Embed Size (px)

Citation preview

Chapter 27 Your Credit and the Law pp. 434- 447

Chapter 27

Introduction to Business, Your Credit and the Law Slide 2 of 60

Learning Objectives

After completing this chapter, you’ll be able to:

1. Explain how government protects credit rights.

2. Name federal laws that protect consumers.

continued

Chapter 27

Introduction to Business, Your Credit and the Law Slide 3 of 60

Learning Objectives

3. Identify consumers’ credit rights.

4. Describe how to handle credit problems.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 4 of 60

Key Words

usury law

Consumer Credit Protection Act

truth-in-lending disclosure

Equal Credit Opportunity Act

Fair Credit Reporting Act

Fair Credit Billing Act

continued

Chapter 27

Introduction to Business, Your Credit and the Law Slide 5 of 60

Key Words

collection agent

Fair Debt Collection Practices Act

credit counselor

consolidation loan

bankruptcy

Is it common for small business

owners to use their personal credit

cards to finance their business

operations.

A. B.

00

5

A. Yes

B. No

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

21 22 23 24 25 26 27 28 29 30

Answer: Yes. Most small business owners

prefer the ease of using their own credit cards

to finance their business operations because if

they pay the balance in full every

month, the financing is free. If they

got a bank loan for financing, the

interest starts the day they got the

loan.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 8 of 60

Equal Credit Opportunity Act

The Equal Credit

Opportunity Act says

that a credit application

can be judged only on

the basis of financial

responsibility

(CAPACITY)

Chapter 27

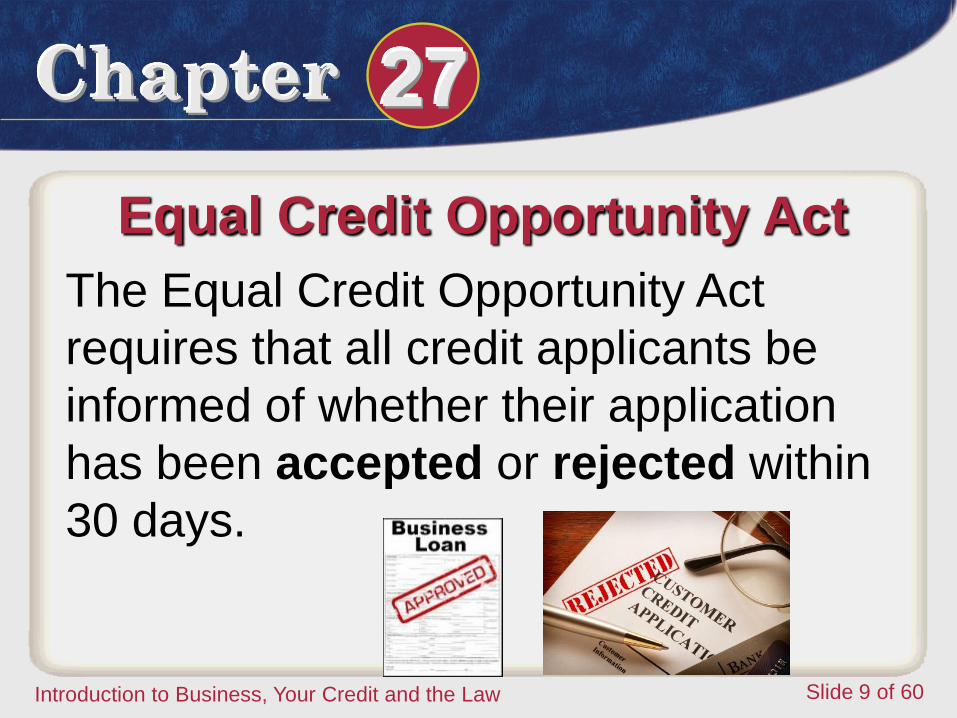

Introduction to Business, Your Credit and the Law Slide 9 of 60

Equal Credit Opportunity Act

The Equal Credit Opportunity Act

requires that all credit applicants be

informed of whether their application

has been accepted or rejected within

30 days.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 10 of 60

Equal Credit Opportunity Act

The three reasons for denying credit

are:

1. Low income

2. Large current debts

3. A poor record of making payments

in the past

A person can be denied credit if the

loan agency (bank) believes that

they are too old.

A. B.

00

5

A. Yes

B. No

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

21 22 23 24 25 26 27 28 29 30

Chapter 27

Introduction to Business, Your Credit and the Law Slide 12 of 60

Why do you need to know credit laws?

To be able to protect yourself from identity theft, and being taken advantage of in relationship to your future usage of credit.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 13 of 60

Protecting Your Credit Rights

To protect consumers the

federal and state

governments regulate the

credit industry.

Laws

Enforcement

Protecting Your Credit Rights

A. B.

00

5

A. Yes

B. No

You are in need of a loan. You go to the bank

(because you know they offer the lowest interest

rate) and fill out an application. Your loan is

approved at 45% Interest.

Can the bank legally charge you

45% interest?

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

21 22 23 24 25 26 27 28 29 30

Chapter 27

Introduction to Business, Your Credit and the Law Slide 15 of 60

Protecting Your Credit Rights

Answer: No.

A law restricting the amount of interest

that can be charged for credit is called a

usury law.

The law is different in each state.

It restricts the MAXIMUM amount

of interest that can be charged,

depending on the obligation

(house, car, personal, etc.)

Chapter 27

Introduction to Business, Your Credit and the Law Slide 16 of 60

Loan Sharking

A loan shark is a person or

body that offers unsecured

loans at a high interest rate

to individuals, often

enforcing repayment by

blackmail or threats of

violence.

I’m so confused?

How do you choose the

best credit opportunity?

A. B.

00

5

A. Go to your favorite

bank. Fill out the papers.

Get the loan.

B. Shop around. Gather

information from many

banks and choose the one

that is right for you.

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

21 22 23 24 25 26 27 28 29 30

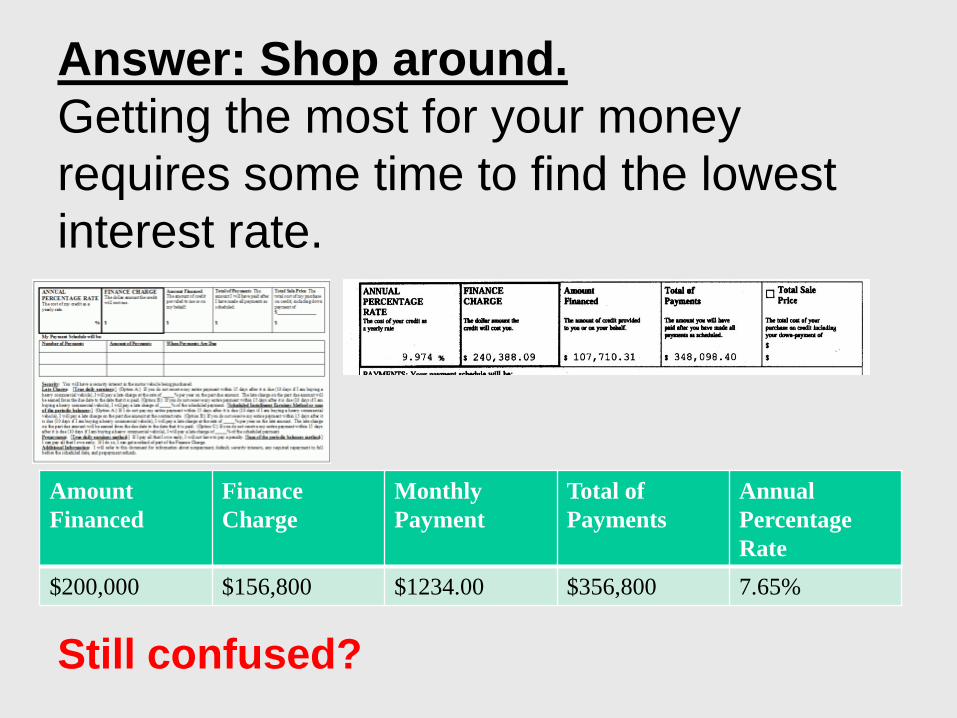

Answer: Shop around.

Getting the most for your money

requires some time to find the lowest

interest rate.

Amount

Financed

Finance

Charge

Monthly

Payment

Total of

Payments

Annual

Percentage

Rate

$200,000 $156,800 $1234.00 $356,800 7.65%

Still confused?

Chapter 27

Introduction to Business, Your Credit and the Law Slide 19 of 60

Consumer Credit Protection Act

To make comparing credit costs

easier, Congress passed the

Consumer Credit Protection

Act, also known as the Truth in

Lending Law.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 20 of 60

Truth-in-Lending Disclosure

All costs of borrowing must be made

known to the consumer.

These costs are provided in the truth-

in-lending disclosure that a creditor

gives to a borrower.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 21 of 60

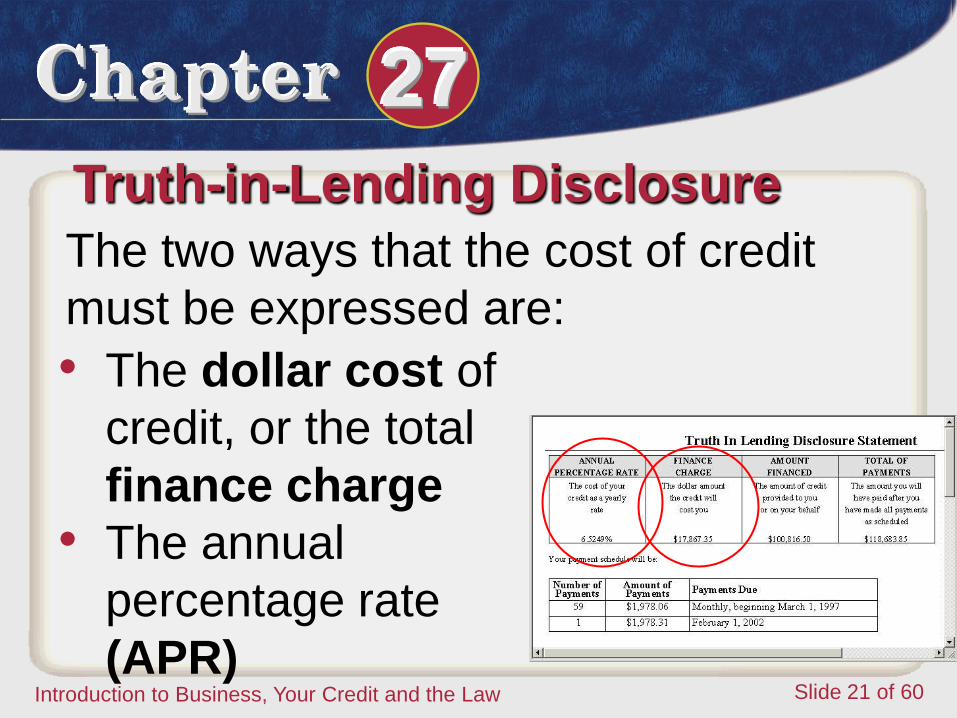

Truth-in-Lending Disclosure

The two ways that the cost of credit

must be expressed are:

• The dollar cost of

credit, or the total

finance charge

• The annual

percentage rate

(APR)

Chapter 27

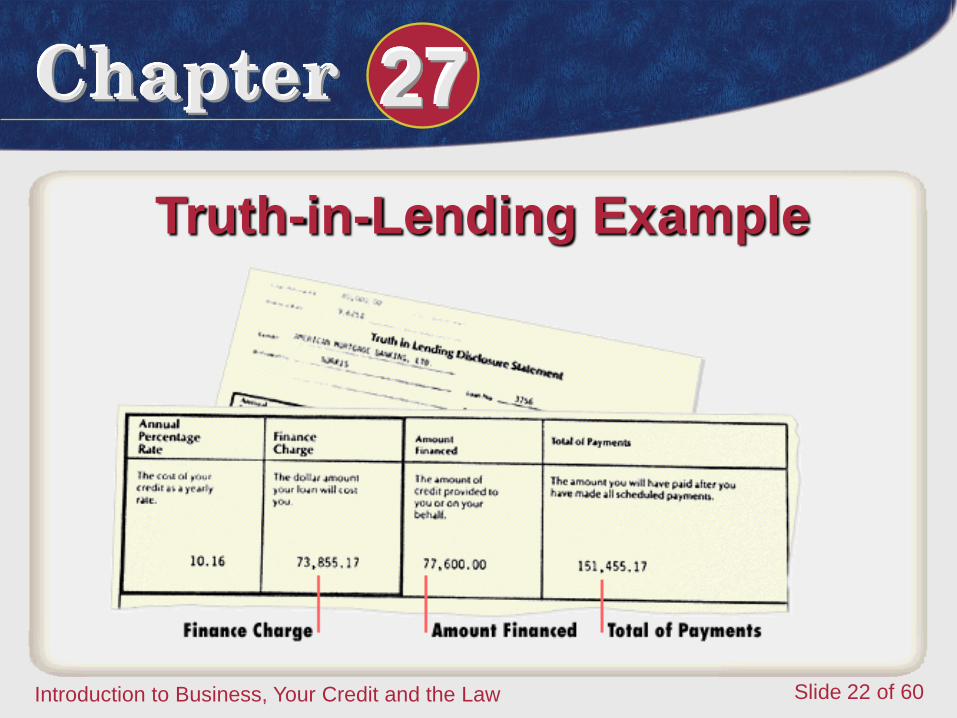

Introduction to Business, Your Credit and the Law Slide 22 of 60

Truth-in-Lending Example

Chapter 27

Introduction to Business, Your Credit and the Law Slide 23 of 60

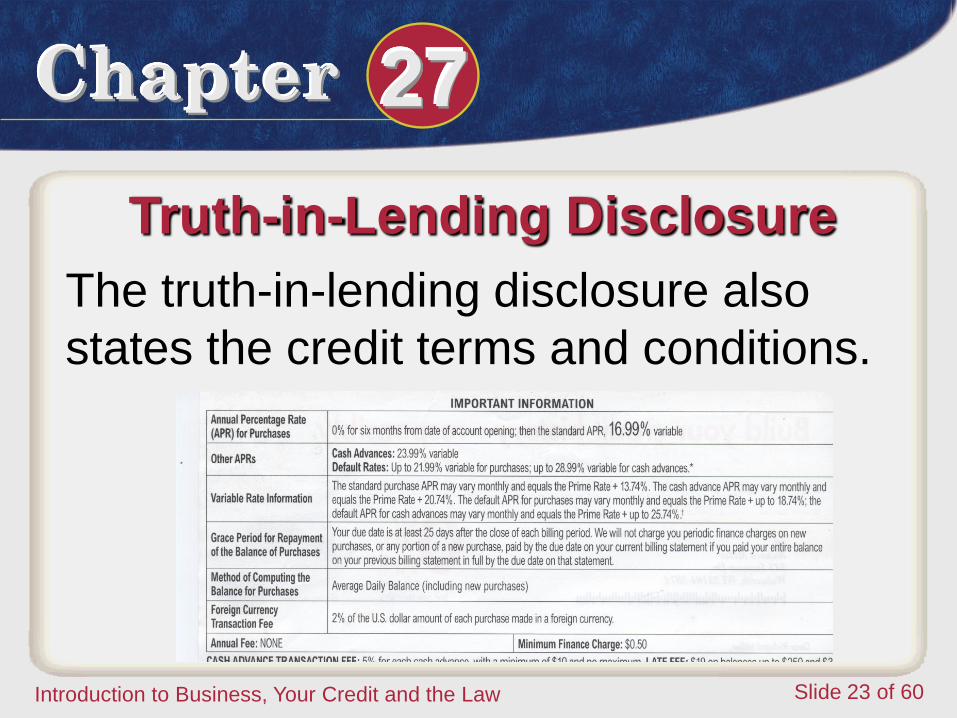

Truth-in-Lending Disclosure

The truth-in-lending disclosure also

states the credit terms and conditions.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 24 of 60

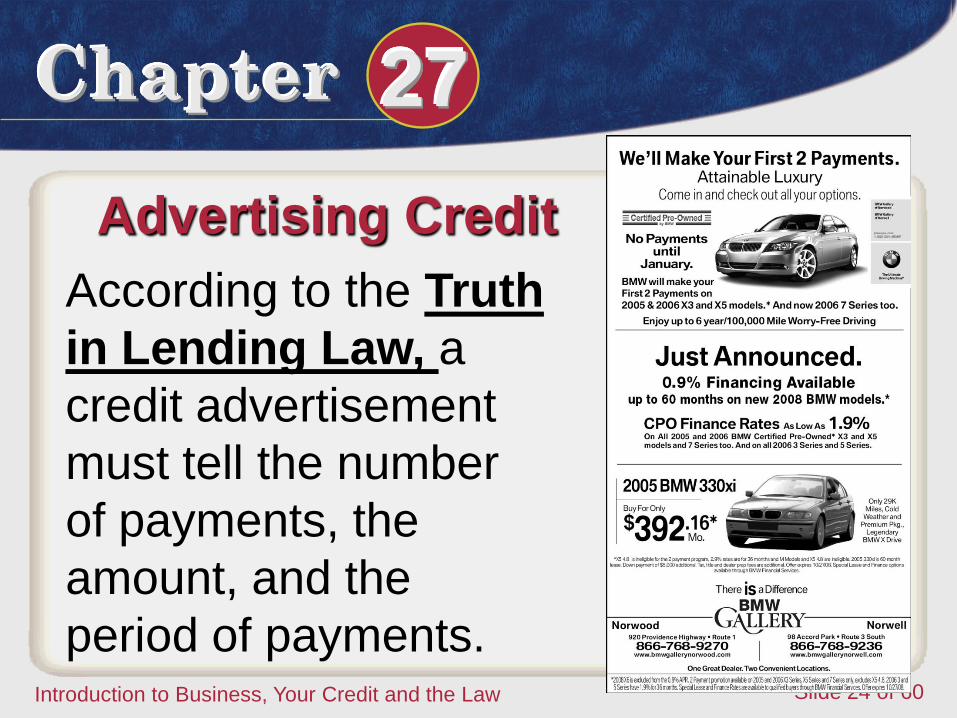

Advertising Credit

According to the Truth

in Lending Law, a

credit advertisement

must tell the number

of payments, the

amount, and the

period of payments.

You lost your credit card. A stranger found it

and is having a good time charging food and

entertainment on your credit card. He has a lot

of new friends! Do you have to pay for all of

this?

A. B.

00

5 A. Yes

B. No

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

21 22 23 24 25 26 27 28 29 30

Chapter 27

Introduction to Business, Your Credit and the Law Slide 26 of 60

Protecting Card Owners

The Truth in Lending

Law states that If your

credit card is lost or stolen

and used by someone

else, your payment for any

unauthorized purchases is

limited to $50.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 27 of 60

Protecting Card Owners

The Truth in Lending

Law also states that

credit card companies

are not allowed to

send REAL cards to

consumers who didn’t

request a credit card.

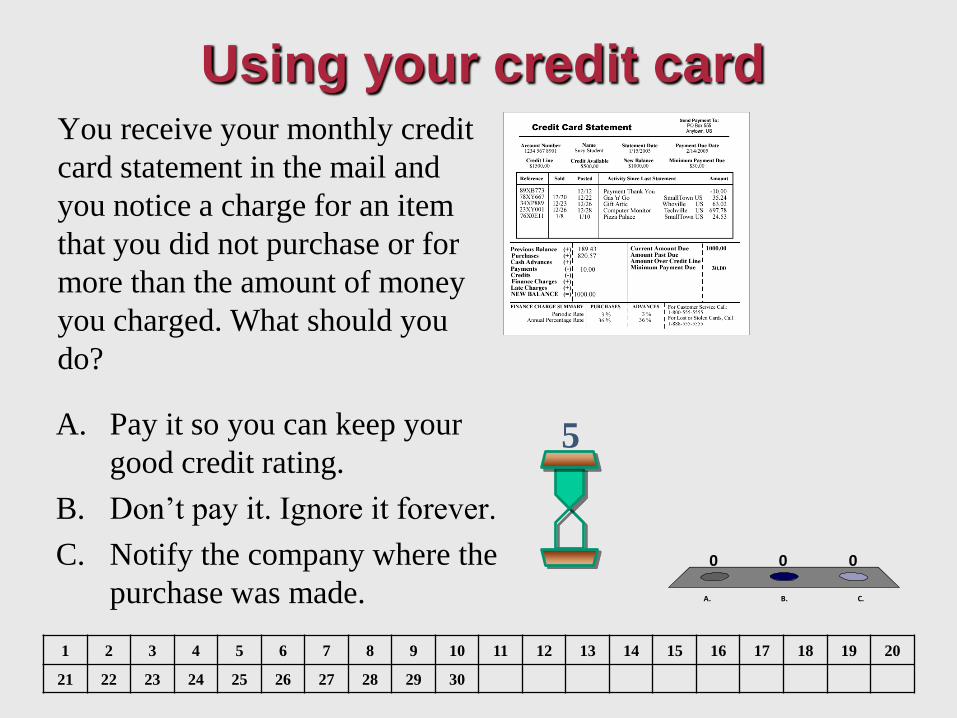

You receive your monthly credit

card statement in the mail and

you notice a charge for an item

that you did not purchase or for

more than the amount of money

you charged. What should you

do?

A. B. C.

0 00

5

Using your credit card

A. Pay it so you can keep your

good credit rating.

B. Don’t pay it. Ignore it forever.

C. Notify the company where the

purchase was made.

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

21 22 23 24 25 26 27 28 29 30

Chapter 27

Introduction to Business, Your Credit and the Law Slide 29 of 60

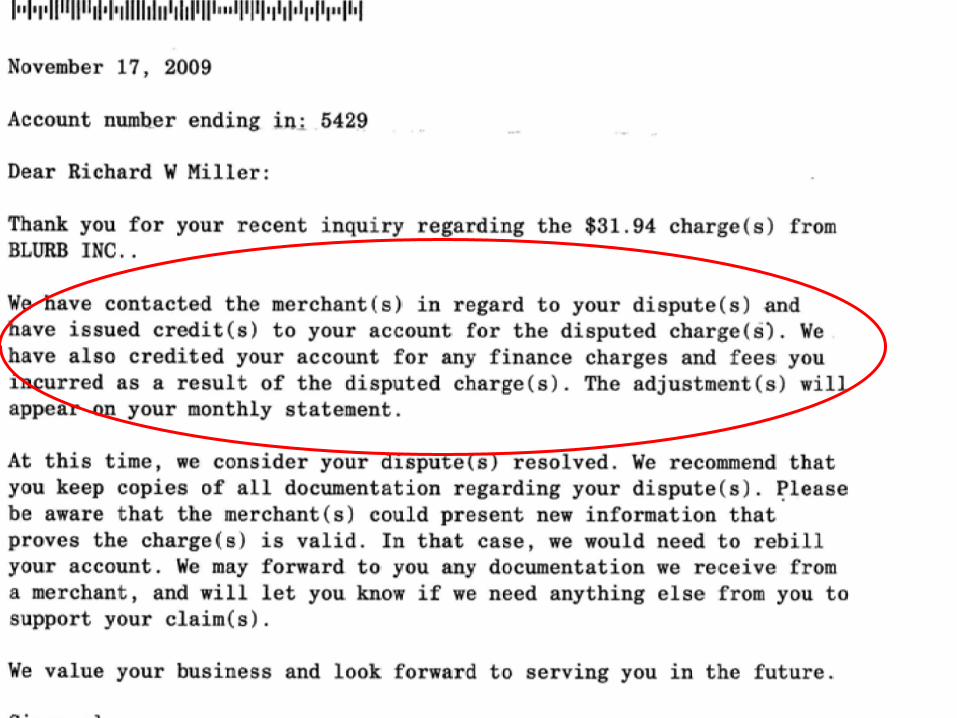

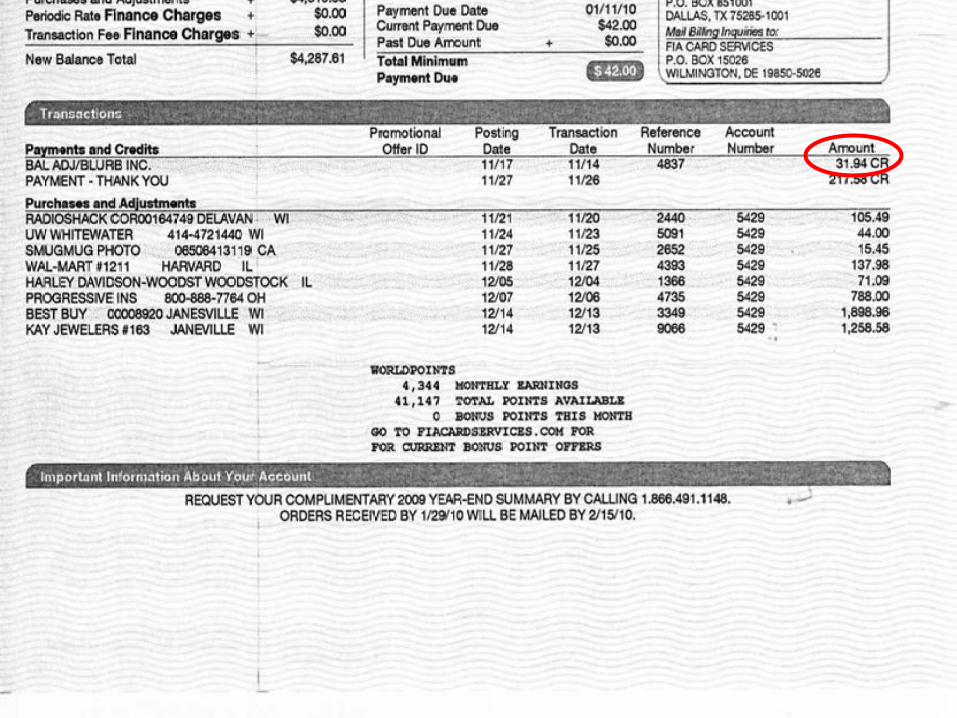

Fair Credit Billing Act

The Fair Credit Billing Act requires

creditors to correct billing mistakes

brought to their attention.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 30 of 60

The law also requires

that consumers (you) be

informed of the steps

they need to take to get

an error corrected.

Fair Credit Billing Act

Chapter 27

Introduction to Business, Your Credit and the Law Slide 31 of 60

Notify the Company Where you made or did not make a

purchase

1. The first step in fixing billing

mistakes is to inform the company

that billed you.

Phone call, e-mail, etc.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 32 of 60

Notify the Credit Card Company

2.The second step in correcting billing

errors is to notify the Credit Card

company in writing.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 33 of 60

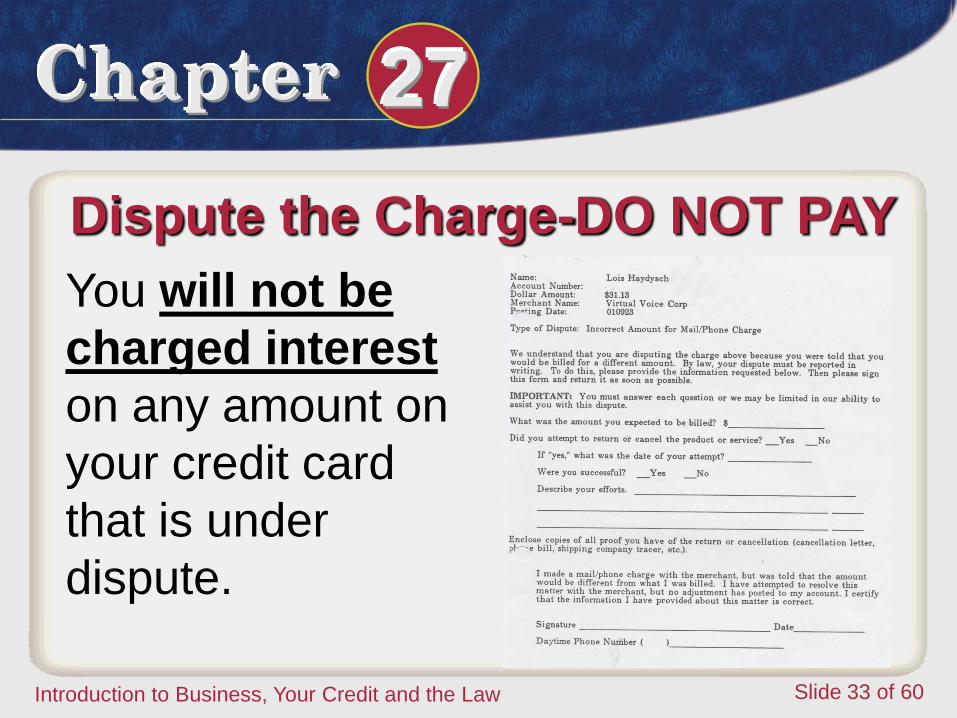

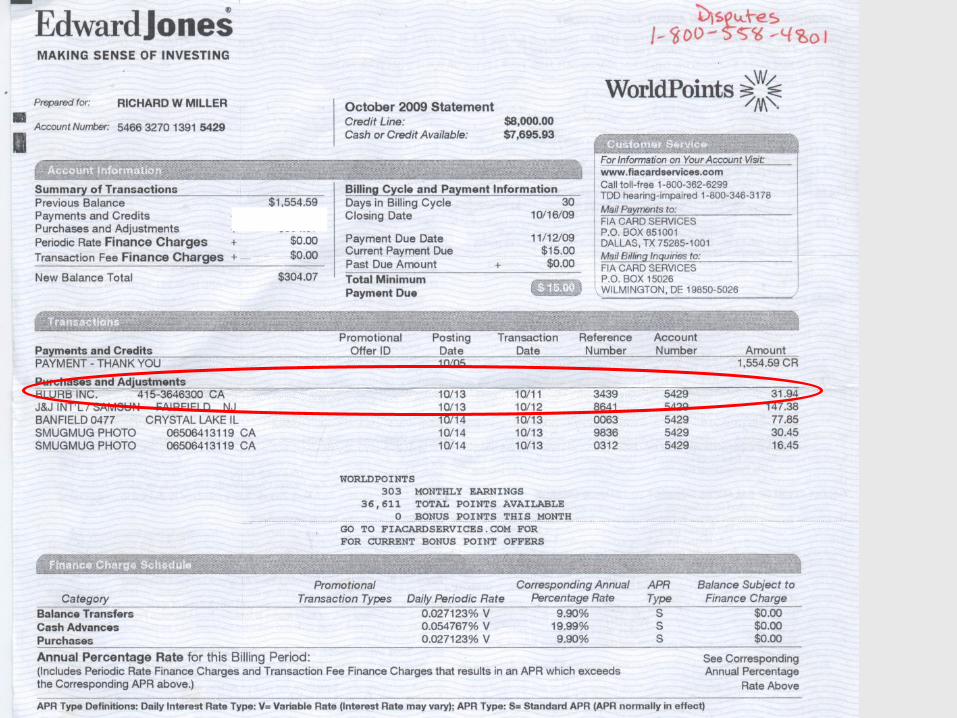

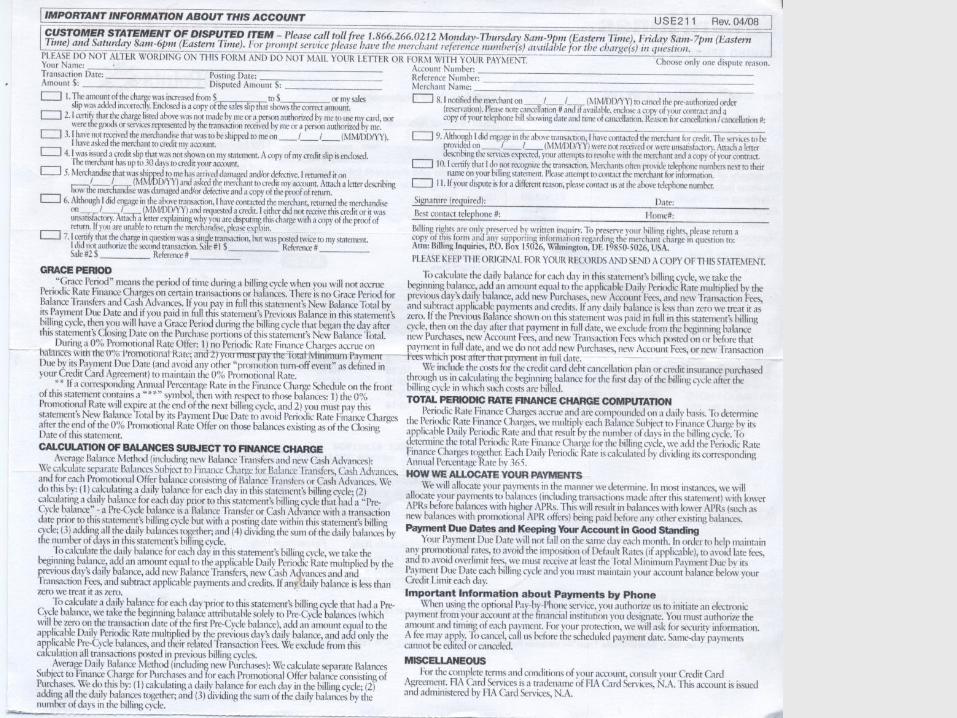

Dispute the Charge-DO NOT PAY

You will not be

charged interest

on any amount on

your credit card

that is under

dispute.

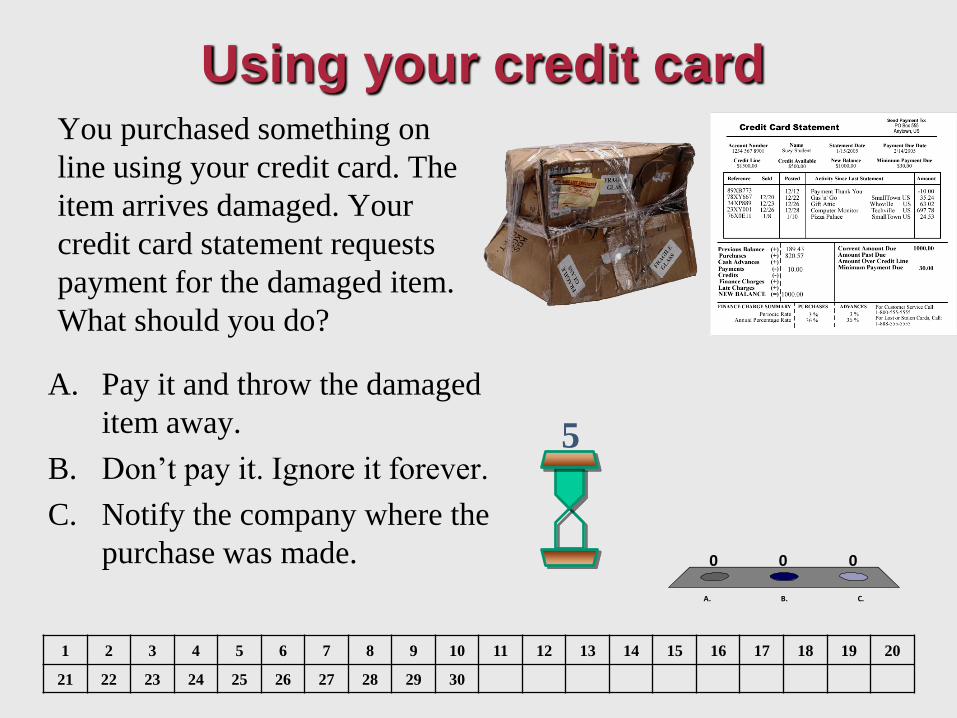

You purchased something on

line using your credit card. The

item arrives damaged. Your

credit card statement requests

payment for the damaged item.

What should you do?

A. B. C.

0 00

5

Using your credit card

A. Pay it and throw the damaged

item away.

B. Don’t pay it. Ignore it forever.

C. Notify the company where the

purchase was made.

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

21 22 23 24 25 26 27 28 29 30

Chapter 27

Introduction to Business, Your Credit and the Law Slide 35 of 60

Stop Payment

The Fair Credit

Billing Act permits

consumers to stop a

credit card payment for

items that are

damaged or defective.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 36 of 60

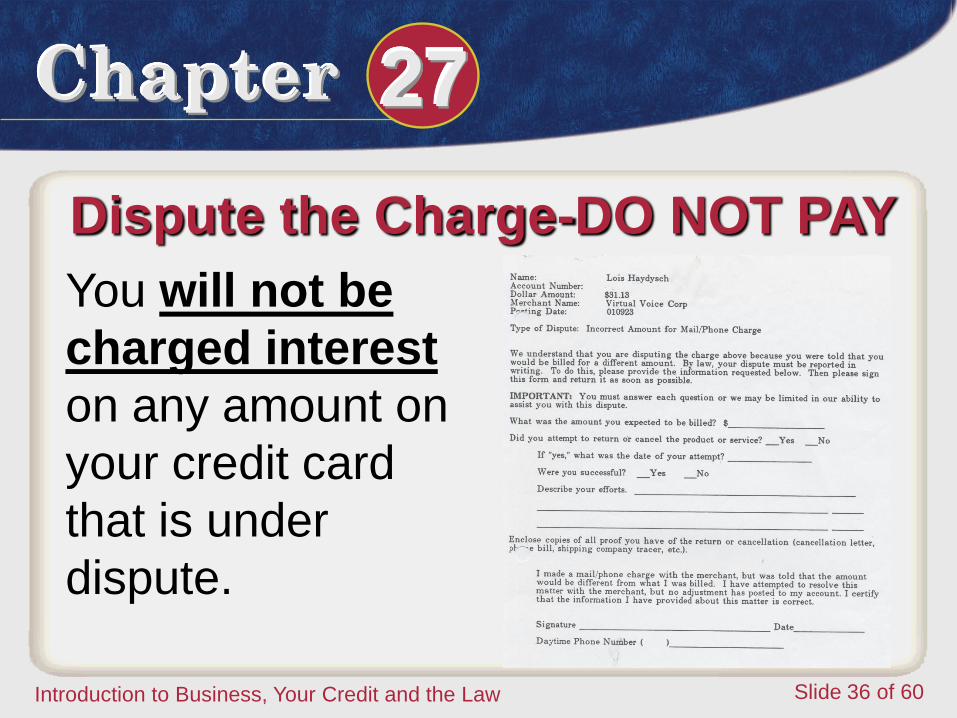

Dispute the Charge-DO NOT PAY

You will not be

charged interest

on any amount on

your credit card

that is under

dispute.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 37 of 60

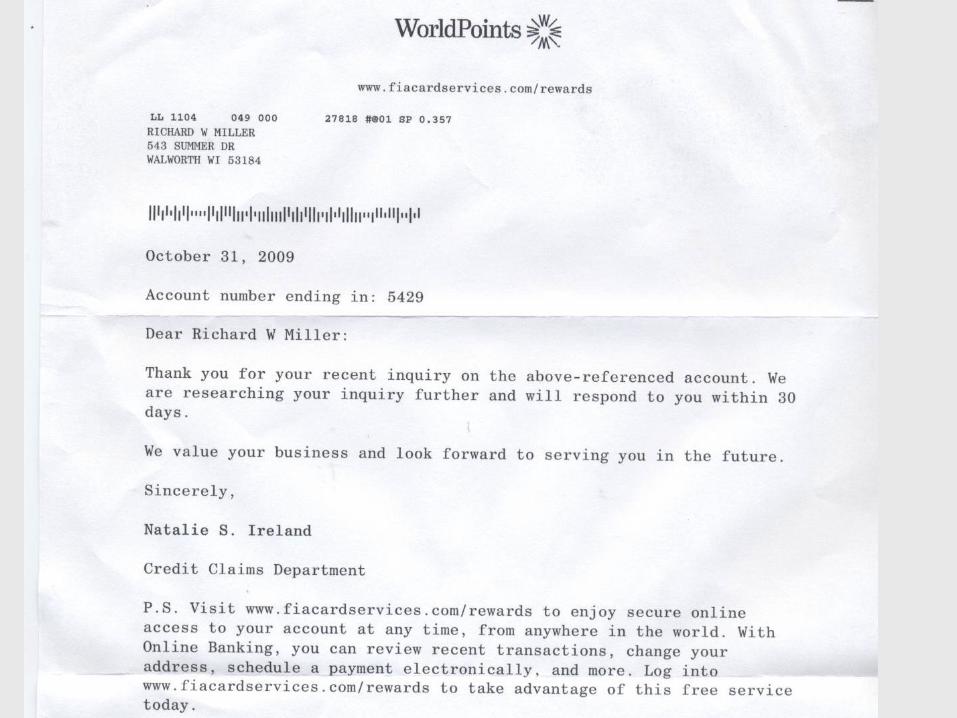

Dispute a Credit Card Charge Activity

Chapter 27 Your Credit and the Law pp. 434- 447

Chapter 27

Introduction to Business, Your Credit and the Law Slide 44 of 60

Learning Objectives

1. Identify consumers’ credit rights.

2. Describe how to handle credit problems.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 45 of 60

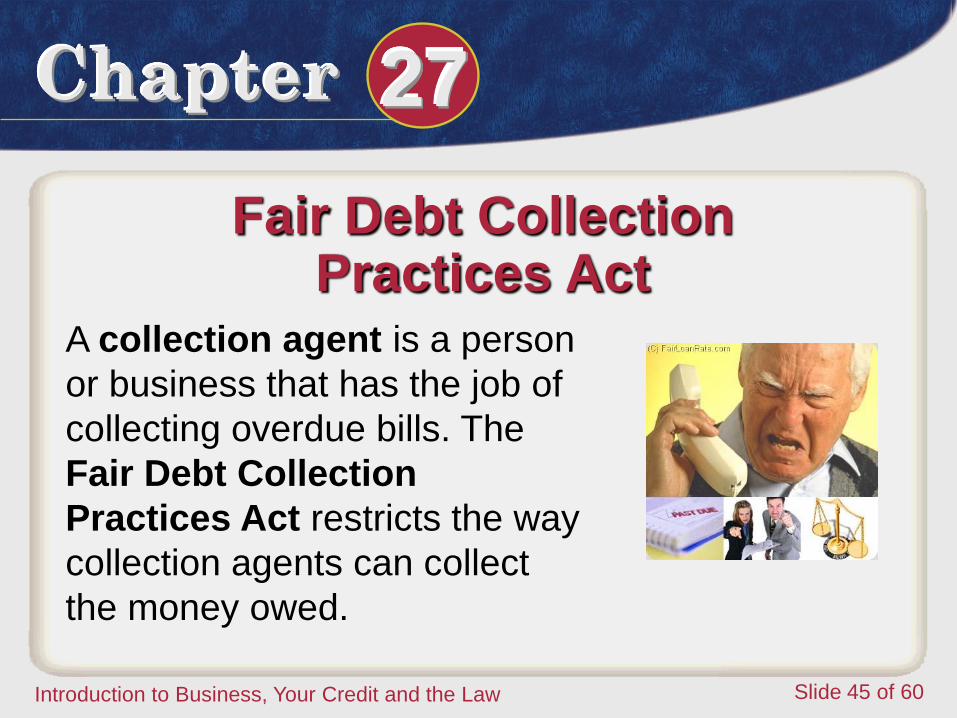

Fair Debt Collection Practices Act

A collection agent is a person

or business that has the job of

collecting overdue bills. The

Fair Debt Collection

Practices Act restricts the way

collection agents can collect

the money owed.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 46 of 60

10 Ways Debt Collectors Break the Law

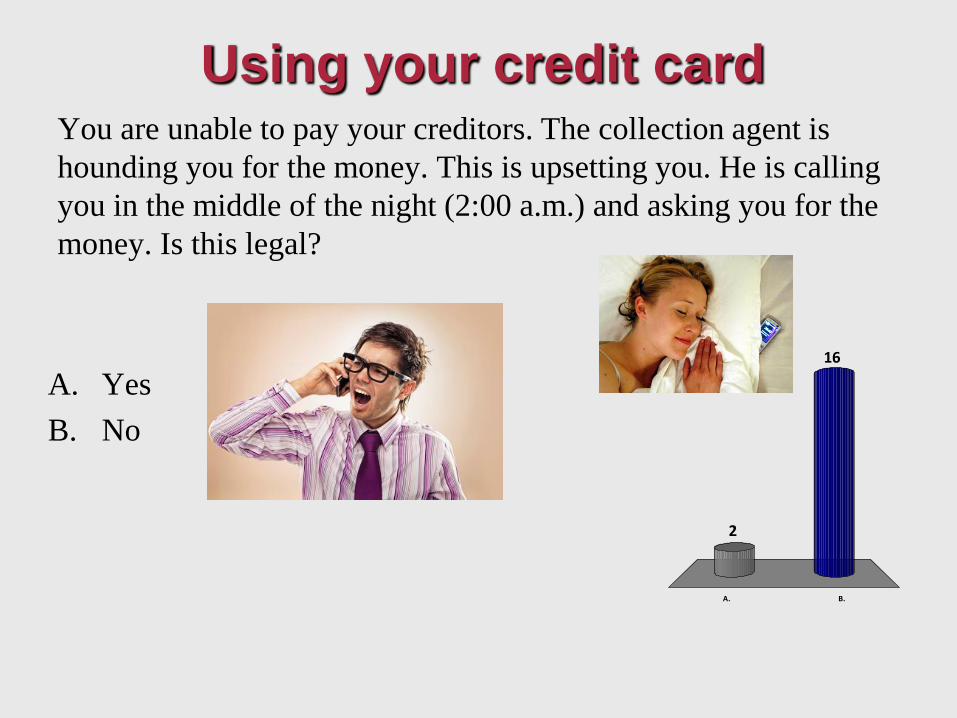

You are unable to pay your creditors. The collection agent is

hounding you for the money. This is upsetting you. He is calling

you in the middle of the night (2:00 a.m.) and asking you for the

money. Is this legal?

A. B.

16

2

Using your credit card

A. Yes

B. No

Chapter 27

Introduction to Business, Your Credit and the Law Slide 48 of 60

Fair Debt Collection Practices Act

Answer: No. The Fair Debt Collection

Practices Act makes this illegal.

Before this act, collection agents

could use any method they chose to

collect the money.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 49 of 60

Fair Debt Collection Practices Act

Answer: No. The Fair Debt Collection

Practices Act makes this illegal.

Before this act, collection agents

could use any method they chose to

collect the money.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 50 of 60

Fair Debt Collection Practices Act

If they use the phone, collection agents

can only call you at home between

8:00 a.m. and 9:00 p.m. They also

cannot continue calling and/or pretend

to be someone else.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 51 of 60

Fair Debt Collection Practices Act

1. Collection agents must identify

themselves to the people whose bills

they’re trying to collect. My name is George

and I’m hear to

collect the $200 you

owe XYZ company.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 52 of 60

Fair Debt Collection Practices Act

2. Collection agents can’t tell

others about the debt.

3. Collection agents can’t

contact a person at work

if the employer doesn’t

permit it.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 53 of 60

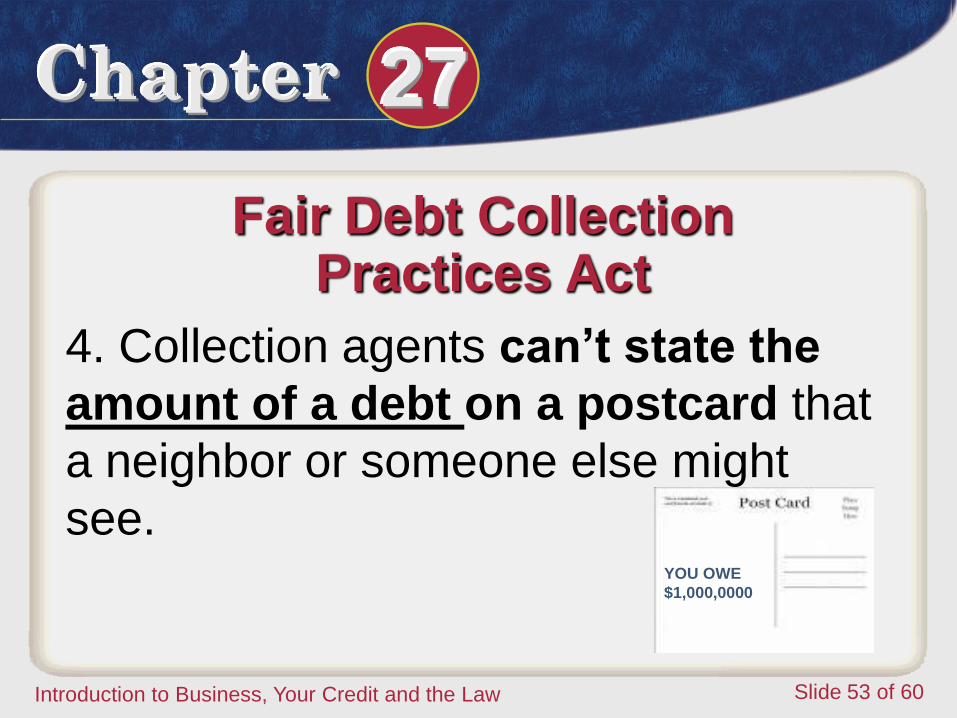

Fair Debt Collection Practices Act

4. Collection agents can’t state the

amount of a debt on a postcard that

a neighbor or someone else might

see. YOU OWE

$1,000,0000

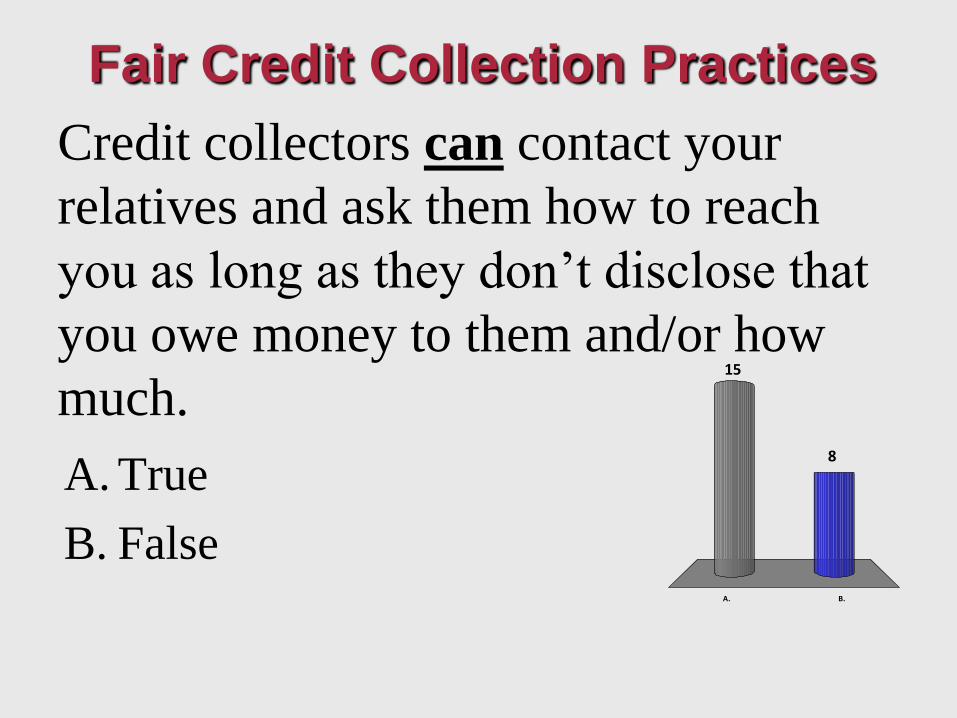

Credit collectors can contact your

relatives and ask them how to reach

you as long as they don’t disclose that

you owe money to them and/or how

much.

A. B.

8

15

Fair Credit Collection Practices

A. True

B. False

Chapter 27

Introduction to Business, Your Credit and the Law Slide 55 of 60

Fair Credit Reporting Act

When you apply for and use credit, the

information goes into a file at one or more

credit bureaus. (Trans Union, Equifax,

Experian).

A credit file includes current and past

addresses, employment history,

financial information and criminal

record.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 56 of 60

Fair Credit Reporting Act

The Fair Credit

Reporting Act was

passed because of

concerns about the

accuracy of credit file

information.

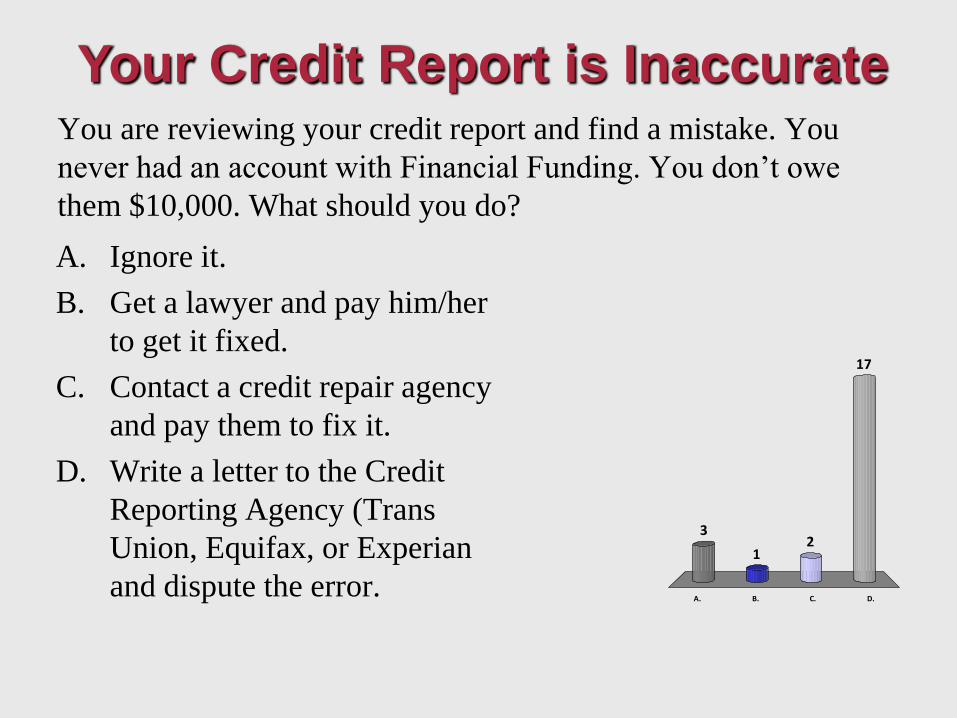

You are reviewing your credit report and find a mistake. You

never had an account with Financial Funding. You don’t owe

them $10,000. What should you do?

A. B. C. D.

3

17

21

Your Credit Report is Inaccurate

A. Ignore it.

B. Get a lawyer and pay him/her

to get it fixed.

C. Contact a credit repair agency

and pay them to fix it.

D. Write a letter to the Credit

Reporting Agency (Trans

Union, Equifax, or Experian

and dispute the error.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 58 of 60

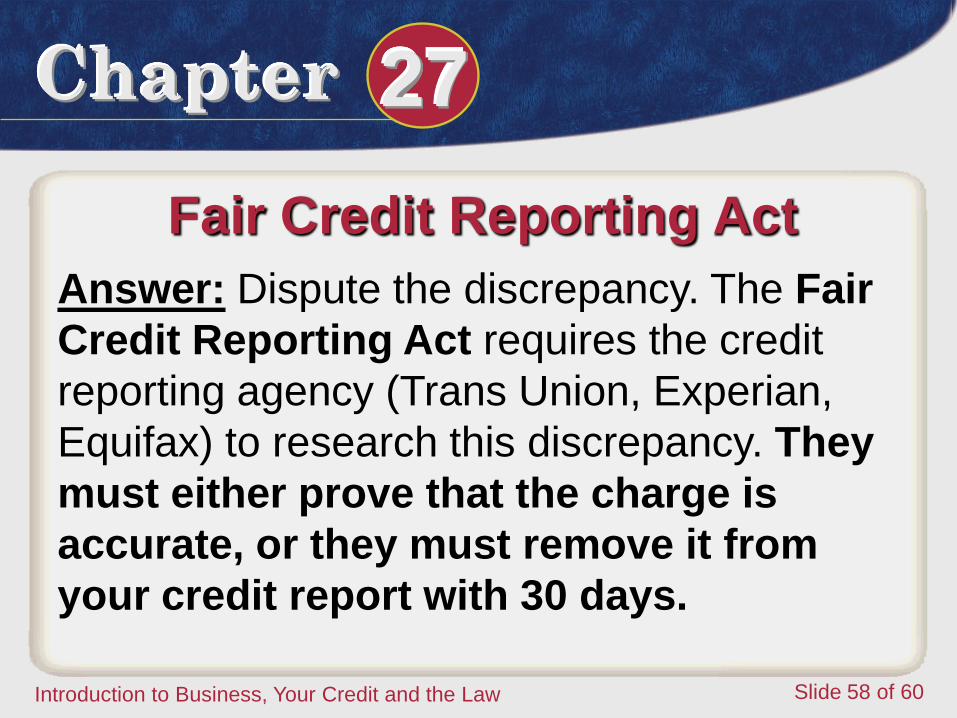

Fair Credit Reporting Act

Answer: Dispute the discrepancy. The Fair

Credit Reporting Act requires the credit

reporting agency (Trans Union, Experian,

Equifax) to research this discrepancy. They

must either prove that the charge is

accurate, or they must remove it from

your credit report with 30 days.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 59 of 60

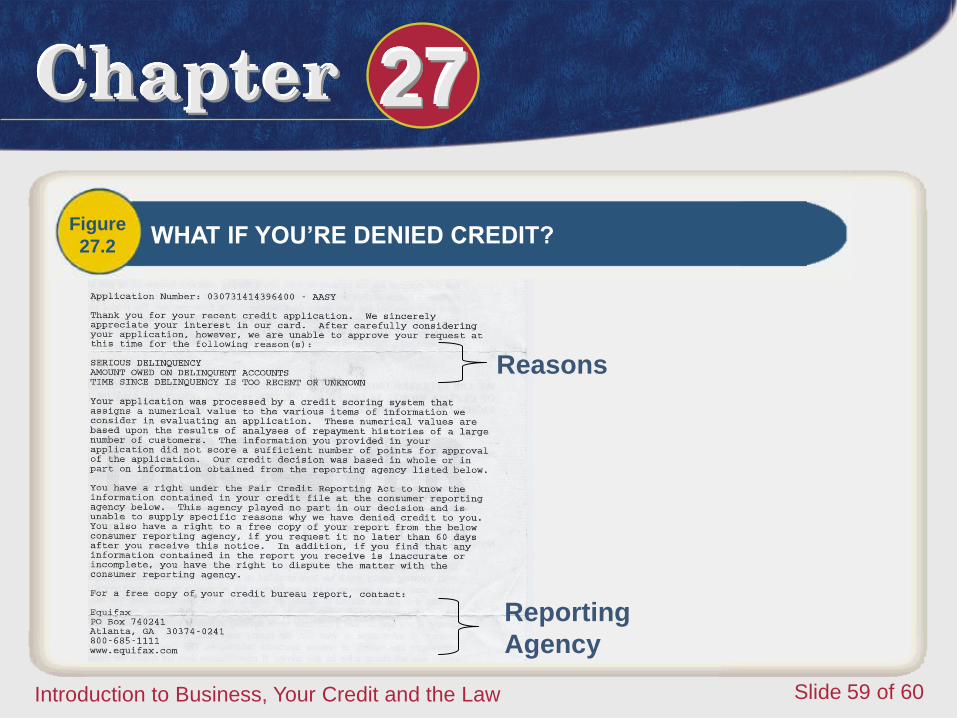

Figure

27.2 WHAT IF YOU’RE DENIED CREDIT?

Reasons

Reporting

Agency

Chapter 27

Introduction to Business, Your Credit and the Law Slide 60 of 60

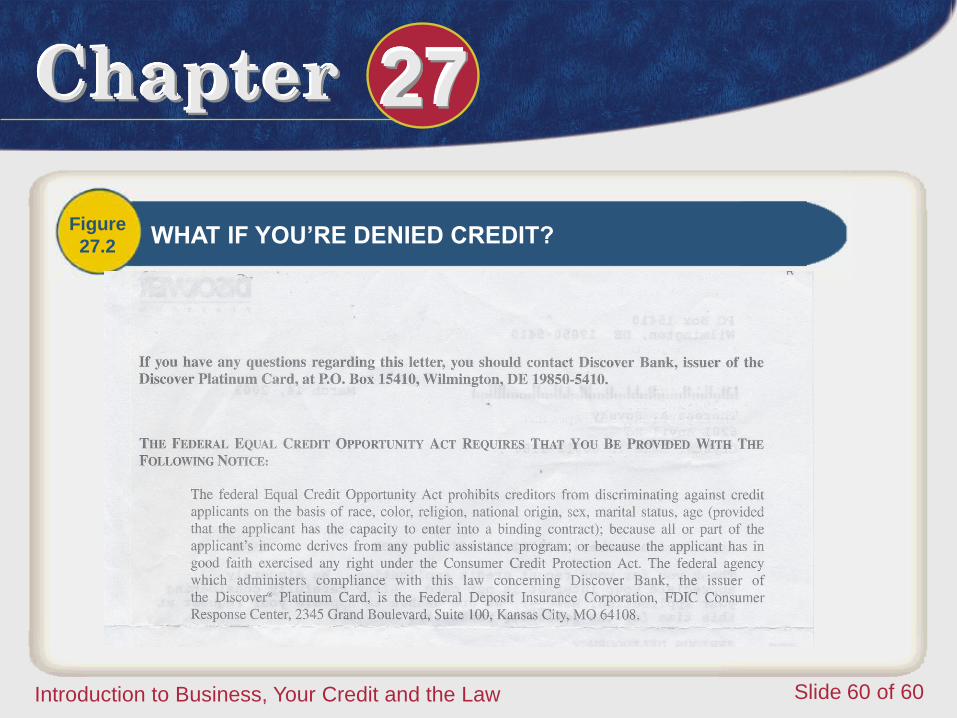

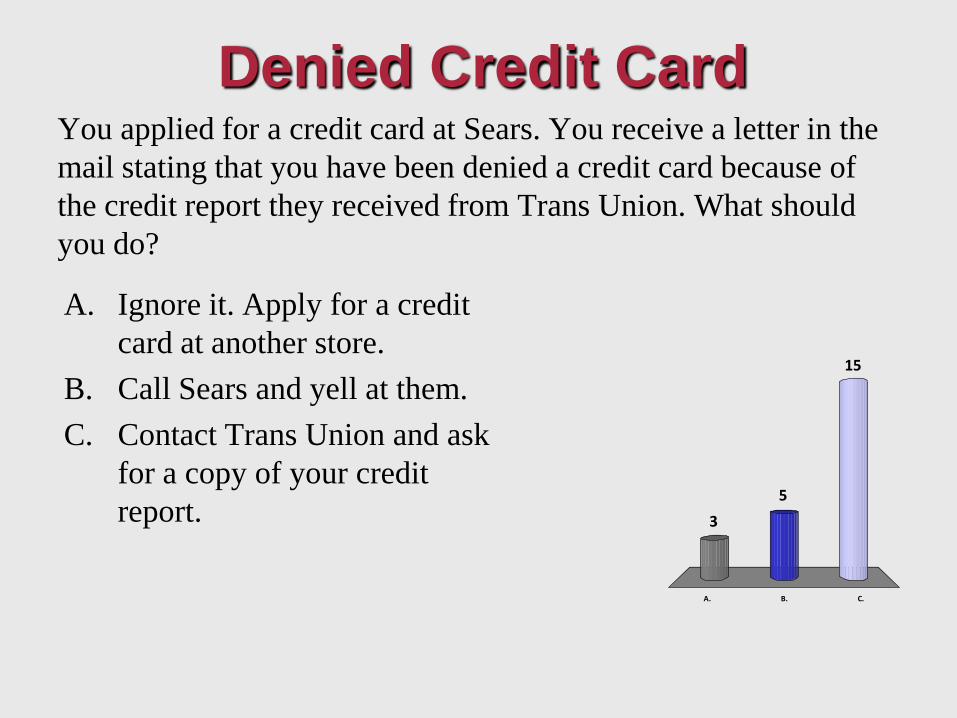

Figure

27.2 WHAT IF YOU’RE DENIED CREDIT?

You applied for a credit card at Sears. You receive a letter in the

mail stating that you have been denied a credit card because of

the credit report they received from Trans Union. What should

you do?

A. B. C.

3

15

5

Denied Credit Card

A. Ignore it. Apply for a credit

card at another store.

B. Call Sears and yell at them.

C. Contact Trans Union and ask

for a copy of your credit

report.

Chapter 27

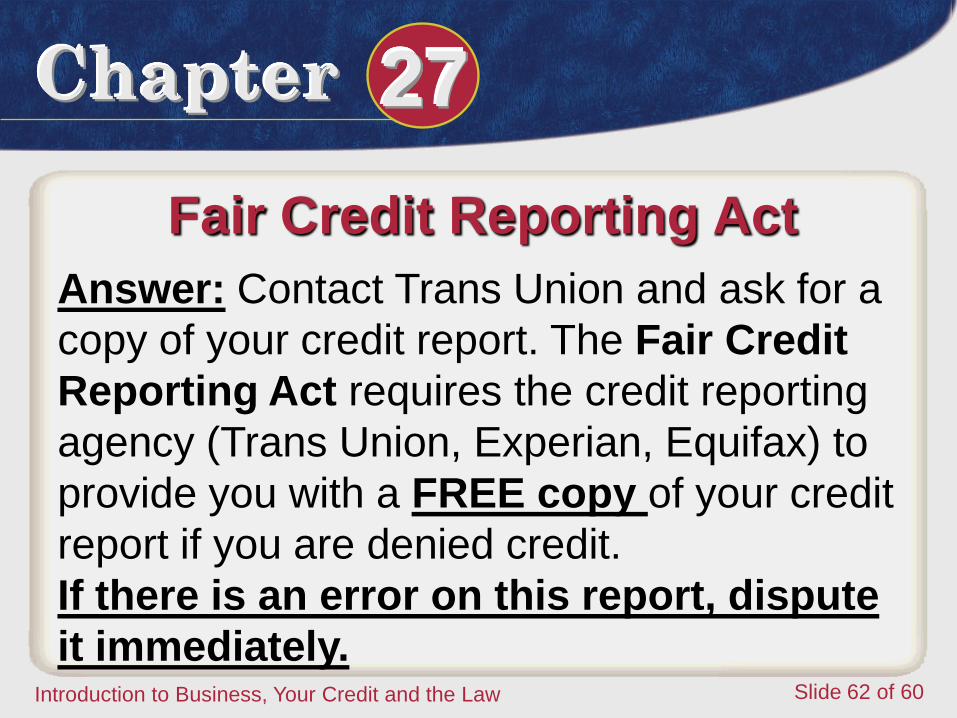

Introduction to Business, Your Credit and the Law Slide 62 of 60

Fair Credit Reporting Act

Answer: Contact Trans Union and ask for a

copy of your credit report. The Fair Credit

Reporting Act requires the credit reporting

agency (Trans Union, Experian, Equifax) to

provide you with a FREE copy of your credit

report if you are denied credit.

If there is an error on this report, dispute

it immediately.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 63 of 60

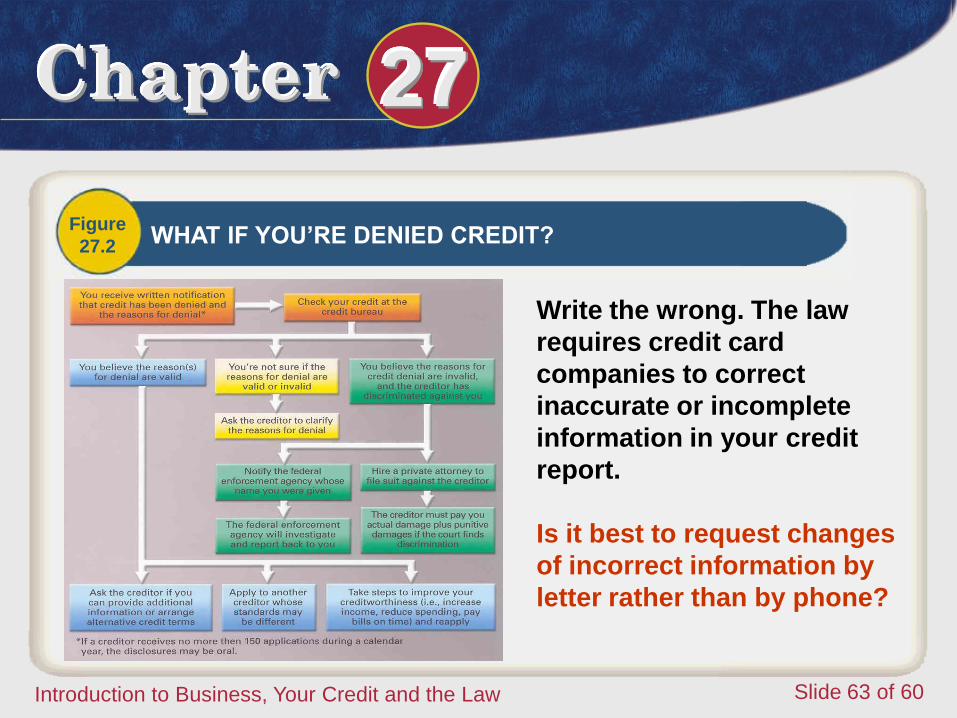

Figure

27.2 WHAT IF YOU’RE DENIED CREDIT?

Write the wrong. The law

requires credit card

companies to correct

inaccurate or incomplete

information in your credit

report.

Is it best to request changes

of incorrect information by

letter rather than by phone?

Chapter 27

Introduction to Business, Your Credit and the Law Slide 64 of 60

Right to Privacy

According to the law, only authorized

persons can see a copy of your credit

report.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 65 of 60

Right to Be Notified

The Fair Credit Reporting Act states

that you must be notified when an

investigation is being conducted on

your credit record.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 66 of 60

Right to 1 Free Credit Report Each Year

The Fair Credit Reporting Act

also states that you are entitled

to 1 FREE credit report each

year, from each of the reporting

agencies (Trans Union, Equifax,

Experian).

Chapter 27

Introduction to Business, Your Credit and the Law Slide 67 of 60

Credit Report Commercials

Commercials

Chapter 27

Introduction to Business, Your Credit and the Law Slide 68 of 60

Credit Services

Some companies charge a fee to

“clean up” your credit rating but

they’re seldom able to restore a bad

credit rating.

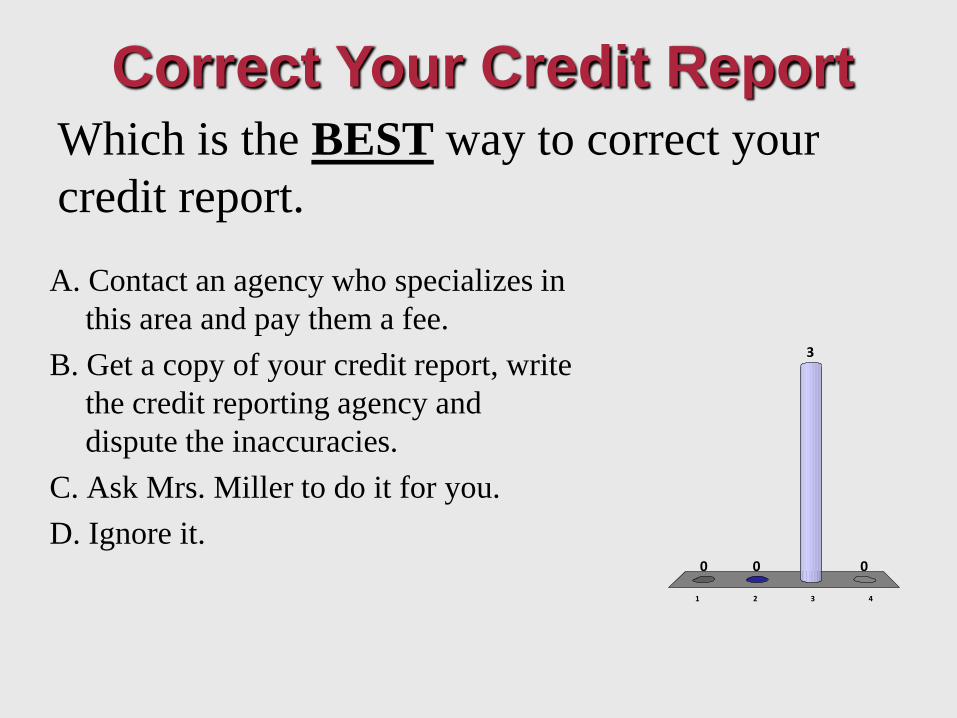

Video

Which is the BEST way to correct your

credit report.

1 2 3 4

0 0

3

0

Correct Your Credit Report

A. Contact an agency who specializes in

this area and pay them a fee.

B. Get a copy of your credit report, write

the credit reporting agency and

dispute the inaccuracies.

C. Ask Mrs. Miller to do it for you.

D. Ignore it.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 70 of 60

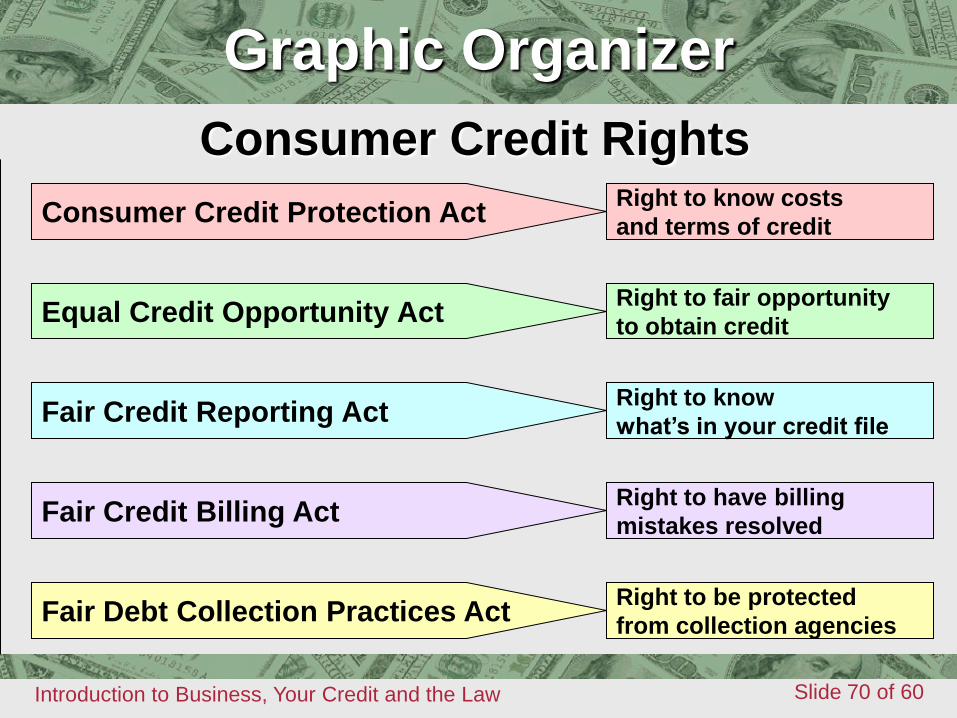

Graphic Organizer Consumer Credit Rights

Graphic Organizer

Consumer Credit Protection Act

Equal Credit Opportunity Act

Fair Credit Reporting Act

Fair Credit Billing Act

Fair Debt Collection Practices Act

Right to know costs

and terms of credit

Right to fair opportunity

to obtain credit

Right to know

what’s in your credit file

Right to have billing

mistakes resolved

Right to be protected

from collection agencies

Chapter 27

Introduction to Business, Your Credit and the Law Slide 71 of 60

February 2010-new regulations so that

banks cannot dig borrowers deeper into

debt.

Video

New Credit Law

Chapter 27

Introduction to Business, Your Credit and the Law Slide 72 of 60

1. Interest Rates cannot be raised in the

first year after an account is opened

UNLESS it is an introductory “teaser” rate.

New Credit Law

Chapter 27

Introduction to Business, Your Credit and the Law Slide 73 of 60

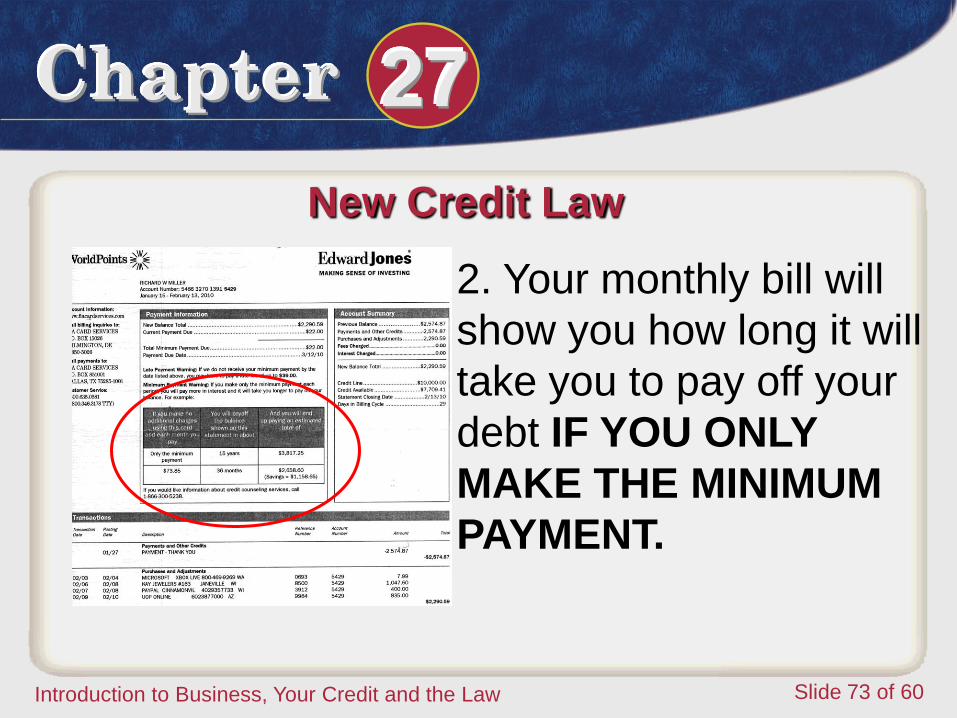

2. Your monthly bill will

show you how long it will

take you to pay off your

debt IF YOU ONLY

MAKE THE MINIMUM

PAYMENT.

New Credit Law

Chapter 27

Introduction to Business, Your Credit and the Law Slide 74 of 60

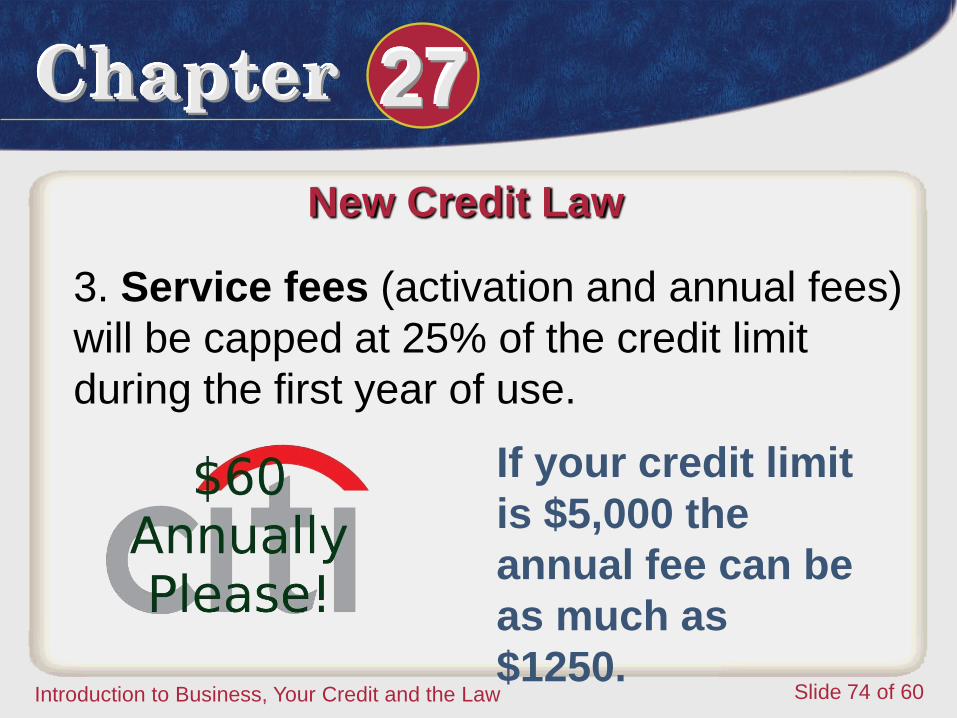

3. Service fees (activation and annual fees)

will be capped at 25% of the credit limit

during the first year of use.

New Credit Law

If your credit limit

is $5,000 the

annual fee can be

as much as

$1250.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 75 of 60

4. Due date is consistent.

5. Statement must be sent out

21 days before the payment due

date.

6. Over the limit fees – You will

be informed BEFORE you go

over the limit.

New Credit Law

Chapter 27

Introduction to Business, Your Credit and the Law Slide 76 of 60

7. Cannot raise interest rates

on existing balances.

8. Credit cards CANNOT be

issued to anyone under 21,

UNLESS there is a co-signer or

you have the capacity (JOB) to

pay a loan.

9. Banks are not allowed to

hand out gifts on or near

college campuses or at their

events.

New Credit Law

Chapter 27

Introduction to Business, Your Credit and the Law Slide 77 of 60

Enforcing the Laws

The Federal Trade Commission

(FTC) is responsible for enforcing the

laws on credit.

The FTC also helps consumers with

credit problems.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 78 of 60

Enforcing the Laws

On the state level, you can contact

your state banking department

about credit problems.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 79 of 60

Enforcing the Laws

A consumer protection division of your

state attorney general’s office deals

with complaints that other government

agencies might not handle.

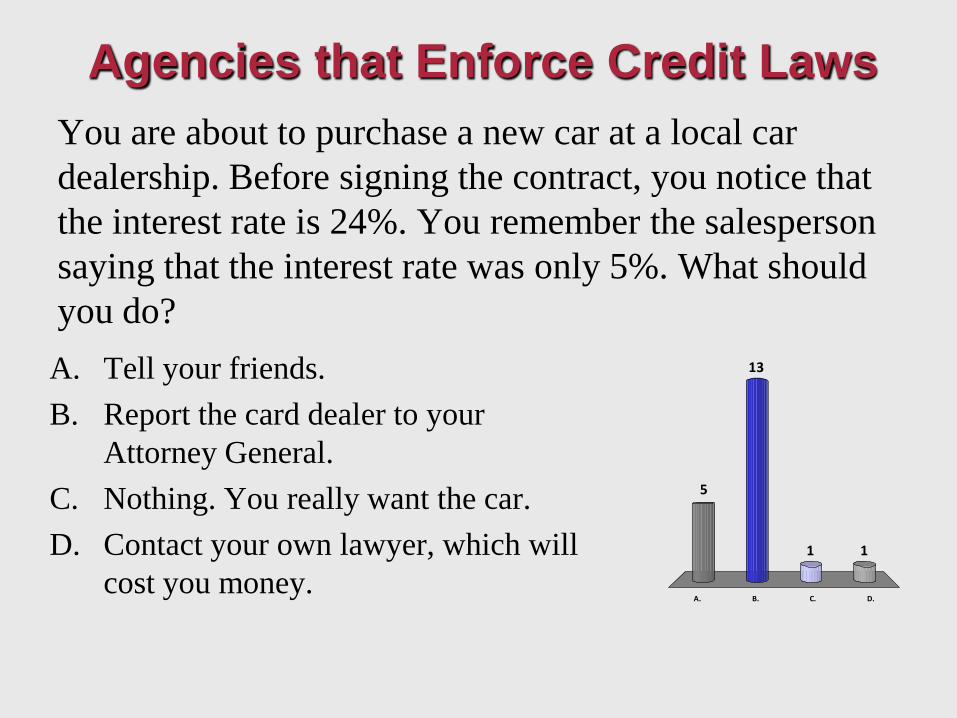

You are about to purchase a new car at a local car

dealership. Before signing the contract, you notice that

the interest rate is 24%. You remember the salesperson

saying that the interest rate was only 5%. What should

you do?

A. B. C. D.

5

11

13

Agencies that Enforce Credit Laws

A. Tell your friends.

B. Report the card dealer to your

Attorney General.

C. Nothing. You really want the car.

D. Contact your own lawyer, which will

cost you money.

Chapter 27

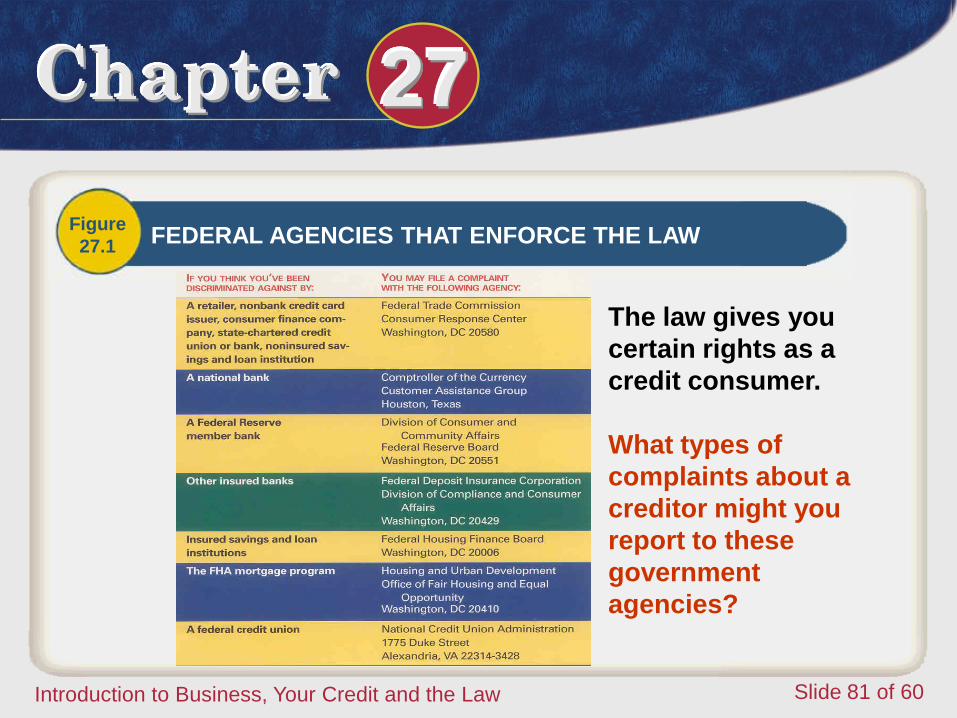

Introduction to Business, Your Credit and the Law Slide 81 of 60

Figure

27.1 FEDERAL AGENCIES THAT ENFORCE THE LAW

The law gives you

certain rights as a

credit consumer.

What types of

complaints about a

creditor might you

report to these

government

agencies?

Chapter 27

Introduction to Business, Your Credit and the Law Slide 82 of 60

Debt! Help!

You have over spent and are in debt.

What should you do?

Chapter 27

Introduction to Business, Your Credit and the Law Slide 83 of 60

Debt! Help!

The first thing you should do

is contact your creditors

(bank, credit card companies,

etc.) and ask them if they can

lower your payments due to

your financial situation. Most

companies are willing to work

with you.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 84 of 60

2. Credit Counseling

A credit counselor can help you

revise your budget, contact creditors to

arrange new payment plans, or help

you find other sources of income such

as getting a part time (seasonal) job.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 85 of 60

Credit Services

If you need a credit counselor, you

can check with your Better Business

Bureau or contact your local

Chamber of Commerce.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 86 of 60

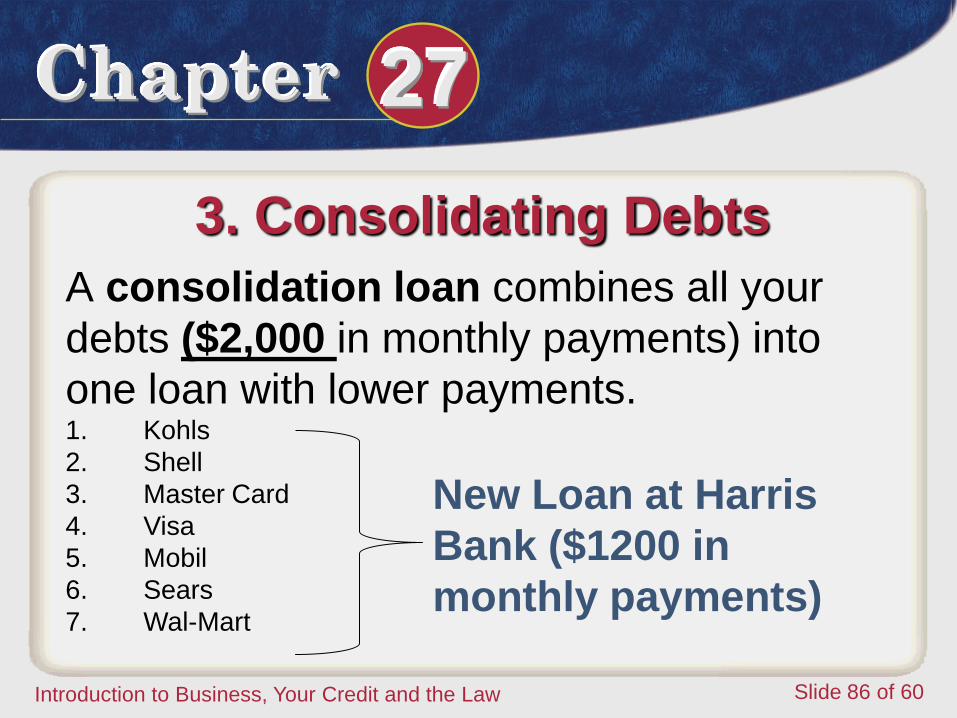

3. Consolidating Debts

A consolidation loan combines all your

debts ($2,000 in monthly payments) into

one loan with lower payments. 1. Kohls

2. Shell

3. Master Card

4. Visa

5. Mobil

6. Sears

7. Wal-Mart

New Loan at Harris

Bank ($1200 in

monthly payments)

Chapter 27

Introduction to Business, Your Credit and the Law Slide 87 of 60

Consolidating Debts

The two problems with a consolidation

loan are:

• There is usually a high interest rate

because people who get such loans

are considered poor credit risks.

continued

Chapter 27

Introduction to Business, Your Credit and the Law Slide 88 of 60

Consolidating Debts

• Because there is only one monthly

payment, you might feel that the credit

problem is under control and start

charging new purchases.

• CUT UP THOSE CHARGE CARDS

Chapter 27

Introduction to Business, Your Credit and the Law Slide 89 of 60

4. Bankruptcy

Bankruptcy is a legal process in which you are

relieved of your debts, but your creditors can take

some or all of your assets.

You must get an attorney and pay a filing fee.

This could cost you as much as $1,800.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 90 of 60

4. Bankruptcy

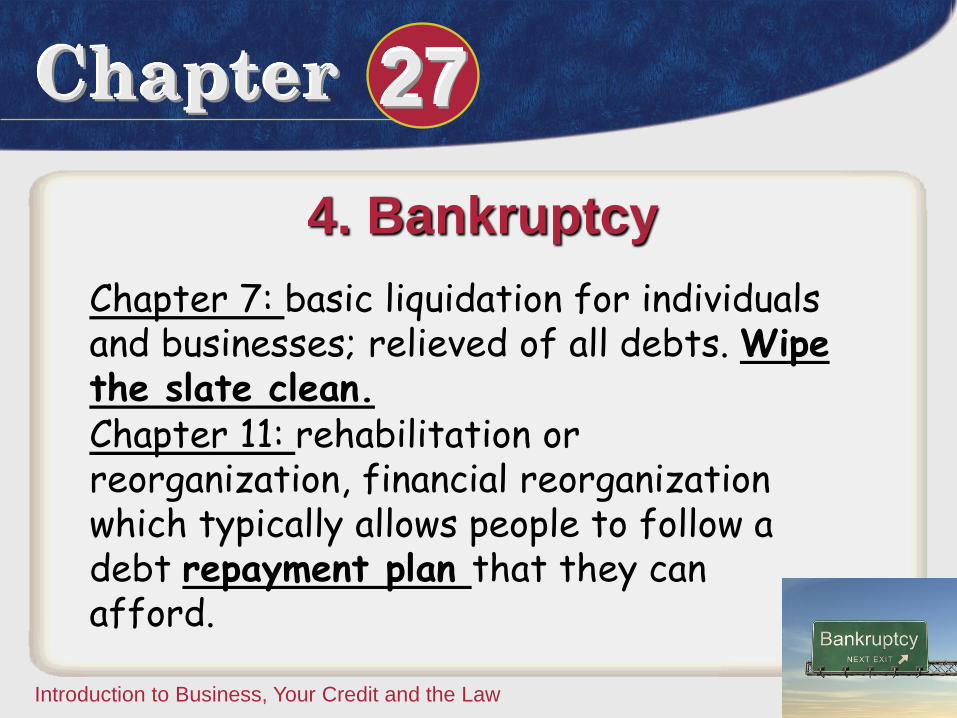

Chapter 7: basic liquidation for individuals and businesses; relieved of all debts. Wipe the slate clean.

Chapter 11: rehabilitation or reorganization, financial reorganization which typically allows people to follow a debt repayment plan that they can afford.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 91 of 60

4. Bankruptcy

When bankruptcy is declared, the

debtor, the creditor, and a court-

appointed trustee come up with a plan

to repay the debt on an installment

basis.

Chapter 27

Introduction to Business, Your Credit and the Law Slide 92 of 60

4. Bankruptcy

You should avoid bankruptcy because

it gives you a bad credit record.

Recent changes in the law have made

it harder to declare bankruptcy.

Which of the following is the 1st step you should take when you can’t pay your creditors?

Your Credit Report is Inaccurate

A. File Bankruptcy

B. Contact your creditors.

C. Get a consolidation loan

D. Find a credit counselor.

End of Chapter Your Credit and the Law

27

![Universities Service Centre for China Studies -- Homeww2.usc.cuhk.edu.hk/DCS/Docs/31-16-02.pdf · 2014. 11. 14. · B4d33 B4d53 B4d73 (10)-EfL B4b2CJ B4c4 B4d14 B4d24 B4d34 B4d44DC]](https://img.pdfslide.net/doc/110x75/60c465160884291b0c15ade2/universities-service-centre-for-china-studies-2014-11-14-b4d33-b4d53-b4d73.jpg)