategic information, so members can provide insight and effectively monitor corporate performance. Finally, it is vital for the board to approach work with a spirit of advocacy and inquiry. Some governance experts have suggested that board members don’t behave effectively in meetings if they are unwilling to raise important issues and challenge the CEO on the firm’s current performance and strategic direction. Boards must rise to this challenge by balancing the seemingly competing demands of advocating on behalf of the firm, acting as its tireless champion, while also serving the needs and preserving the trust and confidence of stakeholders by encouraging robust dialog on challenging and potentially controversial issues. The Strategy Map paints a compelling picture of the board’s endeavors, but to track performance day in and day out, the board must translate the objectives into performance measures and targets. Strategic initiatives— the projects relied on to achieve targets—must also be brainstormed, funded, and monitored for effective performance. And what are the payoffs awaiting boards proactive enough to make this leap of faith into the Balanced Scorecard world? For starters, board operations will become much more effective and efficient as board members glean new insights into their core activities and gain the ingredients they need to divert attention from the perfunctory reviews of the past toward the dialog that will ignite the opportunities of the future. Stakeholders will undoubtedly applaud this intrepid move as well, since the board’s Balanced Scorecard will highlight members’ public commitments to safeguard stakeholder investments. This transparency and enhanced visibility not only ensures improved board functioning, but may have positive financial ramifications for the company.

Committee Scorecard Further, given that Boards of Directors typically disaggregate into committees, themes can also be managed separately with ownership assigned. Executive Scorecard The final aspect of the Board Scorecard System is the Executive Scorecard. This describes the strategic contributions of each of the executive committee (including the CEO) and is drawn from the objectives within the Enterprise Scorecard, thus ensuring that the executive will take responsibility for the Enterprise level strategic objectives. The Executive Scorecard becomes the performance contract between the executive and the Board and is used to evaluate and reward senior executive performance. Moreover, an Executive Scorecard essentially serves as a job description for a senior role and so is equally valuable for selection, or succession planning purposes. There is little doubt that corporate governance will continue as a core organizational priority for many years to come. The potential for financial fraud, coupled with the greater danger of strategic failure in today’s fast-moving markets, will lead to even more vocal demands for performance transparency, responsibility and accountability within, and deep inside, our organizations. Promising performance visibility and line of sight from the

26

boardroom to the front-line, the Balanced Scorecard is well placed to serve this organizational requirement. Effective scorecard design The process of understanding the business model and identifying both performance drivers and appropriate measures is complex. There is often confusion, for instance, around assumed logical, rather than actual, causal relationships between drivers of performance and hence performance measures. It may seem logical to assume causality between reported customer-service satisfaction levels and financial results. However, the two are not necessarily congruent: customer-service satisfaction levels within the budget airline industry may be significantly lower than those of full-service carriers, although the comparative financial performance of the former is markedly better. To be predictive, rather than simply backward looking, the Balanced scorecard approach should focus on those activities and processes that an organisation needs to get right to ensure it fulfils its strategy. The significance of this task cannot be underestimated. The lack of a cause and effect relationship between drivers of performance and indicators, perhaps from invalid assumptions of the business model, will lead to adverse organisational behaviour and performance To summarise, the Kaplan and Norton view is that strategy scorecards: ● Provide a logical and comprehensive way to describe strategy; ● Communicate clearly the organisation’s desired outcomes and its hypotheses about how these outcomes can be achieved; and ● Enable all organisational units to understand the strategy and identify how they can contribute by becoming aligned to the strategy. Getting the ‘Balanced’ right, The correct ‘Balanced’ that a scorecard encompasses should be driven by – and reflect – the value proposition (product leadership, customer intimacy or operational excellence) on which the strategy is based. To be most effective, Scorecards of ‘customer intimates’ should emphasise measures in the customer perspective; product leaders should emphasise those in the innovation and growth perspective; and those pursuing technical excellence should focus more on the internal business-processes perspective. Olson and Slater (2002) have tested this approach. Their research findings showed that ‘superior’ performance can indeed be facilitated by manipulation of performance emphasis, i.e. scorecard design, irrespective of: ● The value proposition on which the strategy is based; and ● The characteristics exhibited in addressing the product/market strategy decisions. Of all the firms participating in Olson and Slater’s study, irrespective of their product/market response position,‘higher performers’ placed greater emphasis on measures included in the financial perspective than did lower performers. Interestingly, for operators classified as ‘low-cost defenders’ those that performed better placed less emphasis on customer-related performance measures than did the lower performers. Recent research suggests that the way forward for managers, is to focus explicitly on how goals, strategies and operations are connected, and to try to understand the interdependencies across the value chain. Chenhall categorised an index of integration over a number of dimensions including:

27

● Operations/strategy: integrated operational actions with organisational strategies; ● Different internal units: integrated objectives of different business units within the organisation; ● Internal/external: make transparent the interrelationships between the activities of different business units and external suppliers and customers; ● Financial/non-financial: provide information on financial, customer-related, business-process related, and long-term innovation related performance; and ● Time: integrate current actions with past and future consequences by using leading and lag indicators. If we accept that organisations create value through their superior co-ordination and integration, identifying what it is exactly that a Balanced scorecard integrates seems very useful. What matters most for the individual company, however, is on which dimension of integration to concentrate. Manufacturers that compete on product quality might, for example, emphasise the integration of internal and external units. Their Balanced scorecards would need to highlight measures of co-operative product design, speed and reliability of deliveries and logistics efficiencies, for example. By contrast, organisations in a strategic turnaround situation might need to emphasise the integration between the operations in local units with overall corporate strategy. Performance measurement systems can support such change programmes by highlighting the extent of integration between operations and strategy. The bottom line is that a good scorecard will reveal an organisation’s strategy and paint a picture that the traditional focus on financial measures is unable to do 5.1 Achieving Strategic Alignment The first process in Building the Balanced Scorecard—translating the vision—helps managers build a consensus around the organization’s vision and strategy. Despite the best intentions of those at the top, lofty statements about becoming “best in class,” “the number one supplier,” or an “empowered organization” don’t translate easily into operational terms that provide useful guides to action at the local level. For people to act on the words in vision and strategy statements, those statements must be expressed as an integrated set of objectives and measures, agreed upon by all senior executives, that describe the long-term drivers of success. The second process—communicating and linking—lets managers communicate their strategy up and down the organization and link it to departmental and individual objectives. Traditionally, departments are evaluated by their financial performance, and individual incentives are tied to short-term financial goals. The scorecard gives managers a way of ensuring that all levels of the organization understand the long-term strategy and that both departmental and individual objectives are aligned with it.

28

The third process—business planning—enables companies to integrate their business and financial plans. Almost all organizations today are implementing a variety of change programs, each with its own champions, gurus, and consultants, and each competing for senior executives’ time, energy, and resources. Managers find it difficult to integrate those diverse initiatives to achieve their strategic goals—a situation that leads to frequent disappointments with the programs’ results. But when managers use the ambitious goals set for Balanced scorecard measures as the basis for allocating resources and setting priorities, they can undertake and coordinate only those initiatives that move them toward their long-term strategic objectives The fourth process—feedback and learning—gives companies the capacity for what we call strategic learning. Existing feedback and review processes focus on whether the company, its departments, or its individual employees have met their budgeted financial goals. With the Balanced scorecard at the centre of its management systems, a company can monitor short-term results from the three additional perspectives—customers, internal business processes, and learning and growth—and evaluate strategy in the light of recent performance. The scorecard thus enables companies to modify strategies to reflect real-time learning. The process of building a Balanced scorecard—clarifying the strategic objectives and then identifying the few critical drivers—also creates a framework for managing an organization’s various change programs. These initiatives—reengineering, employee empowerment, time-based management, and total quality management, among others—promise to deliver results but also compete with one another for scarce resources, including the scarcest resource of all: senior managers’ time and attention.

29

Make strategy a continual process – strategy management meetings and the learning process As operating conditions change continuously, so must the business strategy, and hence a process for strategy management is required. Successful Balanced scorecard companies implement a process for strategy management, which integrates the management of tactics, and the management of strategy into a seamless and continual process. In these organisations, the role of the budget may change. Budgets can be an inflexible tool for managing operations, however few organisations have any tool at all for managing strategic progress. For organisations using a Balanced Scorecard, this may be used as the link between operations and strategy. In managing and controlling operations, the budget defines both resources allocated to business unit operations, and the associated performance targets. Three themes emerge in the implementation of a learning process. First, strategy is linked to the budgeting process, and spending decisions are analysed for their strategic impact. Such analysis has lead some companies to operate two kinds of budget: ● An operational budget which functions as a management tool to guide the day-to-day expenditure necessary to run the business; and ● A strategic budget which protects long-term strategic initiatives from the pressures of short-term The second behavioural change to accompany the strategic management process is the introduction of management meetings to review strategy and facilitate wider involvement in scorecard issues. Some companies have taken this information-sharing initiative as far as open reporting, so that performance results are available to everyone in the organisation. Finally, in taking steps to make strategy a continual learning process, the Balanced scorecard is based on the cause and effect linkages between individual/departmental /business units actions. Once the scorecard is put into action, and feedback processes report progress, the hypotheses on which such cause and effect linkages are based can be tested, either statistically or qualitatively. The scorecard operates by monitoring and measuring actions and the impact that they have, and by allowing managers to manage assets used to deliver value to identified stakeholders. An effective scorecard design must therefore reflect the contribution of these assets by generating appropriate performance indicators. If the strategy is inappropriate or invalidated due to changing market conditions, a Balanced scorecard approach, if implemented in the right way, should allow for organisational learning. This means that the inherent performance measurement system is providing appropriate information to help management to challenge its existing assumptions of the business model. Strategy management meetings The agendas of business management meetings are concerned, generally, with the reporting and control of the organisation’s operational activity. Although this is necessary, it is unlikely to be sufficient to secure the performance improvements often promised by implementation of the ’strategic’ Balanced scorecard. Strategy management meetings, focusing directly on the impact and effective implementation of the strategy itself, should align with the new ‘strategy focused’ culture that Kaplan and Norton espouse. They should focus on strategic issues, and the value of teamwork and organisational strategic learning, to improve the management of strategy, rather than operational tactics.

30

Where the practice of reporting by exception is adopted, the Balanced scorecard can function as a useful agenda for strategic management meetings. Managers’ time is limited and using the scorecard to focus attention on those activities where targets are not being met, is a time-efficient way of steering and managing strategy implementation. To be fully effective, the meetings require honest feedback, commitment, and a culture of supportive teamwork. The Balanced scorecard’s role in fostering a common view of the business model should help this. Organisations also need to ensure that their strategies are still valid. Continuous learning enables management to scrutinise the fundamental assumptions on which strategy is to be founded. However, this approach is not a tool that should be used in isolation to facilitate ‘out-of-the box’ thinking. Other approaches, such as scenario planning, can be used effectively to identify the possible drivers of change in the industry and the wider macro environment. Basic management tools, such as reports of actual performance against budgeted performance, and variance analysis, are useful for the management and control of strategy implementation, and may help executives to determine a course of action that will help the organisation to get back on track. However, traditionally, these tools use only financial metrics, and, more importantly, do not challenge existing assumptions about the performance measure, target, and current strategy for achieving the target. Even where a culture of teamwork and problem solving is fostered, the value of a ‘single-loop’ control system, which operates only within the context of the existing strategy, is obviously limited. By using a Balanced scorecard as the agenda for strategy management meetings, and exceptional reporting, investigation and remedying of anomalous performance results, the underlying causal links and ultimately the validity of current strategy can be considered. Some commentators argue that a strategic management system is a communication rather than control system. Its concerns are not with absolute accuracy of reams of financial data, but with clear, concise and readily understood information about progress towards the achievement of strategy-related targets and strategic projects and initiatives.

6.0 Contributing Factors The Contributing factors towards building the effective Balanced Scorecards are:

1) Balanced scorecard is most successful when it is used to drive the process of change

2) Organizations Mission 3) Organization vision 4) Strategy for implementations 5) Objective’s identified towards the mission 6) Finanical Parameters fixed as per the vision 7) Key performance indicators identified against each objective 8) Linking the four perspectives 9) The skills, competency and knowledge of the board 10) Access to information to about organization strategy 11) productive board meetings that feature discussions, and interactions among

board members and with the executive leadership team

31

Fig 1-5

32

Barriers in Balanced scorecard implementation Why Balanced scorecards sometimes fail Undoubtedly some organisations have been less than successful in using a Balanced scorecard. The reasons why can be explained by the results of several surveys, which show that: ● 78 per cent of companies that have implemented strategic performance measurement systems do not assess rigorously the links between strategies and performance measures; ● 71 per cent have not developed a formal causal model or value-driver map; ● 50 per cent do not use non-financial measures to drive financial performance; ● 79 per cent have not attempted to validate the linkages between their non-financial measures and future financial results; and ● 77 per cent of organisations with a Balanced scorecard place little or no reliance on business models and 45 per cent found the need to quantify results to be a major implementation problem. Research by professors Christopher Ittner and David Larcker at Wharton Business School found that many companies mistake the Balanced scorecard (and other measurement frameworks such as the Performance Prism) as an off-the-shelf checklist. A lack of understanding of the nonfinancial areas of performance that might advance strategy can allow self-serving managers to choose and manipulate measures. Strategy, success or value-creation mapping is a way of facilitating agreement between managers on those non-financial performance drivers that have the greatest impact on the financial outcome. The research by Ittner and Larcker (2003) highlighted the difficulties that most companies have in trying to achieve this, with fewer than 30 per cent of companies developing causal models. Moving to this stage requires a shift in approach to planning and performance and time to think and develop rigorous causal models and performance measures. Ittner and Larcker also found that organisations adopting a causal business model experience both high levels of managerial satisfaction and return on assets.With the potential for economic benefits dependent on getting a Balanced scorecard implementation right, it is perhaps surprising that so few managers devote time to this area. One approach that organisations may find helpful, is to formulate a ‘destination statement’, possibly even before considering the scorecard objectives, which sets out a clear idea of what the organisation is trying to achieve. From the destination statement, a menu of strategic options and the supporting ‘strategy map’ illustrating the cause and effect relationships that underpin the strategy, can be derived. For many organisations, it is advisable to separate the strategy-mapping process from the development of a scorecard. Equally, some organisations, although successful in tracking the causal relationships underpinning strategy and drafting the Balanced scorecard strategy, experience problems at the implementation stage. Some problems that organisations have experienced in using the framework and their underlying causes are considered here.

33

Transitional issues 1. Major organisational changes (for example, a merger or acquisition); The Balanced scorecard is not a ‘quick-fix’ approach to alleviate financial problems. Where large-scale, structural organisational changes are driven by the need to remedy financial difficulties, the longer-term commitment required for successful Balanced scorecard implementation may be sacrificed for the short-term hunger for apparent improvements in reported financial results. A potential problem of such short-termism is that unless organisational strategy has been considered carefully, and measures to secure and manage its implementation have been developed and deployed in the ‘new’ organisation, the strategy is unlikely to be sustainable. 2. Changes in key personnel/management team; Leadership and management commitment to the Balanced scorecard and its underlying principles determines the way it is used and its impact on performance. Existing scorecard initiatives can falter if, following a change in key personnel, new management does not explicitly continue to support its use. It is important to ensure that a change in management does not lead to a preoccupation with operational matters, rather than a continued focus on the strategic issues reflected in the high-level scorecard. Design failures 1. Confusion regarding primary performance drivers Often, financial measures carry more weight within an organisation than non-financials, but to drive through a holistic, long-term and sustainable strategic re-alignment, the needs of non-owner stakeholders (service users, service delivery partners, etc) should also be considered. This is particularly important where: ● The business is adopting a value based management (VBM) approach; ● Shareholder value maximisation is the ultimate objective; and ● The needs of non-financial stakeholders are material to the business. These requirements should be analysed explicitly and translated into scorecard measures. Because of the causality between links within and between scorecard perspectives, it is important that the ultimate impact of the metrics is understood clearly. To construct a scorecard that Balanceds all stakeholders’ requirements the following methodology may be useful: ● Establish prioritised (numerically weighted) stakeholder requirements, based on strategy-adjusted need for improvement; ● Quantitatively rank the internal processes in terms of their aggregate impact on these requirements; and ● Create appropriate metrics for the processes heading the list. Following this approach guides the scorecard team to a consensus, and provides the logic behind the scorecard which is invaluable in gaining credibility and obtaining buy-in throughout the organisation. 2. Poorly defined metrics; Metrics may be classified as either: ● Results metrics – measures seen by the process customer. These are the most useful as a management tool, and are usually what appear on the scorecard. OR ● Process metrics – internal measures that cause the results metrics. Process metrics are most useful to improvement teams and focus attention on the places where improvements will have the greatest impact. Good metrics are: ● A reliable proxy for outcomes and stakeholder satisfaction; ● Weakness or deficit-oriented (have an ideal value of zero);

34